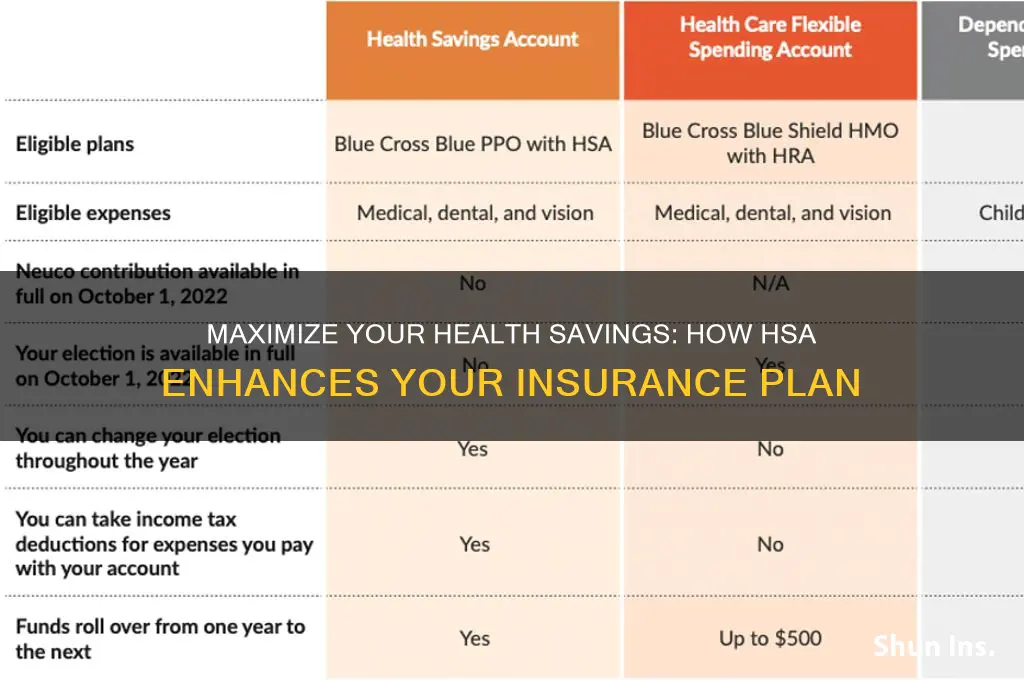

Health Savings Accounts (HSAs) are a valuable tool for individuals seeking to manage healthcare expenses efficiently while enjoying tax advantages. By pairing with a high-deductible health plan (HDHP), HSAs allow users to save pre-tax dollars for qualified medical expenses, reducing taxable income and lowering overall healthcare costs. Contributions grow tax-free, and withdrawals for eligible expenses are also tax-free, providing a triple tax benefit. Additionally, HSAs offer flexibility, as unused funds roll over annually and can be invested for long-term growth, making them a helpful insurance complement that promotes financial security and preparedness for future healthcare needs.

| Characteristics | Values |

|---|---|

| Tax Advantages | Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. |

| Portability | HSAs are owned by the individual, not tied to an employer, and can be carried over even if you change jobs or health plans. |

| Rollover Feature | Funds roll over indefinitely, with no "use-it-or-lose-it" rule like FSAs. |

| Investment Options | Allows investment of contributions for potential long-term growth, similar to a retirement account. |

| Triple Tax Benefit | Only account type offering tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified expenses. |

| High-Deductible Health Plan (HDHP) Pairing | Must be paired with an HDHP, which typically has lower premiums, making it cost-effective for those with low medical expenses. |

| Qualified Medical Expenses Coverage | Covers a wide range of expenses, including deductibles, copays, prescriptions, dental, vision, and more. |

| Retirement Savings | After age 65, funds can be used for non-medical expenses without penalty (though taxes apply if not used for qualified expenses). |

| No Income Limits | Anyone with an HDHP can contribute to an HSA, regardless of income level. |

| Employer Contributions | Employers can contribute to employees' HSAs, reducing taxable income for both parties. |

| Flexibility in Spending | No requirement to spend funds immediately; can save for future medical expenses or retirement. |

| Lower Healthcare Costs | Encourages cost-conscious healthcare decisions due to HDHP pairing and tax incentives. |

| Contribution Limits (2023) | $3,850 for individuals, $7,750 for families, with an additional $1,000 catch-up contribution for those over 55. |

| No Minimum Distribution Requirement | Unlike retirement accounts, there’s no requirement to withdraw funds at a certain age. |

| Estate Planning | Unused funds can be passed to a spouse tax-free or to non-spouse beneficiaries (taxed as income). |

| Reduced Taxable Income | Contributions reduce adjusted gross income (AGI), potentially lowering overall tax liability. |

