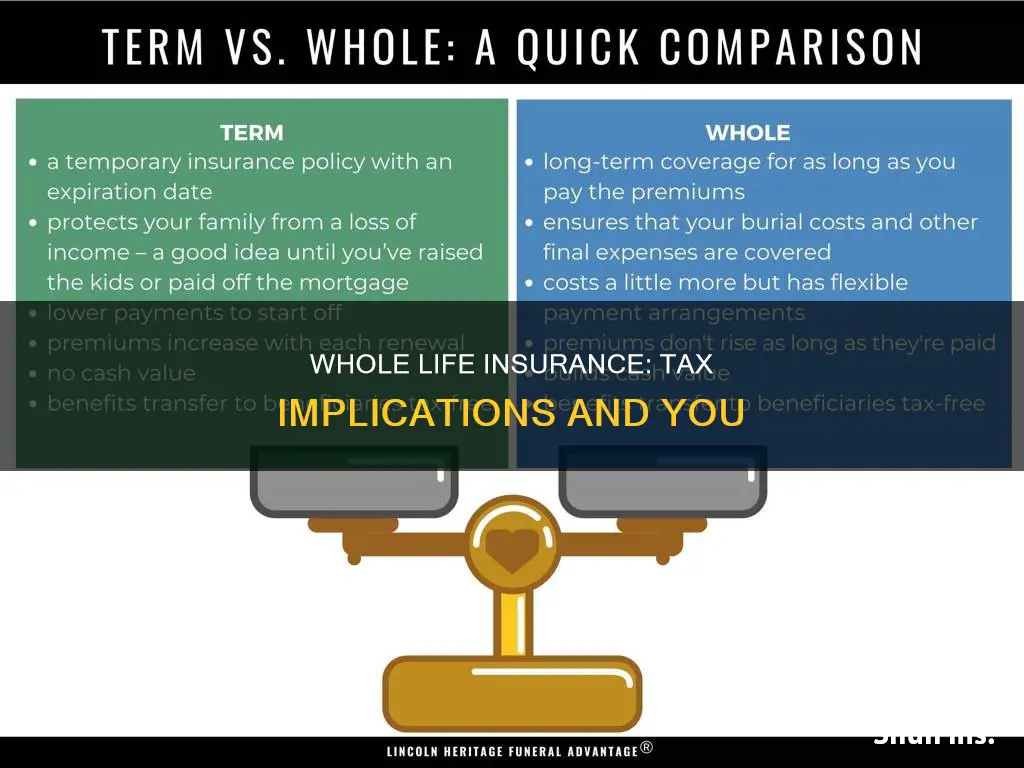

Whole life insurance is a form of permanent life insurance that provides coverage for the entirety of the policyholder's life, as long as premiums are paid. It also has a cash value component that can be used during the policyholder's lifetime. This cash value is not taxed while it is growing, but there are certain instances where taxes may be owed on the cash value, such as withdrawing more than the total premiums paid into the policy. Additionally, if the policy is surrendered or sold, and the proceeds exceed the cumulative premiums, the excess may be taxed as ordinary income. While life insurance death benefits are typically tax-free, there are exceptions, such as when the benefit is paid out in installments or left to the policyholder's estate.

| Characteristics | Values |

|---|---|

| Interest generated from whole life insurance policies taxed | No, until the policy is cashed out |

| Life insurance premiums taxed | No |

| Life insurance death benefit taxed | No, but there are exceptions |

| Whole life insurance policy loan taxed | No, but the loan amount will be deducted from the death benefit |

| Whole life insurance policy surrender taxed | Yes, if the cash surrender value is higher than the amount of premiums paid into the policy |

| Whole life insurance policy sale taxed | Yes, if the sale amount exceeds the amount of premiums paid into the policy |

| Whole life insurance dividends taxed | No, but interest earned on dividends is taxable |

| Whole life insurance policy with no named beneficiaries taxed | Yes, if the value of the estate exceeds the federal estate tax threshold |

| Whole life insurance benefit paid as an annuity taxed | Yes, the interest accrued in the annuity account is taxable |

Explore related products

What You'll Learn

![]()

Interest on whole life insurance policies

Interest generated from whole life insurance policies is not taxed until the policy is cashed out. This is known as "tax-deferred", and it means that the interest you make on your cash value is applied to a higher amount as it is not being reduced by taxes each year. This is a benefit of whole life insurance policies, as the cash value grows over time and can be used as an investment. The cash value of a whole life policy typically earns a fixed rate of interest.

