Health insurance in the United States has become a contentious issue, as skyrocketing premiums, deductibles, and out-of-pocket costs are increasingly siphoning wealth from American households. While ostensibly designed to provide financial protection against medical expenses, the system often functions more like a profit-driven machine, with insurance companies, pharmaceutical corporations, and healthcare providers reaping massive benefits at the expense of consumers. The lack of price transparency, exorbitant administrative costs, and a fragmented market dominated by a few powerful players have created a system where even those with insurance struggle to afford necessary care. As a result, millions of Americans are forced to choose between their health and financial stability, while the industry continues to amass record profits, effectively bleeding the nation’s wealth dry.

Explore related products

What You'll Learn

- Skyrocketing Premiums & Deductibles: Annual increases outpace inflation, squeezing household budgets and limiting disposable income

- Profit Over Patients: Insurance companies prioritize shareholder returns, denying claims and delaying care for maximum profit

- Administrative Bloat: Excessive paperwork and bureaucracy inflate costs, diverting funds from actual healthcare services

- Pharmacy Benefit Managers (PBMs): Middlemen drive up drug prices, profiting from the system while patients pay more

- Lack of Price Transparency: Hidden costs and opaque billing practices make it impossible for consumers to shop wisely

![]()

Skyrocketing Premiums & Deductibles: Annual increases outpace inflation, squeezing household budgets and limiting disposable income

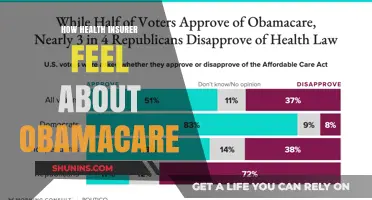

American households are facing a silent crisis as health insurance premiums and deductibles soar at rates that far exceed inflation. In 2023, the average annual premium for employer-sponsored family coverage surpassed $22,000, with workers contributing over $6,000 of that amount. Meanwhile, deductibles have climbed to an average of $1,700 for individual plans, leaving families vulnerable to out-of-pocket expenses before insurance even kicks in. These increases are not mere numbers; they represent a growing share of household income that could otherwise be saved, invested, or spent on education, housing, or leisure.

Consider a middle-class family earning $70,000 annually. With premiums and deductibles consuming nearly 10% of their income, their disposable income shrinks, forcing difficult trade-offs. For instance, a family might delay a child’s orthodontic treatment, skip a vacation, or dip into emergency savings to cover medical costs. This financial strain is exacerbated by the fact that wage growth has not kept pace with healthcare inflation, which rose 4.5% in 2022 compared to a 3.5% increase in average wages. The result? A widening gap between what Americans earn and what they must spend to maintain health coverage.

To mitigate this burden, households can take proactive steps. First, evaluate employer-sponsored plans during open enrollment, focusing on high-deductible health plans (HDHPs) paired with health savings accounts (HSAs). While HDHPs have higher out-of-pocket costs, they often come with lower premiums and tax-advantaged savings opportunities. For example, a family of four could save $2,000 annually by switching to an HDHP and contributing to an HSA, which can be used for qualified medical expenses tax-free. Second, explore state or federal marketplaces for subsidized plans if employer coverage is unaffordable. Subsidies are available for households earning up to 400% of the federal poverty level, capping premium costs at a percentage of income.

However, these strategies are not without pitfalls. HDHPs may discourage necessary care due to high upfront costs, while marketplace plans often have limited provider networks. Additionally, reliance on subsidies ties financial stability to political decisions, as changes in policy could reduce or eliminate these benefits. The takeaway is clear: while individuals can take steps to manage costs, systemic reform is necessary to address the root causes of skyrocketing premiums and deductibles. Until then, American households will continue to bear the brunt of a healthcare system that prioritizes profit over accessibility.

Mastering Health Insurance Calculations: A Step-by-Step Guide for Accurate Estimates

You may want to see also

Explore related products

![]()

Profit Over Patients: Insurance companies prioritize shareholder returns, denying claims and delaying care for maximum profit

Health insurance companies in the U.S. are increasingly acting as profit-driven entities, often at the expense of patient care. A 2022 analysis by the American Medical Association revealed that 1 in 5 medical claims are initially denied, with insurers leveraging complex algorithms and fine-print policies to reject coverage. For instance, a 45-year-old patient with stage 2 breast cancer might see her insurer deny coverage for a recommended PET scan, citing it as "experimental," despite clinical guidelines supporting its use. This systematic denial forces patients into costly appeals processes, delaying treatment and exacerbating health outcomes.