Explore related products

What You'll Learn

- Tax Benefits: HSA contributions are tax-deductible, reducing taxable income and lowering tax liability

- Triple Tax Advantage: Tax-free contributions, growth, and withdrawals for qualified medical expenses

- Portability: HSAs stay with you, even if you change jobs or health plans

- Investment Growth: Funds can be invested, growing tax-free for long-term healthcare savings

- Retirement Savings: Unused HSA funds roll over annually, aiding in retirement healthcare planning

![]()

Tax Benefits: HSA contributions are tax-deductible, reducing taxable income and lowering tax liability

One of the most compelling advantages of a Health Savings Account (HSA) is its ability to directly reduce your tax burden. When you contribute to an HSA, those funds are deducted from your taxable income, dollar for dollar. For instance, if you earn $60,000 annually and contribute $3,650 (the 2023 individual contribution limit) to your HSA, your taxable income drops to $56,350. This reduction can lower your tax liability significantly, especially if you’re in a higher tax bracket. For someone in the 22% federal tax bracket, this single contribution could save over $800 in taxes.

To maximize this benefit, consider contributing the full annual limit allowed by the IRS. For 2023, individuals can contribute up to $3,850, while families can contribute up to $7,750. If you’re 55 or older, you’re eligible for an additional $1,000 catch-up contribution. These limits are adjusted annually for inflation, so staying informed about current figures is key. Contributions can be made through payroll deductions (pre-tax) or manually, with the latter requiring you to claim the deduction when filing taxes.

A strategic approach to HSA contributions involves timing. If you anticipate a higher income year, maximizing your HSA contributions can offset a larger portion of your taxable income. Conversely, in lower-income years, you might opt for smaller contributions, saving the full limit for years with greater financial flexibility. This flexibility is a unique advantage of HSAs compared to other tax-advantaged accounts like 401(k)s, which have stricter contribution rules.

It’s important to note that HSA contributions are not just tax-deductible—they’re also tax-free when used for qualified medical expenses. This dual benefit means your contributions grow tax-free and can be withdrawn tax-free for eligible healthcare costs, creating a powerful trifecta of tax advantages. For example, if you contribute $5,000 over two years and use it to cover medical expenses, you’ve effectively shielded $5,000 from taxes twice: once when contributing and again when spending.

Finally, consider the long-term impact of these tax benefits. Unlike Flexible Spending Accounts (FSAs), HSAs have no "use-it-or-lose-it" rule, allowing funds to roll over indefinitely. This feature, combined with tax-deductible contributions, makes HSAs a valuable tool for both immediate tax savings and long-term healthcare planning. By strategically contributing to an HSA, you’re not just reducing your current tax liability—you’re building a tax-efficient safety net for future medical expenses.

Steps to Add a Certificate Holder to Your Insurance Policy

You may want to see also

Explore related products

![]()

Triple Tax Advantage: Tax-free contributions, growth, and withdrawals for qualified medical expenses

Health Savings Accounts (HSAs) offer a unique financial tool that maximizes your healthcare dollars through a triple tax advantage: tax-free contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This trifecta of benefits sets HSAs apart from other savings vehicles, making them a powerful strategy for both short-term medical costs and long-term financial planning.

Consider this scenario: A 35-year-old individual contributes $3,600 annually to their HSA, the maximum allowed for self-only coverage in 2023. These contributions are made pre-tax, reducing their taxable income by the same amount. Over 30 years, assuming a conservative 5% annual growth rate, the account could grow to over $250,000. Unlike traditional retirement accounts, withdrawals for qualified medical expenses are entirely tax-free, allowing the individual to access these funds without penalty or tax liability. This makes HSAs a highly efficient way to save for both expected and unexpected healthcare costs.

The key to unlocking the full potential of an HSA lies in understanding qualified medical expenses. These include a wide range of costs, from doctor visits and prescription medications to dental care, vision care, and even certain over-the-counter items. For example, expenses like acupuncture, smoking cessation programs, and mental health counseling qualify, as do medical equipment such as crutches, wheelchairs, and hearing aids. Keeping detailed records of these expenses is crucial, as they can be reimbursed tax-free at any time, even years after the initial contribution.

