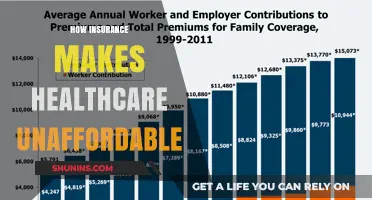

Insurance premiums are experiencing a significant surge, with many policyholders facing increases of up to $2000 annually. This steep rise is attributed to a combination of factors, including escalating healthcare costs, more frequent and severe natural disasters, and rising inflation. Insurers are passing these increased expenses onto consumers, leaving many households struggling to afford essential coverage. As a result, individuals and families are being forced to reevaluate their budgets and seek alternative options to manage these higher costs, while policymakers and industry experts grapple with finding sustainable solutions to this growing financial burden.

| Characteristics | Values |

|---|---|

| Average Annual Increase in Car Insurance Premiums (2023) | $200 - $500 (varies by state and provider) |

| Factors Contributing to $2000 Increase | Accumulation of smaller annual increases over multiple years |

| Primary Drivers of Premium Increases | Increased vehicle repair costs, rising medical costs after accidents, more frequent and severe weather events, supply chain disruptions |

| Impact of Inflation | Inflation drives up costs across the board, including parts, labor, and medical care |

| State-Specific Variations | Some states experience higher increases due to local factors like accident rates, theft, and natural disasters |

| Individual Factors Affecting Premiums | Driving record, age, vehicle type, coverage level, claims history |

| Projected Future Trends | Premiums are expected to continue rising due to ongoing economic and environmental factors |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- Economic Inflation Impact: Rising costs of healthcare, repairs, and claims drive insurance premiums upward significantly

- Natural Disasters Frequency: Increased hurricanes, floods, and wildfires lead to higher property and casualty insurance rates

- Medical Cost Surge: Expensive treatments and drugs push health insurance premiums up by large amounts

- Regulatory Changes: New laws and compliance requirements force insurers to raise policy costs substantially

- Supply Chain Disruptions: Higher material and labor costs increase auto and home insurance premiums sharply

![]()

Economic Inflation Impact: Rising costs of healthcare, repairs, and claims drive insurance premiums upward significantly

The surge in insurance premiums, often by $2000 or more, isn’t arbitrary—it’s a direct response to economic inflation. Healthcare costs, for instance, have skyrocketed due to advanced medical technologies and longer hospital stays. A single MRI scan now averages $2,611, up from $1,800 a decade ago, while prescription drug prices have risen 33% since 2015. Insurers, forced to cover these escalating expenses, pass the burden onto policyholders. Similarly, auto repair costs have jumped 40% in the past five years due to sophisticated vehicle components and labor shortages, driving up collision coverage premiums. This inflationary spiral isn’t just a number—it’s a reflection of systemic economic pressures reshaping the insurance landscape.

Consider the claims environment, which has grown increasingly volatile. Natural disasters, exacerbated by climate change, have led to record-breaking payouts. In 2023, insurers paid out $135 billion in catastrophe claims, a 25% increase from 2020. These losses aren’t absorbed silently; they’re offset by higher premiums for homeowners and renters. For example, in fire-prone regions like California, premiums have surged by $2,500 annually for average policies. Even seemingly minor claims, like water damage repairs, now cost 50% more due to inflated material and labor costs. Insurers aren’t profiteering—they’re recalibrating to survive in an era of unpredictable, high-cost claims.

To mitigate these increases, policyholders must become proactive. Start by reviewing your coverage limits annually; over-insuring can unnecessarily inflate premiums. For health insurance, consider high-deductible plans paired with Health Savings Accounts (HSAs) to offset costs. Auto policyholders should inquire about telematics programs, which can reduce premiums by up to 30% for safe drivers. Homeowners can invest in preventative measures like storm shutters or smart leak detectors, potentially qualifying for discounts. While these steps won’t reverse inflation, they can soften its impact on your wallet.