Consider the mechanics of how insurers maximize profits: by minimizing payouts. A common tactic is "prior authorization," where insurers require providers to justify treatments before approval. For a 60-year-old diabetic needing a specific insulin brand (e.g., Humalog U-200, priced at $275 per vial), the insurer might delay approval for weeks, pushing the patient toward a cheaper, less effective alternative. This delay not only risks complications like diabetic ketoacidosis but also shifts the financial burden onto patients or providers. Insurers save billions annually through such tactics, funneling these savings into shareholder dividends rather than improving care.

The financial incentives driving this behavior are stark. In 2021, UnitedHealth Group, the largest U.S. insurer, reported $20 billion in profits, with 85% allocated to shareholders and executive bonuses. Meanwhile, a Kaiser Family Foundation study found that 40% of insured Americans delayed care due to cost concerns. This profit-first model is unsustainable. For example, a 30-year-old with a herniated disc might wait months for MRI approval, during which time the condition worsens, requiring more invasive (and costly) surgery. The insurer saves short-term but shifts long-term costs onto the patient and healthcare system.

To combat this, patients must become proactive advocates. First, scrutinize your policy’s Explanation of Benefits (EOB) for denied claims and appeal within 30 days using specific medical evidence. Second, leverage state insurance commissioners to dispute unfair denials—in California, 65% of appealed denials are overturned. Third, support legislative reforms like the proposed "No Surprises Act" expansions, which cap out-of-network charges and streamline appeals. Finally, consider joining group plans or health-sharing ministries, which often bypass insurer profiteering. The system won’t change without collective action, but individual steps can mitigate its predatory effects.

H4 Visa Health Insurance: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Administrative Bloat: Excessive paperwork and bureaucracy inflate costs, diverting funds from actual healthcare services

The American healthcare system is drowning in paperwork. For every dollar spent on healthcare, nearly a quarter disappears into the administrative void—a staggering figure that eclipses the administrative costs of any other developed nation. This bureaucratic morass isn’t just inefficient; it’s a deliberate siphon, diverting funds from patient care to line the pockets of insurance companies and administrative middlemen. Consider this: doctors spend nearly a third of their time on paperwork, not patients. Nurses juggle charts instead of providing care. Hospitals employ armies of billing specialists to navigate the labyrinthine claims process. This isn’t healthcare—it’s a paperwork factory masquerading as one.

Let’s break down the mechanics of this administrative bloat. Insurance companies require providers to submit claims using complex, proprietary codes, each with its own nuances and pitfalls. A single mistake—a misplaced decimal, an incorrect modifier—can result in a denied claim, forcing providers to resubmit, appeal, or write off the loss entirely. This system isn’t designed to streamline care; it’s designed to create friction, to justify the existence of an army of administrators whose sole purpose is to process, dispute, and delay payments. For context, the average physician’s office dedicates 15% of its revenue to billing and insurance-related tasks. That’s money that could fund more nurses, better equipment, or lower patient costs.

The human cost of this bureaucracy is just as alarming. Patients face delayed treatments, denied claims, and surprise bills, all because their care is secondary to the administrative process. Take the case of prior authorization—a requirement for insurers to approve certain treatments before they’re administered. This process, which often takes weeks, is responsible for 90% of delays in patient care, according to a 2021 AMA survey. It’s not uncommon for a cancer patient to wait weeks for chemotherapy approval, not because the treatment is questionable, but because an insurance adjuster needs to check a box. This isn’t healthcare; it’s a game of red tape, and patients are the pawns.

To dismantle this system, we need radical simplification. Single-payer systems, like those in Canada or the UK, demonstrate that healthcare can be administered with a fraction of the bureaucracy. Even within the current framework, solutions exist: standardized billing codes, automated claims processing, and the elimination of prior authorization for evidence-based treatments. Providers could redirect the billions saved toward hiring more staff, reducing wait times, and improving patient outcomes. Until then, every form filled out, every hour spent on the phone with an insurer, is a dollar stolen from the care Americans deserve.

Why Your Insurance Company Tracks Mileage: Understanding the Impact

You may want to see also

Explore related products

![]()

Pharmacy Benefit Managers (PBMs): Middlemen drive up drug prices, profiting from the system while patients pay more

Pharmacy Benefit Managers (PBMs) operate as invisible middlemen in the healthcare system, negotiating drug prices between pharmaceutical manufacturers, insurers, and pharmacies. On the surface, their role seems beneficial: lowering costs for insurers and patients. However, the reality is far more insidious. PBMs often inflate drug prices through complex rebate systems, where they pocket a portion of the difference between the list price and the discounted price paid by insurers. For instance, a diabetes medication with a list price of $500 might be sold to an insurer for $300, but the PBM keeps a $100 rebate, leaving the patient to pay a higher copay based on the inflated list price. This system prioritizes PBM profits over patient affordability, making essential medications inaccessible for many.

