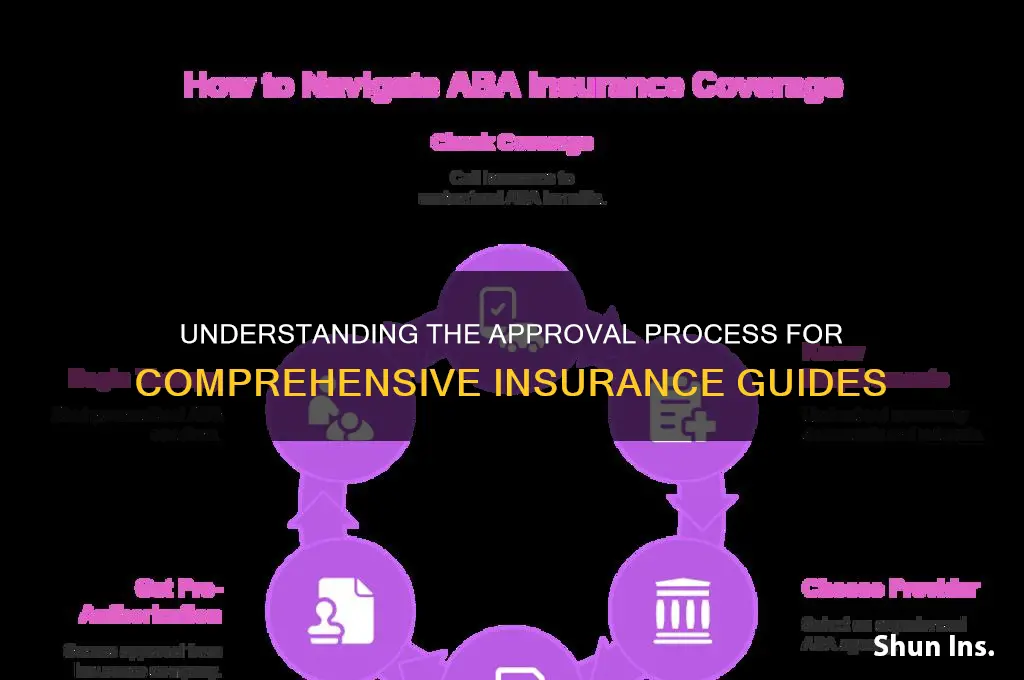

The approval process for an insurance guide is a meticulous and regulated procedure designed to ensure accuracy, compliance, and clarity for policyholders. Typically, insurance guides are developed by insurance companies or industry experts and must adhere to strict guidelines set by regulatory bodies such as state insurance departments or federal agencies. The process begins with drafting the guide, incorporating essential information about policies, coverage details, claims procedures, and legal requirements. Once drafted, the guide undergoes internal reviews by legal and compliance teams to verify its alignment with current laws and regulations. Subsequently, it is submitted to the relevant regulatory authority for external approval, where it is scrutinized for completeness, transparency, and fairness. Upon approval, the guide is officially authorized for distribution, providing consumers with a reliable resource to understand their insurance options and rights. This rigorous process ensures that insurance guides serve as trustworthy tools for informed decision-making.

Explore related products

What You'll Learn

- Regulatory Compliance: Ensuring adherence to legal standards and industry regulations for guide approval

- Content Accuracy: Verifying factual correctness and clarity in the insurance guide

- Internal Review: Approval process by company experts and stakeholders

- External Validation: Third-party review for impartial assessment and credibility

- Final Sign-Off: Executive or regulatory authority approval to publish the guide

![]()

Regulatory Compliance: Ensuring adherence to legal standards and industry regulations for guide approval

Regulatory compliance is the backbone of any insurance guide approval process, ensuring that the information provided is not only accurate but also legally sound. In the United States, for instance, insurance guides must adhere to regulations set by the Federal Trade Commission (FTC) and state insurance departments. These bodies require that guides clearly disclose policy terms, exclusions, and consumer rights, using plain language to avoid confusion. Failure to comply can result in hefty fines, legal action, or loss of credibility. For example, a guide that omits mandatory disclosures about cancellation policies may be deemed non-compliant, jeopardizing its approval.