Comparatively, the insurance industry’s response to inflation mirrors broader economic trends. Just as wages struggle to keep pace with rising living costs, insurers are caught between rising expenses and consumer affordability. Unlike other sectors, however, insurance operates on a predictive model, requiring premiums to account for future risks. This forward-looking approach means today’s increases are less about current costs and more about anticipated challenges. For instance, cyber insurance premiums have doubled in the past two years due to the projected rise in ransomware attacks, even if a policyholder hasn’t filed a claim. This proactive pricing strategy, while frustrating, ensures the industry’s solvency in an uncertain future.

Ultimately, the $2000 premium hike isn’t a random fee—it’s a symptom of interconnected economic forces. Healthcare inflation, repair cost surges, and volatile claims environments are driving insurers to recalibrate their models. While policyholders bear the brunt, understanding these factors empowers smarter decision-making. Whether through policy adjustments, preventative measures, or alternative coverage options, navigating this new reality requires both awareness and action. Inflation may be inevitable, but its impact on your insurance costs doesn’t have to be uncontested.

Travelers' Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Natural Disasters Frequency: Increased hurricanes, floods, and wildfires lead to higher property and casualty insurance rates

The escalating frequency and intensity of natural disasters—hurricanes, floods, and wildfires—are reshaping the insurance landscape. In 2023, the U.S. experienced 25 separate billion-dollar weather and climate disasters, a record high. These events don’t just destroy homes and businesses; they force insurers to recalibrate their risk models. For instance, in California, wildfire-prone areas have seen premiums spike by $2,000 or more annually as insurers factor in the growing likelihood of total loss. This isn’t an isolated trend—it’s a nationwide shift driven by climate change, and policyholders are footing the bill.

Consider the mechanics of insurance pricing. Insurers rely on historical data to predict future claims, but when disasters become more frequent, that data becomes obsolete. In Florida, hurricane claims have surged 50% in the past decade, prompting insurers to raise rates by an average of $1,800 per policyholder. Similarly, flood insurance premiums in Louisiana have jumped by $2,200 in high-risk zones, as FEMA’s National Flood Insurance Program adjusts to repeated inundations. These increases aren’t arbitrary—they’re a direct response to the rising cost of rebuilding after catastrophic events.

For homeowners, the financial strain is palpable. Take the case of a family in Colorado, where wildfires have become a near-annual threat. Their annual premium rose from $1,500 to $3,700 in just three years, reflecting the insurer’s assessment of heightened risk. To mitigate costs, some are opting for higher deductibles or dropping coverage altogether—a risky move in an era of unpredictable disasters. Renters aren’t immune either; landlords often pass on increased property insurance costs through higher rents, indirectly inflating living expenses.

What can policyholders do? First, assess your risk profile. If you live in a floodplain, wildfire zone, or hurricane-prone area, invest in mitigation measures like storm shutters, fire-resistant roofing, or elevated foundations. These improvements can reduce premiums by up to 20%. Second, shop around. Some insurers offer discounts for bundling policies or installing smart home devices that detect leaks or fires early. Finally, consider government programs like FEMA’s flood insurance or state-backed wildfire funds, though these too are adjusting rates upward in response to growing claims.

The takeaway is clear: as natural disasters become the new normal, insurance is no longer a static expense. Policyholders must adapt by understanding their risks, investing in prevention, and exploring all available options. Ignoring these trends could leave you underinsured—or worse, priced out of coverage entirely. The $2,000 increase isn’t just a number; it’s a warning sign of a future where protection comes at a premium.

Insurance Investigators: What Are They Hiding?

You may want to see also

Explore related products

![]()

Medical Cost Surge: Expensive treatments and drugs push health insurance premiums up by large amounts

The rising cost of medical treatments and prescription drugs is a significant driver behind the steep increase in health insurance premiums, often by $2,000 or more annually. For instance, a single dose of gene therapy for rare diseases like spinal muscular atrophy (SMA) can cost upwards of $2.1 million, while specialty drugs for chronic conditions like rheumatoid arthritis or cancer can run $50,000 to $100,000 per year. Insurers, faced with these escalating expenses, pass the burden onto policyholders through higher premiums, deductibles, and copays. This trend disproportionately affects individuals and families with employer-sponsored plans, where annual premium increases outpace wage growth, squeezing household budgets.