Consider the case of a 65-year-old patient with hypertension prescribed a brand-name ACE inhibitor. The list price for a 30-day supply is $200, but the PBM negotiates a $50 rebate. Instead of passing the savings to the patient, the PBM retains the rebate, and the patient’s copay remains high, often $50 or more. Over a year, this adds up to $600 in out-of-pocket costs, a significant burden for someone on a fixed income. Meanwhile, the PBM profits from the rebate, creating a perverse incentive to keep list prices high. This practice is not an anomaly but a systemic issue, as PBMs control over 80% of the prescription drug market in the U.S.

To combat this, patients can take proactive steps. First, ask your pharmacist for the cash price of a medication, which is often lower than the insurance copay due to PBM markups. Second, inquire about generic alternatives or manufacturer copay assistance programs, which bypass PBM involvement. For example, a generic statin for cholesterol management might cost $10 for a 90-day supply through a discount program, compared to a $40 copay for the brand-name version. Third, advocate for legislative reforms that increase PBM transparency and regulate rebate practices. States like Ohio and Louisiana have already passed laws requiring PBMs to disclose their fees, a step toward holding them accountable.

The takeaway is clear: PBMs exploit their position in the drug supply chain to maximize profits at the expense of patients. Their opaque practices drive up costs, making healthcare less affordable and more inequitable. By understanding how PBMs operate and taking informed actions, patients can mitigate some of the financial strain. However, systemic change is necessary to dismantle this predatory model and ensure medications are accessible to all. Until then, PBMs will continue to bleed American wealth dry, one prescription at a time.

Health Insurance Marketplace and Medicaid: What's the Difference?

You may want to see also

Explore related products

![]()

Lack of Price Transparency: Hidden costs and opaque billing practices make it impossible for consumers to shop wisely

Imagine receiving a medical bill for a routine procedure, only to find it riddled with cryptic charges like "facility fee," "supply surcharge," or "provider assessment." This isn't a hypothetical scenario; it's the reality for countless Americans navigating the labyrinthine world of healthcare billing. Lack of price transparency in the U.S. healthcare system isn't just frustrating—it's a deliberate strategy that exploits consumers, inflates costs, and undermines their ability to make informed financial decisions.

Consider the case of a 45-year-old patient who undergoes a colonoscopy, a preventive service often touted as "fully covered" by insurance. Yet, the bill reveals a $500 "anesthesia fee" and a $300 "pathology charge" for a single polyp removal. These hidden costs, often buried in fine print or omitted from pre-procedure estimates, exemplify how providers and insurers obfuscate pricing. Unlike purchasing a car or even a cup of coffee, healthcare consumers are rarely given a clear, upfront cost breakdown. This opacity forces patients into a financial game of whack-a-mole, where unexpected charges surface long after the service is rendered.

The root of this problem lies in the complex, negotiated rates between insurers and providers, which vary wildly even within the same hospital. For instance, an MRI might cost $500 under one insurer's contract but $2,500 under another. Adding to the chaos, "list prices" (officially known as chargemasters) are often inflated by 300–500%, serving as starting points for negotiations rather than actual costs. This system not only confuses consumers but also shields providers from competitive pressure, allowing them to maintain artificially high prices.

To combat this, consumers can take proactive steps. First, request an itemized bill and scrutinize each charge for errors—studies show up to 80% of medical bills contain inaccuracies. Second, use tools like Healthcare Bluebook or FAIR Health to estimate fair prices for procedures in your area. For those with high-deductible plans, negotiate rates directly with providers or seek cash-pay discounts, which can be 40–60% lower than billed amounts. Finally, advocate for policy changes, such as mandating price transparency laws that require hospitals to publish clear, standardized pricing for common services.

The takeaway is clear: lack of price transparency isn't a bureaucratic oversight—it's a systemic flaw designed to maximize profits at the expense of patients. By demanding clarity, leveraging available tools, and pushing for reform, consumers can begin to reclaim control over their healthcare spending and halt the drain on their financial well-being.

Christian Medical Insurance: Faith-Based Healthcare

You may want to see also

Frequently asked questions

Health insurance premiums, deductibles, and out-of-pocket costs have skyrocketed, forcing many Americans to allocate a significant portion of their income to healthcare. This reduces disposable income and limits savings, effectively draining household wealth.

Yes, many health insurance companies report record profits while premiums and costs for consumers continue to rise. Critics argue that these profits are driven by high administrative costs, shareholder payouts, and restrictive coverage policies that prioritize profit over patient care.

Complex plans with hidden fees, limited provider networks, and confusing coverage terms often leave consumers paying more than they realize. This lack of transparency allows insurers to maximize revenue while patients struggle to understand their financial obligations.

Without a universal healthcare system, Americans rely on private insurers, which operate on a for-profit model. This system incentivizes insurers to minimize payouts and maximize premiums, leading to higher costs for individuals and families compared to countries with single-payer systems.