Lenders Mortgage Insurance (LMI) is a type of insurance that protects the lender in case the borrower is unable to repay their home loan. It is usually required when the borrower has a deposit of less than 20% of the property's value. The cost of LMI is typically passed on to the borrower and can be paid upfront or added to the loan amount. The calculation of LMI premiums takes into account various factors, including the loan amount, loan-to-value ratio (LVR), and the lender's specific policies. Online LMI calculators are available to help estimate the potential cost of LMI for a specific property purchase.

| Characteristics | Values |

|---|---|

| What is LMI? | Lenders Mortgage Insurance (LMI) is a one-off, non-refundable, non-transferrable premium that's added to your home loan. |

| Who does LMI protect? | LMI protects the lender if you default on your home loan. |

| Who pays for LMI? | The borrower pays for LMI. |

| When is LMI applicable? | LMI is usually required if your Loan-to-Value Ratio (LVR) is above 80%, meaning you have a deposit of less than 20% of the property's value. |

| How much does LMI cost? | LMI can cost around 1-5% of your home loan amount, depending on your LVR. |

| How is LMI calculated? | LMI is calculated as a percentage of your loan amount. The cost is typically based on the size of your deposit and how much you borrow. |

| How can I pay for LMI? | LMI is payable either as an upfront lump-sum payment or by capitalising it into the loan and paying it off over the life of your mortgage. |

| How can I avoid paying LMI? | You can avoid paying LMI by having a deposit of 20% or more. Alternatively, the government will guarantee part of your loan, removing the need for LMI. |

Explore related products

What You'll Learn

![]()

Lenders Mortgage Insurance (LMI)

The cost of LMI varies depending on several factors, including the LVR, the size of the loan, and the lender's policies. It is generally calculated as a percentage of the loan amount, ranging from 1% to 5%. For example, a $500,000 loan with a 10% deposit may incur an LMI cost of over $10,000. LMI calculators are available online to estimate these costs based on an individual's circumstances.

LMI can be paid in two ways: as an upfront lump-sum payment or by capitalising it into the loan. Paying upfront requires a significant amount of money readily available, whereas capitalising the LMI fee adds it to the loan's principal balance, increasing the overall loan amount and interest paid over time.

While LMI is not mandatory in all cases, it enables borrowers with smaller deposits to enter the market sooner. Without LMI, lenders may refuse to lend to those with low deposits. Additionally, some lenders may waive LMI costs for certain professions, such as medical and legal professionals, or for borrowers with stable employment histories.

It is important to note that LMI protects the lender and not the borrower, despite the borrower incurring the cost. Borrowers seeking financial protection against illness, disability, unemployment, or death can consider Mortgage Protection Insurance (MPI).

Metropcs Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Loan-to-Value Ratio (LVR)

The Loan-to-Value Ratio (LVR) is a term used a lot in the world of home loans. It is the amount you need to borrow, calculated as a percentage of the property's 'lender-assessed value'. LVR is calculated by dividing the loan amount by the lender-assessed value of the property and then multiplying by 100 to get a percentage. For example, if you borrow $450,000 to buy a property valued at $600,000, the LVR is 75% (450,000/600,000 x 100 = 75%).

LVR is important because it affects your borrowing power. Lenders place a large emphasis on LVR when assessing loan applications. Generally, loans with an LVR over 80% are considered higher risk. If your LVR is higher than 80%, you may be required to pay for Lenders Mortgage Insurance (LMI). LMI protects the lender if you default on your home loan and there is a shortfall following the sale of the property.

LMI is a one-off, non-refundable, non-transferrable premium that is added to your home loan. It is calculated based on the size of your deposit and how much you borrow. The more you contribute to the purchase price of the property, the lower the cost of LMI will be. LMI can be paid as an upfront lump sum or capitalised into the loan.

Lenders will usually require you to have a deposit of 20% of the property's value to avoid LMI. For example, if you want to buy a house worth $500,000, you will typically need to have a deposit of $100,000. If your LVR is below 80%, you can get an LMI exemption.