To navigate this complex landscape, start by identifying the specific regulations applicable to your jurisdiction. In the European Union, the Insurance Distribution Directive (IDD) mandates that guides provide transparent information about products and intermediaries. Similarly, in Australia, the Australian Securities and Investments Commission (ASIC) requires guides to include key facts sheets (KFS) for life insurance products. Once you’ve pinpointed the relevant laws, conduct a gap analysis to ensure your guide meets all legal requirements. Tools like compliance checklists or legal review software can streamline this process, reducing the risk of oversight.

A persuasive argument for prioritizing regulatory compliance is its role in building consumer trust. When a guide aligns with legal standards, it signals to readers that the information is reliable and their interests are protected. For instance, a guide that clearly outlines the cooling-off period—typically 10 to 30 days, depending on the region—empowers consumers to make informed decisions. Conversely, non-compliant guides can lead to mistrust and disputes, damaging both the insurer’s reputation and the consumer’s experience. Thus, compliance is not just a legal obligation but a strategic investment in customer satisfaction.

Comparatively, the approval process for insurance guides varies significantly across industries and regions. While health insurance guides in the U.S. must comply with the Affordable Care Act (ACA), auto insurance guides in the UK are governed by the Financial Conduct Authority (FCA). Despite these differences, a common thread is the emphasis on transparency and fairness. For practical implementation, consider adopting a layered approach: first, ensure core compliance with mandatory disclosures; second, incorporate industry best practices; and third, include optional enhancements like FAQs or case studies to improve readability. This tiered strategy balances legal requirements with user engagement.

In conclusion, regulatory compliance is a non-negotiable aspect of insurance guide approval, demanding meticulous attention to detail and a proactive approach. By understanding and adhering to legal standards, insurers not only avoid penalties but also foster trust and clarity for their audience. Whether you’re drafting a guide for life, health, or property insurance, the principles remain the same: know the rules, apply them rigorously, and communicate transparently. After all, a compliant guide is not just a legal document—it’s a tool for empowering consumers to make confident, informed choices.

Life Insurance License: Misdemeanor Impact in Florida

You may want to see also

Explore related products

![]()

Content Accuracy: Verifying factual correctness and clarity in the insurance guide

Ensuring content accuracy in an insurance guide is paramount, as even minor errors can lead to misunderstandings, financial losses, or legal repercussions. To verify factual correctness, start by cross-referencing all data against primary sources such as regulatory documents, industry reports, and official statistics. For instance, when discussing policy coverage limits, confirm the figures with the latest updates from the Insurance Information Institute or relevant government bodies. Avoid relying solely on secondary sources, as they may contain inaccuracies or outdated information.

Clarity is equally critical, as insurance terminology can be complex and confusing for the average reader. To enhance comprehension, break down technical terms into plain language and provide real-world examples. For example, instead of merely stating that a policy has a "$500 deductible," explain that this means the policyholder must pay the first $500 of a claim out of pocket before the insurer covers the remaining costs. Use bullet points or tables to organize information logically, ensuring that key details are easy to locate and understand.

A structured review process is essential for maintaining accuracy and clarity. Begin with an internal review by subject matter experts who can identify gaps or inconsistencies. Follow this with an external review by legal and compliance teams to ensure adherence to industry regulations and standards. For instance, if the guide mentions tax benefits for certain policies, verify that the claims align with the latest IRS guidelines. Additionally, consider user testing with a sample audience to gauge readability and identify areas of confusion.

Practical tools can streamline the verification process. Grammar and spell-check software like Grammarly can catch minor errors, while fact-checking platforms such as FactCheck.org can help validate claims. For complex topics, consult industry experts or legal advisors to ensure precision. For example, when discussing health insurance exclusions for pre-existing conditions, consult the Affordable Care Act’s provisions to provide accurate, up-to-date information. Regularly updating the guide to reflect policy changes or new regulations is also crucial, as outdated content can mislead readers.

Finally, transparency builds trust with your audience. Include a disclaimer that outlines the guide’s limitations and encourages readers to consult their insurance provider for personalized advice. For instance, a disclaimer might state, “This guide provides general information and should not be considered legal or financial advice. Always review your policy documents or speak with an agent for specific details.” By prioritizing accuracy, clarity, and transparency, your insurance guide will serve as a reliable resource that empowers readers to make informed decisions.