Consider the case of a 45-year-old with Type 2 diabetes, a condition affecting over 34 million Americans. Monthly prescriptions for insulin, metformin, and SGLT2 inhibitors can total $600 or more, even with insurance. When insurers negotiate drug prices with pharmaceutical companies, they often fail to secure discounts that offset the drugs’ list prices, leading to higher claims costs. These costs are then spread across the insured pool, resulting in premium hikes. For example, a family plan might see a $2,000 increase annually due to the collective impact of such high-cost claims.

To mitigate these increases, consumers can take proactive steps. First, review your plan’s formulary annually to ensure your medications are covered at the lowest tier. If not, ask your doctor about therapeutic alternatives or generic options. For instance, switching from brand-name insulin (e.g., Lantus) to a biosimilar version can save hundreds of dollars monthly. Second, explore health savings accounts (HSAs) or flexible spending accounts (FSAs) to pay for out-of-pocket costs with pre-tax dollars. Finally, consider high-deductible health plans (HDHPs) paired with an HSA, which often have lower premiums but require careful budgeting for potential medical expenses.

A comparative analysis reveals that countries with single-payer systems or robust price controls, like Canada or the UK, experience slower premium growth than the U.S. For example, Canada spends roughly 11% of its GDP on healthcare, compared to 18% in the U.S., yet achieves comparable health outcomes. While systemic reform remains a distant goal, policymakers could cap drug price increases or allow Medicare to negotiate prices directly, potentially slowing premium growth. Until then, individuals must navigate this complex landscape by advocating for themselves and leveraging available tools to manage costs.

The takeaway is clear: expensive treatments and drugs are not just a healthcare issue—they’re a financial one. Without intervention, premiums will continue to rise, eroding affordability and access. By understanding the drivers of these increases and taking strategic action, individuals can soften the blow, but broader solutions are needed to address the root causes of this unsustainable trend.

SORN Requirements: Must You Declare Off-Road Vehicles Without Insurance?

You may want to see also

Explore related products

![]()

Regulatory Changes: New laws and compliance requirements force insurers to raise policy costs substantially

Regulatory changes are a significant driver behind the steep increases in insurance premiums, often adding hundreds or even thousands of dollars to annual costs. New laws and compliance requirements mandate insurers to adjust their policies, covering additional risks or enhancing consumer protections. For instance, recent legislation in several states now requires insurers to include comprehensive mental health coverage, a shift that, while beneficial for policyholders, necessitates higher premiums to offset the expanded benefits. Similarly, stricter environmental regulations force insurers to account for climate-related risks, such as flood or wildfire damage, which were previously excluded or underpriced. These changes, though necessary, directly contribute to the substantial rise in policy costs.

Consider the impact of medical malpractice insurance, where regulatory reforms have tightened liability standards. Insurers are now required to provide higher coverage limits to protect against larger settlements, a change spurred by legislative efforts to safeguard patients. This adjustment alone can increase premiums by $1,500 to $2,000 annually for healthcare providers, who often pass these costs onto consumers through higher service fees. Similarly, auto insurance premiums have surged due to laws mandating lower blood alcohol limits for drivers, which insurers interpret as increased risk, leading to higher rates. These examples illustrate how regulatory changes, while aimed at public welfare, create a ripple effect that elevates insurance costs.

To navigate these increases, policyholders should proactively review their coverage and explore options to mitigate the financial impact. For instance, bundling policies or increasing deductibles can offset some of the added costs. Additionally, staying informed about pending legislation can provide foresight into potential premium hikes, allowing individuals to budget accordingly. Insurers, on the other hand, must balance compliance with affordability, often investing in technology to streamline operations and reduce administrative costs. However, such measures rarely fully counteract the financial burden of new regulations, leaving premium increases as the primary solution.