The cash value of a whole life insurance policy will not be taxed while it is growing. Interest accrues on a tax-deferred basis, and the interest build-up portion of the annual increase in the policy's cash value is not taxed annually by the IRS. This is because life insurance is intended to support one's beneficiaries, so the IRS treats it differently from other types of financial products.

However, if you withdraw more than you have contributed to the cash value, the excess amount is taxed as income. Withdrawals are tax-free up to the value of the total premiums paid. If you surrender the whole policy, you will likely be subject to income tax on the value it has gained, and your beneficiaries will not receive a life insurance death benefit when you die.

Additionally, if you take out a loan against the cash value of your policy, it will accrue interest, which you will need to pay back along with the loan amount. If the loan is not repaid, it will reduce the death benefit. Interest charged on policy loans varies per insurer but is generally lower than you would get with a personal loan or home equity loan.

Ohio Life and Health Insurance Exam: Challenging or Easy?

You may want to see also

Explore related products

![]()

Whole life insurance as an investment

Whole life insurance is a type of permanent life insurance that provides coverage for your whole life as long as you continue to pay your premiums. It is typically purchased for its death benefit, but it can also be used as an investment tool and savings account. Here are some ways whole life insurance can be used as an investment:

- Withdraw or take a loan on the cash value: You can tap into the cash value of your whole life insurance policy to pay for major expenses, such as college fees, a down payment on a house, an emergency fund, or retirement income. Withdrawing or taking a loan against the cash value can provide you with tax-free income, as there is no tax liability on partial surrenders of non-modified endowment contracts until you have received all your premiums back. However, if you take out a loan, you will need to repay it with interest, and failing to do so may cause your contract to lapse.

- Create generational wealth: Whole life insurance can help you create generational wealth by allowing you to leave the full value of assets to your heirs. By creating an irrevocable life insurance trust (ILIT), the death benefit proceeds from your whole life insurance policy may pass to your heirs outside of your taxable estate, helping them cover any estate taxes and continue building wealth.

- Collect dividends: Some whole life insurance policies offer dividends, which are payments made by the insurance company to eligible clients when the company performs better financially than expected for the year. You can use these dividends to reduce your out-of-pocket payments, pay yourself directly, earn interest, pay back loans, or purchase paid-up additional insurance to increase the cash value and death benefit of your policy.

- Surrender the policy: If you no longer need your whole life insurance policy, you can surrender it and receive the accumulated cash value, minus any fees and outstanding loan balances. However, surrendering the policy may create a taxable event, and you will need to consider the consequences of giving up the death benefit.

While whole life insurance can be a valuable investment tool, it is important to note that it has higher premiums than term life insurance and provides less flexibility in modifying coverage and choosing how to invest the cash value. Additionally, the cash value of whole life insurance policies can be slow to grow, and you may earn higher returns with other investments. Therefore, it is essential to carefully consider your financial goals and consult with a financial professional before deciding if whole life insurance is the right investment for you.

Nurses Aid Life Insurance Applications at Home

You may want to see also

Explore related products

![]()

Whole life insurance and estate taxes

Life insurance proceeds are tax-free to some extent, but there are situations in which they can be subject to estate tax. This is a complex area, so it's important to consult a tax advisor for specific guidance. Here are some key considerations regarding whole life insurance and estate taxes:

Naming the Estate as Beneficiary

If the estate is named as the beneficiary of a life insurance policy, the death benefit is typically included in the estate and subject to estate tax. This can significantly increase the estate's value and result in high estate taxes for heirs. To avoid this, most people name individuals as beneficiaries, ensuring that the death benefit remains separate from the estate.

Ownership of the Policy

The owner of a life insurance policy has lifetime rights to the contract, including the ability to borrow against it, cancel it, or designate beneficiaries. The owner of a policy is not always the insured individual. For example, you might purchase a policy on your spouse's life, making you the owner. If the owner/insured spouse dies, the death benefit is included in the deceased's estate but qualifies for the "unlimited marital deduction," which means there is no estate tax until the surviving spouse also passes away.

Transfer of Ownership

Transferring ownership of a life insurance policy is a common strategy to reduce potential estate taxes. To do this, the policy owner must surrender all rights to the policy, including the ability to make changes, to a competent adult or entity. The new owner must pay the premiums, but the previous owner can gift an amount up to the annual gift tax exclusion ($16,000 in 2022 and $17,000 in 2023) to help cover these costs. It's important to note that the original owner must survive for at least three years after the transfer for this strategy to be effective in removing the death benefit from the estate for tax purposes.

