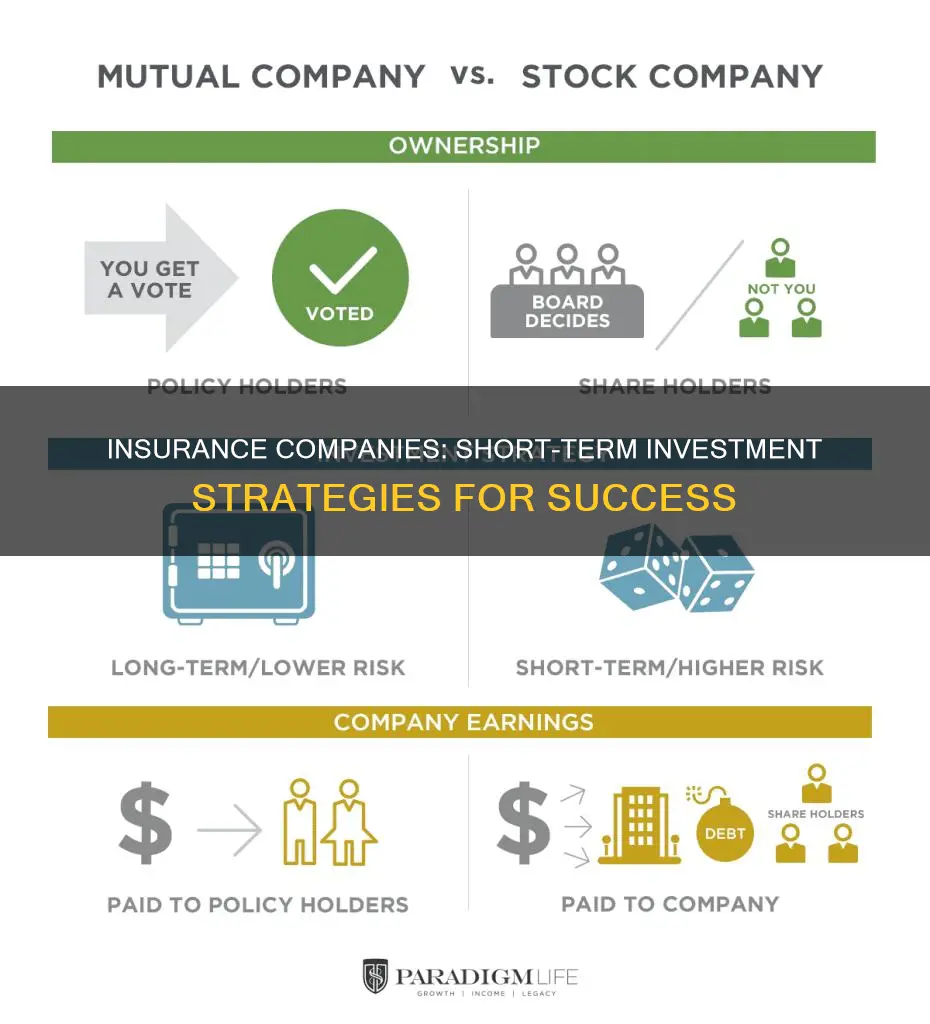

Insurance companies make money by charging premiums to their customers and investing these payments in short-term, interest-generating assets. They also invest in riskier assets when rates fall to maintain their earnings forecast. Insurance-cum-investment plans are also becoming popular as they offer a two-in-one benefit of protection and wealth creation for the policyholder. In addition, life insurance policies can be used as investment vehicles, although they may not be the best choice for everyone.

| Characteristics | Values |

|---|---|

| Type of insurance | Health, auto, property, life insurance |

| Investment type | High-yield savings accounts, money market funds, certificates of deposit, treasury bills, ultra-short-term bond ETFs, stocks, bonds, blue-chip stocks |

| Investment income | Smaller than underwriting revenue |

| Risk | Low-rate environments can lead to riskier investments |

| Reinsurance | Insurance that insurance companies buy to protect themselves from excessive losses |

| Liquidity | High |

| Tax | Tax benefits, e.g. Section 80C, 10 (10D) and 80D in India |

| Premium payment | Single premium for 5-10 years of coverage |

| Returns | Solid long-term returns |

Explore related products

What You'll Learn

![]()

Insurance-cum-investment plans

One advantage of insurance-cum-investment plans is their flexibility. Investors can switch between different funds based on their risk tolerance and investment objectives. Additionally, these plans can be tailored to meet specific goals, such as child plans designed for long-term objectives like education or marriage, which often combine investment growth with life insurance coverage for the parent. The waiver of premium feature in child plans ensures that the policy continues even if the parent dies or becomes disabled, protecting the child's future.

When considering insurance-cum-investment plans, it is important to evaluate both short-term and long-term objectives. These plans may not be suitable for everyone, and investors should carefully assess their financial goals, risk tolerance, and investment timeline before making a decision. While insurance-cum-investment plans offer the convenience of combined protection and wealth creation, investors need to weigh their options and select the right plan to meet their specific needs.

