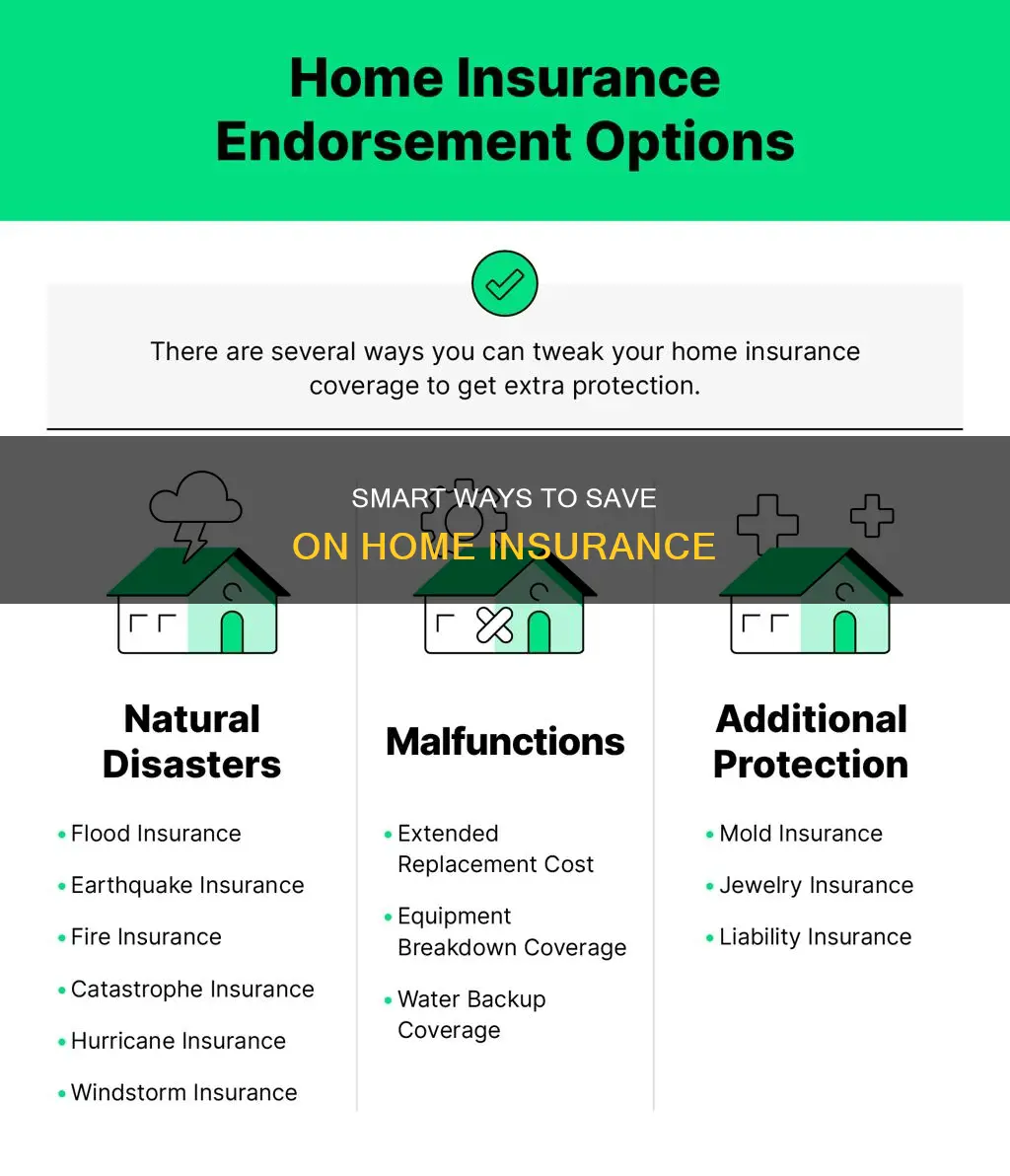

Home insurance is a necessity, but it can be costly. Luckily, there are many ways to save money on your policy. Firstly, it's important to shop around and compare prices and coverage options from different insurers. You should also consider the cost of insurance when buying a house, as factors like location and construction type can affect your premium. Increasing your deductible can save you money each month, but ensure you have enough savings to cover a larger out-of-pocket expense if needed. Installing security measures like burglar alarms, smoke detectors, and deadbolt locks can also earn you discounts. Maintaining and protecting your property can reduce the chances of making a claim, and some insurers offer lower rates for those with no recent claims. You can also save by choosing a joint buildings and contents cover instead of separate policies. Finally, consider the coverage you need and any unnecessary features you can cut back on, such as accidental damage cover if you don't have children or expensive items.