One often-overlooked strategy is using an HSA as a long-term investment vehicle. By contributing regularly and letting the funds grow tax-free, individuals can build a substantial nest egg for future healthcare needs. For instance, a 25-year-old who contributes $3,000 annually with a 7% annual return could accumulate over $600,000 by age 65. This approach not only covers medical expenses but also supplements retirement savings, as funds can be withdrawn penalty-free for any purpose after age 65 (though non-medical withdrawals are subject to income tax).

To maximize the benefits of an HSA, follow these practical tips: first, contribute the maximum allowable amount each year to take full advantage of the tax savings. Second, invest HSA funds in growth-oriented options like mutual funds or ETFs if your account balance and risk tolerance allow. Third, pay for current medical expenses out of pocket and save receipts to reimburse yourself later, allowing your HSA funds to grow undisturbed. Finally, treat your HSA as a long-term financial tool, not just a short-term savings account, to fully leverage its triple tax advantage. By doing so, you’ll transform your healthcare spending into a strategic component of your overall financial plan.

Consequences of Insurance Lapse: Understanding Fines and Penalties for Expired Coverage

You may want to see also

Explore related products

![]()

Portability: HSAs stay with you, even if you change jobs or health plans

One of the most overlooked yet powerful features of Health Savings Accounts (HSAs) is their portability. Unlike employer-sponsored health plans or Flexible Spending Accounts (FSAs), HSAs are not tied to your job or a specific insurance provider. This means if you leave your current employer, switch jobs, or change health plans, your HSA remains yours. It’s a financial tool that moves with you, providing continuity in an otherwise fragmented healthcare landscape. For instance, if you’ve contributed $3,000 to your HSA this year and decide to switch jobs mid-year, that $3,000 stays in your account, accessible for qualified medical expenses, regardless of your new employer’s benefits package.

Consider the practical implications of this portability. If you’re in your 30s or 40s and plan to change jobs multiple times over your career, an HSA ensures your healthcare savings aren’t reset each time. This is particularly valuable for long-term financial planning. For example, funds in an HSA can be invested, allowing them to grow tax-free over decades. If you start contributing $200 monthly at age 30 and earn an average annual return of 6%, you could have over $250,000 by age 65, even with periods of job transition. This makes HSAs a rare vehicle for both short-term medical expenses and long-term wealth accumulation.

However, portability comes with responsibilities. Since the HSA is yours to manage, you must ensure contributions are made consistently, even during job transitions. If you’re between jobs, consider setting up automatic transfers from a personal bank account to maintain your savings momentum. Additionally, be mindful of eligible expenses to avoid penalties. While over-the-counter medications and menstrual care products are now HSA-eligible, items like gym memberships or cosmetic procedures are not. Keeping detailed records of expenses and receipts is essential, especially if you’re using the account across multiple employers or health plans.

A comparative analysis highlights the HSA’s edge over other healthcare savings options. FSAs, for example, are often “use-it-or-lose-it,” with funds forfeited if not spent by year-end. HSAs, on the other hand, roll over indefinitely. Similarly, while employer-sponsored plans may offer immediate convenience, they lack the long-term flexibility of an HSA. For freelancers or those in gig economy jobs, an HSA provides a stable healthcare savings mechanism, independent of inconsistent or non-existent employer benefits. This portability makes HSAs particularly appealing for younger workers who anticipate frequent career shifts or those nearing retirement who want to maximize tax-advantaged savings.

In conclusion, the portability of HSAs is a game-changer for individuals navigating today’s dynamic job market. It offers financial resilience, ensuring your healthcare savings aren’t disrupted by career changes or shifts in health coverage. By understanding and leveraging this feature, you can build a robust healthcare financial strategy that adapts to life’s transitions. Whether you’re starting your first job, switching careers, or planning for retirement, an HSA’s portability ensures your savings remain a constant in an ever-changing landscape.

Is Bristol West Insurance Legit? A Comprehensive Review and Analysis

You may want to see also

Explore related products

![]()

Investment Growth: Funds can be invested, growing tax-free for long-term healthcare savings

One of the most compelling advantages of a Health Savings Account (HSA) is its ability to serve as both a healthcare financing tool and a long-term investment vehicle. Unlike traditional savings accounts, HSAs allow account holders to invest their funds in a variety of assets, such as mutual funds, stocks, or bonds. This feature transforms the HSA from a mere parking spot for medical expenses into a dynamic growth opportunity. By investing HSA funds, individuals can harness the power of compound interest, enabling their savings to grow tax-free over time. This growth potential is particularly valuable for long-term healthcare planning, as it can outpace inflation and rising medical costs, ensuring that funds are more robust when needed in retirement or for future health expenses.