Irrevocable Life Insurance Trust (ILIT)

Another way to remove life insurance proceeds from the taxable estate is to create an ILIT. In this case, the policy is held in trust, and the owner no longer has any rights to the policy or its proceeds. This ensures that the proceeds are not included in the estate. ILITs can be particularly useful when beneficiaries are minor children, as a trusted family member can be named as trustee to manage the funds according to the trust document.

State and Federal Taxes

While federal estate taxes typically apply to larger estates, with an exemption amount of $12.92 million for 2023, it's important to consider state inheritance taxes as well. Twelve states and the District of Columbia impose an estate tax, and their exemption thresholds can be much lower. For example, in Massachusetts and Oregon, the exemption was only $1 million in 2021.

Login Credentials for SBI Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Whole life insurance and income tax

Whole life insurance is a form of permanent life insurance that provides coverage for your entire life, as long as you keep your payments up to date. It also has a cash value component that is money you can use during your lifetime. This cash value will increase each year on a schedule guaranteed by the insurance company, allowing it to grow throughout your life.

The cash value of a whole life insurance policy is not taxed while it's growing. This is known as "tax-deferred", and it means that your money grows faster because it's not being reduced by taxes each year. The interest you make on your cash value is applied to a higher amount, resulting in greater overall growth. This can be particularly beneficial if you withdraw your money when you're in a lower tax bracket later in life, as it will be taxed less than when it was first applied to your account.

You can access the cash value that has accumulated in your policy through loans or withdrawals without immediate tax consequences, as long as they are structured properly. However, if you withdraw more than your cumulative premium payments, you may have to pay income taxes on the excess. Additionally, if you have unpaid loans against the policy, they will be deducted from the death benefit, resulting in a lower payout to your beneficiaries.

Dividends received from the insurance company are also generally not taxable. However, if you choose to leave your dividends with the insurer in exchange for interest, then you may pay income tax on the interest earned.

When it comes to the death benefit, it is typically not taxed as income, and your beneficiaries receive the full amount. However, if you choose to receive the death benefit in installments instead of a lump sum, any interest that builds up on those payments could be taxed as regular income. Additionally, if you leave the death benefit to your estate instead of directly naming a person as the beneficiary, it may be subject to estate taxes if the value of your estate exceeds the federal estate tax exemption.

Life Insurance Options Post-Melanoma: What You Need to Know

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![]()

Whole life insurance and tax deductions

Whole life insurance is a form of permanent life insurance that provides coverage for the entirety of the policyholder's life, as long as premiums are paid. It also has a cash value component that can be used during the lifetime of the insured. This cash value is not taxed while it is growing, which is known as "tax-deferred". The interest made on the cash value is also not taxed annually by the IRS.

The death benefit paid to beneficiaries is generally not taxed as income, though there are some exceptions. If the beneficiary chooses to receive the death benefit as an annuity, the interest accrued by the annuity account may be subject to taxes. If the policy is left to the estate instead of a named individual, estate taxes may apply.

Policyholders can borrow or withdraw money from the cash value of a whole life insurance policy. Withdrawing up to the amount of the total premiums paid into the policy is usually tax-free. However, withdrawing any gains, such as dividends, may be taxed as ordinary income. If there are any outstanding loans against the policy when it is terminated or surrendered, the loan amount exceeding the total premiums may be subject to income taxes.

Selling or surrendering a whole life insurance policy may also have tax implications. If the sale or surrender proceeds exceed the cumulative premiums, the excess may be subject to income taxes.

Term Life Insurance: A Smart Financial Move?

You may want to see also

Frequently asked questions

The cash value of whole life insurance grows tax-free. However, there are some instances where you may owe taxes on the cash value.

If you take out a loan from your life insurance plan and the policy terminates before you’ve repaid the loan, you will be taxed on the remaining loan amount. You can also withdraw up to the amount of the total premiums you’ve paid into the policy without paying taxes, but any withdrawals on gains, such as dividends, will be taxed as ordinary income.

In general, a life insurance benefit isn’t subject to taxes. However, there are a few exceptions. If you opt for monthly installments rather than a lump sum, the funds that have yet to be distributed will accrue taxable interest. Also, if you plan to name your estate as a beneficiary, you may owe taxes as well.

Consult a tax advisor to determine how your unique situation may impact the tax status of your whole life insurance.

Inheritance or estate taxes may apply if the policy is part of the deceased's estate, and the value of the estate exceeds the state or federal estate tax threshold.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)