Life Insurance and Self-Directed 401(k)s: What You Need to Know

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UY218_.jpg)

![]()

Internal Review: Approval process by company experts and stakeholders

Internal review is the backbone of ensuring an insurance guide’s accuracy, compliance, and relevance before it reaches the public. This stage involves a meticulous evaluation by company experts and stakeholders, each bringing unique perspectives to the table. Actuaries scrutinize the financial models and risk assessments to ensure the guide’s recommendations are actuarially sound. Legal teams comb through the content to identify potential liabilities and ensure compliance with regulatory frameworks, such as the Affordable Care Act or GDPR, depending on the jurisdiction. Underwriters assess the practicality of the guide’s advice in real-world scenarios, while customer service representatives provide insights into common client pain points and questions. This multidisciplinary approach ensures the guide is not only technically correct but also user-friendly and aligned with the company’s strategic goals.

The approval process begins with a draft submission to a designated internal committee, often comprising representatives from these key departments. The committee reviews the guide against predefined criteria, such as clarity, completeness, and adherence to industry standards. For instance, a life insurance guide might be evaluated for its treatment of exclusions, waiting periods, and beneficiary designations. During this phase, feedback is collected in a structured format—annotated comments, scoring rubrics, or checklists—to ensure consistency. High-stakes issues, like misstated coverage limits or ambiguous policy explanations, are flagged for immediate revision. This step is critical because even minor errors can lead to costly claims or reputational damage.

One practical tip for streamlining internal reviews is to establish clear roles and timelines from the outset. For example, actuaries might have 5 business days to verify premium calculations, while legal teams focus on compliance within a 7-day window. Stakeholders should also be encouraged to provide actionable feedback, such as “Rewrite Section 3.2 to clarify that pre-existing conditions are covered after a 12-month waiting period,” rather than vague comments like “This is confusing.” Tools like collaborative platforms (e.g., Microsoft Teams or Asana) can facilitate real-time communication and version control, reducing the risk of conflicting edits.

A common pitfall in internal reviews is over-reliance on a single department’s perspective, which can lead to imbalanced content. For instance, a guide dominated by legal input might become overly technical and inaccessible to the average consumer. To mitigate this, companies should adopt a weighted scoring system where feedback from customer-facing teams carries equal importance to that of technical experts. Pilot testing the guide with a small focus group of policyholders can also provide invaluable insights into readability and practical utility. This hybrid approach ensures the guide resonates with both internal standards and external needs.

Ultimately, the internal review process is a collaborative effort that transforms a draft into a trusted resource. By leveraging the diverse expertise of company stakeholders and adhering to structured protocols, organizations can produce insurance guides that are not only compliant but also genuinely helpful. The takeaway is clear: internal review is not a bureaucratic hurdle but a strategic investment in quality and credibility. When executed effectively, it ensures the guide stands up to scrutiny from regulators, competitors, and, most importantly, the customers it aims to serve.

Gender Gap in Insurance: Do Men Receive Better Coverage Than Women?

You may want to see also

Explore related products

![]()

External Validation: Third-party review for impartial assessment and credibility

Third-party reviews serve as a cornerstone for establishing the credibility of an insurance guide, offering an impartial lens that internal assessments cannot provide. These external validators, often industry experts, regulatory bodies, or independent auditors, scrutinize the guide’s accuracy, relevance, and compliance with legal standards. For instance, a guide on life insurance policies might be reviewed by the Insurance Regulatory and Development Authority (IRDA) in India or the Financial Conduct Authority (FCA) in the UK. Such endorsements signal to consumers that the information is reliable and adheres to industry best practices, fostering trust in an otherwise complex and often opaque sector.

The process of securing third-party validation involves more than just submitting a document for review. It requires a structured approach: first, identify reputable organizations or experts with authority in the insurance domain. Second, tailor the guide to meet their evaluation criteria, which may include clarity of language, comprehensiveness of coverage, and alignment with current regulations. Third, engage transparently, addressing any concerns or gaps highlighted during the review. For example, a guide targeting seniors might be reviewed by AARP to ensure it addresses age-specific needs, such as long-term care options or premium affordability for retirees.