In terms of how insurance companies make money from these plans, it primarily involves charging premiums to the insured and investing the premium payments. Insurance companies invest in short-term, safe investments to generate additional interest revenue while waiting for potential claim payouts. They aim to price the risk effectively, generating more revenue in premiums than is spent on claim payouts. By investing a portion of the premiums, insurance companies can increase their income, although investment income is typically smaller than underwriting revenue.

Root Insurance: Saving Money or Not?

You may want to see also

Explore related products

![]()

Short-term lock-in features

Insurance companies make money through premiums and investing these payments. They invest the premiums in interest-generating assets. The revenue model varies among different types of insurance, including auto, health, and property insurance. However, the insurance industry generally operates by assuming a customer's financial risk and transferring it to the insurer.

Insurance companies often look for safe, short-term investments to generate additional interest revenue while waiting for potential claim payouts. These short-term investments include high-yield savings accounts, money market funds, certificates of deposit, treasury bills, and ultra-short-term bond ETFs.

While short-term lock-in features offer the benefit of shorter commitment periods, it's important to consider the trade-offs. Shorter lock-in periods may result in lower returns compared to long-term investments, and they may not always provide the most competitive interest rates.

Additionally, when evaluating short-term lock-in features, it's crucial to consider the specific terms and conditions of the insurance plan. Different insurers may have varying provisions regarding premium payment frequency, maturity benefits, and waiver options in the event of unforeseen circumstances.

Navigating Mercury Insurance: The Benefits of Engaging a Private Adjuster

You may want to see also

Explore related products

![]()

Premium payment frequency

The choice between these options depends on various factors, including the policyholder's preference, liquidity, and opportunity costs. While less frequent premium payments, such as annual or semi-annual payments, may result in discounted rates and lower total costs, they require larger sums of money to be paid at once. On the other hand, more frequent premium payments, such as monthly or quarterly payments, may be more convenient for budgeting and ensuring timely payments, but they often come with a higher total cost.

It is worth noting that some insurance companies may charge higher premiums for more frequent payment options to compensate for the additional administrative costs associated with processing multiple smaller payments. Additionally, policyholders should be mindful of the potential for higher overall expenses with more frequent payments, even though each individual payment may seem more manageable.

The flexibility of premium payment frequency allows policyholders to choose an option that aligns with their financial situation and preferences. For example, individuals with stable incomes and sufficient savings may opt for annual or semi-annual payments to take advantage of potential discounts. In contrast, those with more variable incomes or those who prefer smaller, more frequent payments may choose monthly or quarterly options.

It is important to carefully review the terms and conditions of the insurance policy, as well as the potential impact on overall costs, before selecting a premium payment frequency. Policyholders should also be aware that changing the frequency of premium payments during the life of the policy may be possible, but it is best to consult with the insurance provider to understand the specific implications and any associated costs.

The Path to Becoming an Independent Insurance Adjuster: A Comprehensive Guide

You may want to see also

Explore related products

$19.95 $24.95

![]()

Reinsurance

In the context of insurance companies, investing in reinsurance can help them manage their risk exposure and protect their solvency. By transferring a portion of their risk to reinsurers, insurance companies can reduce the potential impact of excessive claim payouts. This, in turn, allows them to maintain their financial stability and fulfill their obligations to policyholders.

In summary, reinsurance plays a crucial role in the insurance industry by providing a mechanism for insurers to manage their risk exposure and protect their financial stability. By investing in reinsurance, insurance companies can safeguard themselves from excessive losses and ensure they remain solvent even in the face of catastrophic events or an unusually high number of claims.

**Insurance Adjusters: Dressing to Impress and Projecting Professionalism**

You may want to see also

Explore related products

![]()

Risk pricing

Actuaries play a crucial role in risk pricing by evaluating risks and setting premium rates. They draw on industry experience and academic research to connect theory to real-world practice. This includes assessing the performance of business units, evaluating risk transfer options, and optimizing portfolio mix. Effective risk pricing ensures that insurance companies generate more revenue from premiums than they spend on claim payouts.

If an insurance company prices its risk too low, it risks losing money if a claim is filed. On the other hand, if the company prices its risk too high, it may lose prospective clients to competitors. Therefore, accurate risk pricing is essential for the financial stability and competitiveness of an insurance company.

Insurance companies often seek safe, short-term investments to generate interest revenue while waiting for potential claim payouts. These investments provide additional income to complement the revenue generated from premiums. By investing in relatively conservative assets, such as bonds or stable blue-chip stocks, insurance companies can pad their top and bottom lines.

In summary, risk pricing is a critical function in the insurance industry, involving the assessment and pricing of risks to ensure profitability and sustainability. Effective risk pricing balances the need to generate revenue and remain competitive in the market.

The Dynamic Nature of Revocable Orthodontic Retainer Adjustments: An Insurance Perspective

You may want to see also

Frequently asked questions

Insurance companies make money in the short term by investing the premiums they receive from customers. They invest in short-term, interest-generating assets while waiting for potential claim payouts.

Examples of short-term investments include high-yield savings accounts, money market funds, certificates of deposit, treasury bills, and ultra-short-term bond ETFs.

Life insurance can be used as an investment vehicle, although its primary purpose is not investment. Permanent life insurance policies, such as whole life insurance, include a "cash value" component that grows over time. Policyholders can access this cash value while alive, but it is important to note that withdrawing money from the cash value reduces the death benefit.