To maximize investment growth within an HSA, it’s essential to adopt a strategic approach. Start by evaluating your risk tolerance and time horizon. Younger individuals with decades until retirement may opt for more aggressive investments, such as growth-oriented mutual funds or ETFs, to capitalize on higher returns. Conversely, those nearing retirement might prefer more conservative options, like bond funds or dividend-paying stocks, to preserve capital while still achieving modest growth. Many HSA providers offer low-cost investment options, making it easier to maintain a diversified portfolio without excessive fees eroding returns. Regularly reviewing and rebalancing your portfolio ensures alignment with your financial goals and risk profile.

A key benefit of investing HSA funds is the triple tax advantage it offers: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This unique feature amplifies the impact of investment returns, as every dollar grows unencumbered by taxes. For example, if you contribute $3,000 annually to an HSA and achieve an average annual return of 7%, your account could grow to over $100,000 in 20 years, all tax-free. This makes HSAs one of the most tax-efficient investment vehicles available, particularly for those with high healthcare costs or a long-term savings horizon.

However, it’s crucial to balance investment growth with liquidity needs. While investing HSA funds can yield significant returns, ensure you maintain enough cash reserves to cover immediate medical expenses. A common strategy is to keep a portion of the HSA in a cash account for short-term needs while investing the remainder for long-term growth. Additionally, be mindful of fees associated with investment accounts, as these can eat into returns. Opt for HSA providers with low expense ratios and transparent fee structures to maximize your investment’s potential.

In conclusion, the investment growth potential of an HSA makes it a powerful tool for long-term healthcare savings. By strategically investing funds, individuals can benefit from tax-free growth, outpacing inflation and rising medical costs. Whether you’re planning for retirement or building a safety net for future health expenses, an HSA’s investment capabilities offer a unique opportunity to grow wealth while securing your healthcare future. With careful planning and a focus on diversification, an HSA can become a cornerstone of your financial strategy, blending the benefits of insurance with the rewards of investing.

Life Insurance Beneficiary Options in North Carolina

You may want to see also

Explore related products

![]()

Retirement Savings: Unused HSA funds roll over annually, aiding in retirement healthcare planning

Unused HSA funds don't vanish at year-end. Unlike FSAs, which often have "use-it-or-lose-it" rules, HSAs allow your balance to roll over indefinitely. This feature transforms your HSA into a powerful tool for long-term healthcare savings, particularly for retirement.

Imagine reaching retirement age with a substantial HSA balance. This nest egg can be used tax-free to cover Medicare premiums, out-of-pocket expenses, and even long-term care costs. It's essentially a dedicated healthcare fund, grown tax-advantaged over decades, ready to supplement your retirement income when healthcare needs typically increase.

The beauty lies in the triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This compounding effect can significantly boost your retirement healthcare savings. For instance, a 30-year-old contributing $3,000 annually to an HSA with a 7% average annual return could accumulate over $300,000 by age 65, providing a substantial cushion for future healthcare needs.

However, maximizing this benefit requires strategic planning. Start contributing early and consistently. Even small, regular contributions can grow substantially over time. Consider investing your HSA funds for potentially higher returns, but be mindful of risk tolerance and time horizon. Finally, resist the urge to spend HSA funds on non-medical expenses before retirement, as this forfeits the tax advantages and diminishes your long-term savings potential.

Custom Whole Life Insurance: Tax Documents Required?

You may want to see also

Frequently asked questions

An HSA (Health Savings Account) is a tax-advantaged savings account paired with a high-deductible health plan (HDHP). It allows you to save pre-tax dollars for qualified medical expenses, reducing taxable income. The funds grow tax-free and can be used for current or future healthcare costs, making it a flexible and cost-effective way to manage healthcare expenses alongside insurance.

HSAs are typically paired with HDHPs, which generally have lower monthly premiums compared to traditional health insurance plans. The savings on premiums can offset the higher deductible, and the HSA allows you to set aside funds for out-of-pocket costs, making healthcare more affordable overall.

Yes, HSA funds can be used for a wide range of qualified medical expenses, including deductibles, copays, prescriptions, dental, and vision care, even if they are not covered by your insurance plan. This flexibility ensures you can address healthcare needs beyond what your insurance covers.