| Characteristics | Values |

|---|---|

| Timing | Buying at the right time can save up to 25%. Getting a quote 15 days before the renewal date is cheapest on average. |

| Compare quotes | Shop around to find the best value deal. |

| Haggling | Haggling with your existing insurer can save you money. |

| Payment frequency | Paying annually can save you money as monthly payments are classed as a loan, and interest is charged. |

| Auto-renewal | Avoid auto-renewal and check if you can get a cheaper policy elsewhere. |

| Payment amount | Increasing your excess can reduce your premium, but only if you can afford to pay more in the event of a claim. |

| Security | Installing security devices such as alarms and high-quality locks can reduce your premium. |

| Insurer claims | Insurers may offer discounts to customers who haven't claimed against their insurance for a certain period. |

| Accurate valuation | Accurately calculate the rebuild cost and contents value of your home to avoid paying extra. |

| Optional extras | Only pay for the cover you need. Remove unnecessary extras such as accidental damage cover if you don't have children or expensive items. |

Explore related products

What You'll Learn

![]()

Compare quotes online

Comparing quotes online is a great way to save money on house insurance. Online platforms like Insurify, Policygenius, and Zebra allow you to compare quotes from hundreds of providers simultaneously. These platforms offer a quick and reliable way to find the best value for your money. Here are some tips to help you get the most out of comparing quotes online:

Provide Accurate Information:

When using an online comparison tool, ensure that you enter accurate and up-to-date information about your home, including its size, age, safety features, location, current value, claims history, and the level of coverage needed. This will help you get the most accurate quotes and ensure that you have sufficient coverage.

Consider Coverage and Deductibles:

Don't just look for the cheapest option; consider the amount of coverage you need. Review the details of each quote, including deductibles, coverage limits, and endorsements. Make sure you are comfortable with the deductibles and that the coverage offered meets your needs. Ask about extended replacement coverage if you're unsure about the exact amount of coverage required.

Compare Multiple Quotes:

Don't settle for the first few quotes you receive. Take the time to compare quotes from multiple companies. Review at least three different quotes to make an informed decision. This will help you find the most competitive rates and benefits.

Look for Discounts:

Insurance providers often offer various discounts, such as money off for bundling home and auto insurance or installing home security systems. Check the websites of different companies or contact their agents to inquire about available discounts. You may qualify for additional savings that are not included in the online quote.

Read the Fine Print:

When comparing quotes, be sure to read the fine print to understand the exclusions and inclusions of each policy. This will help you avoid any surprises later and ensure that you are getting the coverage you need.

By following these tips and using online comparison tools, you can save both time and money when shopping for house insurance.

Navigating the Path to Becoming a Farm Bureau Insurance Adjuster

You may want to see also

Explore related products

![]()

Pay annually

Paying for your house insurance annually is one way to save money on your insurance premium. While many people choose to pay monthly to make the cost more manageable, paying monthly often comes with a charge. By paying annually, you can avoid this charge, and save money overall.

If you can afford to pay the full year's premium upfront, this is a great way to save money. However, it is important to remember that you will be responsible for a larger sum of money if you need to make a claim. Therefore, it is recommended that you set aside enough money to cover a bigger deductible should disaster strike.

You can use the savings from your reduced premium to fund your deductible. For example, if you have a $1,000 deductible, you could save an average of nearly 12% a year by increasing it to $2,500. This puts money in your wallet every month that otherwise would have gone to your insurer.

It is also worth noting that the way an insurance provider processes claims can make a difference. For example, some providers will replace broken appliances with new, more energy-efficient models, while others may not. Therefore, it is important to shop around to find the best deal and ensure you have enough cover for your needs.

Explore related products

![]()

Don't auto-renew

Home insurance policies are usually purchased for year-long terms, and they often have an auto-renewal clause. This means that your home insurance will renew for another 12 months without you having to do anything, unless you specifically request that it does not continue. While this is an easy way of ensuring your cover does not expire, it can also mean that you end up paying more. Insurers tend to save their best deals for new customers, so your premiums will likely increase with auto-renewal.

Insurers are usually required to send out notifications around 45 to 60 days before the end of your policy period, and they must contact you at least 21 days before your policy is due to end. This notification will include details of your new policy and the premiums that you will be charged. However, if you auto-renew, you may miss out on a better deal with a different provider. Therefore, it is recommended that you compare quotes from different insurance carriers at least once a year to ensure you are getting the best value for money.