While third-party reviews enhance credibility, they are not without challenges. The cost and time involved can be significant, particularly for smaller organizations. Additionally, reviewers may have differing priorities, leading to conflicting feedback. To mitigate this, prioritize validators whose expertise aligns closely with the guide’s target audience. For instance, a guide on health insurance for millennials might benefit from review by digital health platforms or consumer advocacy groups, ensuring it resonates with tech-savvy, cost-conscious readers.

The ultimate takeaway is that external validation is an investment in long-term trust and authority. A guide endorsed by respected third parties not only stands out in a crowded market but also serves as a protective measure against misinformation. For consumers, seeing a seal of approval from a trusted entity simplifies decision-making, reducing the cognitive load of deciphering complex insurance jargon. For creators, it reinforces the guide’s position as a go-to resource, driving engagement and loyalty. In a field where transparency is often questioned, third-party reviews are not just beneficial—they are essential.

Demerit Points and Insurance: How Traffic Violations Impact Your Premiums

You may want to see also

Explore related products

![]()

Final Sign-Off: Executive or regulatory authority approval to publish the guide

Executive approval is the final gatekeeper before an insurance guide reaches the public. This step ensures the document aligns with the company's strategic goals, complies with legal requirements, and maintains brand integrity. Executives scrutinize the guide for accuracy, clarity, and consistency, often cross-referencing it with internal policies and external regulations. For instance, a life insurance guide must reflect the latest tax implications and beneficiary rules, which an executive would verify against IRS guidelines. Without this sign-off, even the most well-crafted guide remains shelved, underscoring the critical role of leadership in the approval process.

Regulatory authorities often require their own approval for insurance guides, particularly in highly regulated markets like healthcare or auto insurance. This step involves submitting the guide to agencies such as the Department of Insurance or the Financial Conduct Authority for review. These bodies assess whether the guide provides fair, transparent, and non-misleading information to consumers. For example, a health insurance guide must clearly outline coverage limits, exclusions, and claim procedures, adhering to the Affordable Care Act’s standards. Failure to secure regulatory approval can result in fines, legal action, or reputational damage, making this step non-negotiable.

Practical tips for navigating final sign-off include creating a checklist of executive and regulatory requirements early in the drafting process. This ensures the guide is built to meet these standards from the outset, reducing revision cycles. For instance, if an executive prioritizes alignment with the company’s ESG (Environmental, Social, Governance) goals, integrate these themes into the guide’s examples and case studies. Similarly, if a regulator requires specific disclaimers, draft these in advance and highlight them for reviewers. Proactive preparation not only expedites approval but also demonstrates respect for the authority’s time and expertise.

A comparative analysis reveals that while executive approval focuses on internal alignment and strategic fit, regulatory approval emphasizes external compliance and consumer protection. Executives may push for innovative language or marketing angles, whereas regulators demand precision and conservatism. For example, an executive might approve a statement like “Our policy offers unparalleled peace of mind,” but a regulator could flag it as unsubstantiated. Balancing these perspectives requires diplomacy and a willingness to revise. Ultimately, the guide must satisfy both audiences, ensuring it is both compelling and compliant.

In conclusion, final sign-off is a dual-layered process that demands meticulous attention to detail and strategic foresight. Executives and regulators serve as complementary filters, each addressing distinct but equally vital aspects of the guide’s readiness for publication. By understanding their priorities and preparing accordingly, creators can streamline this stage, ensuring the guide not only meets but exceeds expectations. This final approval is not just a formality—it’s the stamp of authority that transforms a draft into a trusted resource for consumers.

A Comprehensive Guide to Buying E&O Insurance for Your Business

You may want to see also

Frequently asked questions

The approval process for an insurance guide typically involves submission to regulatory bodies or industry authorities, who review the content for accuracy, compliance with laws, and clarity. Once reviewed, it is either approved, requires revisions, or is rejected.

Regulatory agencies, such as state insurance departments or federal bodies like the National Association of Insurance Commissioners (NAIC), are responsible for approving insurance guides to ensure they meet legal and industry standards.

The approval timeline varies depending on the complexity of the guide and the regulatory body's workload. It can take anywhere from a few weeks to several months.

An insurance guide must be accurate, transparent, compliant with relevant laws and regulations, and free of misleading information. It should also be written in clear, understandable language for the intended audience.