A comparative analysis reveals that regions with fewer regulatory changes tend to experience slower premium growth. For example, states with minimal updates to healthcare or auto insurance laws have seen average increases of $300 to $500, compared to $2,000 or more in states with extensive reforms. This disparity underscores the direct correlation between regulatory activity and insurance costs. While some argue that these changes are essential for consumer protection and risk management, others contend that they disproportionately affect low-income individuals, who may struggle to afford the higher premiums. Striking a balance between regulation and affordability remains a challenge for policymakers and insurers alike.

In conclusion, regulatory changes are a critical yet often overlooked factor in the rising cost of insurance. By mandating broader coverage, stricter liability standards, and enhanced consumer protections, these reforms force insurers to recalibrate their pricing models, resulting in substantial premium increases. While such changes aim to improve safety and fairness, they also highlight the need for innovative solutions to manage costs without compromising quality. For policyholders, understanding the link between regulation and premiums is the first step toward making informed decisions in an increasingly complex insurance landscape.

AARP Life Insurance: Registration Process Simplified

You may want to see also

Explore related products

![]()

Supply Chain Disruptions: Higher material and labor costs increase auto and home insurance premiums sharply

The global supply chain crisis has triggered a ripple effect, pushing material and labor costs to unprecedented heights. Steel prices, for instance, surged by over 200% between 2020 and 2022, while lumber costs fluctuated wildly, peaking at $1,700 per thousand board feet in 2021. These increases directly impact the cost of repairing or replacing vehicles and homes, forcing insurers to recalibrate their premiums. For homeowners, this means a $500 to $1,200 annual increase, depending on location and coverage. Auto insurance premiums have risen by an average of $300 to $800, with luxury vehicle owners seeing even steeper hikes due to the specialized materials required for repairs.

Consider the case of a 35-year-old homeowner in Texas whose annual premium jumped from $1,800 to $2,800 in 2023. The insurer cited a 40% increase in construction material costs and a 25% rise in labor expenses as the primary drivers. Similarly, a 45-year-old driver in California saw their auto insurance premium rise by $600 after a minor accident, as the cost of replacement parts had skyrocketed. These examples illustrate how supply chain disruptions are translating into tangible financial burdens for policyholders.

To mitigate these increases, policyholders can take proactive steps. First, review your policy annually to ensure you’re not over-insured. For instance, if your car is older than 10 years, consider dropping comprehensive coverage, which could save you $200 to $400 annually. Second, bundle auto and home insurance policies with the same provider, often yielding discounts of 10% to 25%. Third, invest in preventive measures like home security systems or safe driving courses, which can reduce premiums by $100 to $300 per year.

Comparatively, the impact of supply chain disruptions on insurance premiums is more severe than inflationary pressures alone. While general inflation has hovered around 6% to 8%, insurance premiums have outpaced this, rising by 12% to 18% in some regions. This disparity highlights the unique vulnerability of the insurance sector to global supply chain issues. Unlike other industries, insurers cannot easily absorb these costs, as their pricing models are tightly regulated and based on historical data that no longer reflects current realities.

In conclusion, supply chain disruptions are a critical yet often overlooked factor in the sharp rise of auto and home insurance premiums. By understanding the specific drivers—such as material and labor cost increases—policyholders can make informed decisions to manage their expenses. While insurers work to adjust their models, individuals must take proactive steps to minimize the financial impact, ensuring they remain adequately covered without overpaying.

Mastering the P&C Insurance Exam: Proven Strategies for Success

You may want to see also

Frequently asked questions

Insurance premiums can increase due to factors like rising healthcare costs, inflation, increased claims in your area, changes in coverage, or updates to your personal risk profile.

A $2000 increase is significant and not typical for everyone. It often reflects specific circumstances, such as major changes in your policy, high claims activity, or broader industry trends affecting costs.

Yes, you can explore options like adjusting your coverage limits, increasing deductibles, bundling policies, shopping around for better rates, or qualifying for discounts to potentially lower your premium.

Not necessarily. Future increases depend on ongoing factors like inflation, claims history, and industry trends. Reviewing your policy annually and staying informed can help manage costs.