When you switch providers, you can usually take your no-claims discount with you. If you have not made a claim, you should have a no-claims bonus, which can give you leverage when trying to negotiate a better deal. However, it is worth noting that no-claims bonuses can still be given by other insurers, so make sure you are still getting the best deal. You can also use a contents calculator to ensure you are not paying for more cover than you need.

If you do not wish to auto-renew, make sure to get in touch with your provider a good amount of time before your contract finishes. You should have a 14-day cooling-off period during which you can cancel your policy for a minimal or no fee. However, if you cancel after this period, you may have to pay a hefty cancellation fee.

Is Your Money Safe on Venmo?

You may want to see also

Explore related products

![]()

Get security devices installed

Installing security devices can help to lower your home insurance costs. Security systems reduce the risk of burglary and can prevent future theft claims, which saves your insurance company money. This means they can pass on the savings to you through a discount on your insurance.

There are a variety of security devices that can help you save on insurance. Security cameras, for example, deter potential burglars and provide valuable evidence in the case of a break-in. Smoke and carbon monoxide detectors quickly detect fires and gas leaks, helping to prevent extensive damage and loss of life. Insurers may offer discounts for installing these detectors, as they reduce the risk of catastrophic claims.

Reinforced doors and windows can also help to lower insurance costs. Strengthening entry points with reinforced doors and shatterproof windows prevents easy access to your home, and insurance companies may offer lower rates to homeowners who take these extra precautions.

Smart home technology, such as automated lights and smart locks, can also help to enhance your home's security by allowing remote monitoring and control. Smart home devices can be expensive, but they may be worth the investment if they help you save on insurance costs and give you peace of mind.

When choosing a security system, you can opt for DIY installation or professional installation. Professional installation can ensure that your system is set up correctly and may be required for certain insurance discounts. You can also choose between self-monitored and professionally monitored systems, with the latter potentially offering greater savings.

Overall, installing security devices can provide both financial and safety benefits, making your home a safer and more secure place.

Understanding Insurance Carriers' Profit From Fixed Annuities

You may want to see also

Explore related products

![]()

Accurately calculate rebuild cost

When it comes to saving money on house insurance, one of the most important factors is accurately calculating the rebuild cost. This is because the rebuild cost is one of the most significant figures in your home insurance policy. Here are some detailed and instructive points on how to do this:

Firstly, it is important to understand what the replacement cost of a home entails. This refers to the cost of rebuilding your home from scratch, using similar construction materials to the original build. It includes the costs of labour, building materials, and other relevant expenses, but does not factor in the value of the land.

To calculate the rebuild cost, you will need to know the square footage of your home, as well as its age, foundation type, and other relevant details. You can then multiply the square footage by the local average cost per square foot to get a quick estimate. However, this method may not always be accurate, especially if your home deviates from the average in terms of materials, architectural style, or other features.

To get a more precise figure, you can use online replacement cost calculators, such as the BCIS Rebuild calculator, which is suitable for homes built with brick or stone walls and tile or slate roofs. These calculators factor in details like size, age, and materials to provide a reasonably accurate estimate. However, they may not account for market demands during high-volume periods, such as after a natural disaster when prices tend to surge.

If your home is made of unconventional materials, was built before 1850, or is a listed building, you may need to hire a professional surveyor or quantity surveyor to calculate the rebuild cost. While this option is more expensive, it ensures a more precise and comprehensive evaluation, giving you peace of mind that you are fully covered.

Additionally, unique architectural features, custom elements, or historical features may require specialised skills and materials, increasing the rebuilding costs. Other factors that can influence the rebuild cost include home systems (plumbing, electrical, and HVAC), location (building codes, accessibility, and environmental risks), and inflation and supply chain issues affecting material and labour prices.

By accurately calculating the rebuild cost of your home, you can ensure that you are neither overpaying for your insurance nor underinsured, which could result in insufficient coverage in the event of a claim.

The Comprehensive Guide to Becoming a Successful Remote Insurance Adjuster

You may want to see also

Frequently asked questions

Shop around for the best price and accurately answer any questions about your circumstances when taking out a policy. It's also worth checking what is and isn't covered before purchasing.

You can save money by bundling your insurance policies together and buying from the same provider. For example, buying home and auto insurance together.

Increasing your deductible will put money in your wallet every month, but you need to ensure you have enough saved to cover a bigger out-of-pocket expense if you need to make a claim.