Prescription Insurance: Is It a Worthy Investment?

You may want to see also

Explore related products

![]()

Deposit size

The deposit size is a critical factor in determining whether you need to pay mortgage insurance in Australia. Lenders Mortgage Insurance (LMI) is typically required when the borrower's deposit is less than 20% of the property's purchase price. The premium for LMI can vary depending on the

Parking Tickets: Do They Affect Insurance Rates?

You may want to see also

Explore related products

![]()

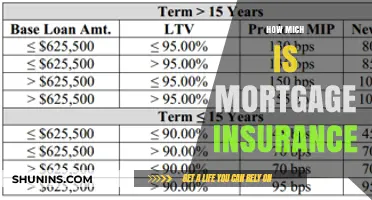

LMI cost

Lenders Mortgage Insurance (LMI) is a one-time, non-refundable, and non-transferable premium that is added to your home loan. It is calculated based on the size of your deposit and how much you borrow. The cost of LMI varies depending on several factors, including the loan amount, the loan-to-value ratio (LVR), and the lender's specific policies. Generally, LMI can range from 1% to 5% of the loan amount. For example, on a $500,000 loan with a 10% deposit (LVR of 90%), the LMI cost could be over $10,000. If you have a 20% or larger deposit, you typically won't need to pay LMI.

LMI is payable either as an upfront lump-sum payment or by capitalising it into the loan. Capitalising the LMI fee means adding it to the home loan's principal balance, which increases the total loan amount and the interest paid over the life of the loan. LMI calculators are available online to estimate the potential LMI expense based on the property value and deposit amount.

The cost of LMI can be influenced by factors such as the state in which the property is located, the borrower's employment status, and the loan type (investment or owner-occupied). Additionally, the borrower's occupation and financial stability may be considered, with some lenders waiving LMI for certain professions or applicants deemed low-risk.

While LMI protects the lender in case of borrower default, it enables borrowers to enter the market sooner by purchasing a home with a smaller deposit. However, it is important to note that LMI does not protect the borrower, and there are strategies to avoid paying LMI, such as saving for a larger deposit or exploring alternative loan options.

Ski Pass Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

LMI waivers

Lenders Mortgage Insurance (LMI) is a one-off, non-refundable premium that is added to a home loan. It is calculated based on the size of the deposit and the loan amount. LMI is usually required if the loan-to-value ratio (LVR) is above 80%, meaning the deposit is less than 20% of the property's value. While LMI protects the lender, the cost is typically passed on to the borrower.

The First Home Guarantee in Australia allows first-time homebuyers to purchase a home with just a 5% deposit without paying LMI. This program helps individuals enter the housing market sooner and makes homeownership more accessible.

Some banks and lenders offer LMI waivers based on various criteria. For example, NAB provides LMI waivers for doctors, lawyers, and financial professionals. These waivers can make a significant difference in the overall cost of a home loan.

It is important to note that LMI waivers are not widely advertised by lenders, and seeking expert advice or utilizing resources like LMI Waiver can help identify eligibility for waivers. By understanding the eligibility criteria and lender policies, homebuyers can make informed decisions and explore options to secure a mortgage without incurring the additional cost of LMI.

Should You Insure Your Train Ticket?

You may want to see also

Frequently asked questions

LMI stands for Lenders Mortgage Insurance. It is a type of insurance that protects the lender in case the borrower is unable to repay their home loan.

LMI is calculated as a percentage of your loan amount. The bigger the loan, the higher the cost of the insurance. The smaller the deposit, the higher the cost of LMI. LMI can be paid as an upfront lump-sum payment or by capitalising it into the loan.

The cost of LMI varies depending on several factors, including the size of the loan, the size of the deposit, and the lender's specific policies. LMI can range from 1% to 5% of the loan amount. For example, on a $500,000 loan with a 10% deposit, LMI could cost over $10,000.