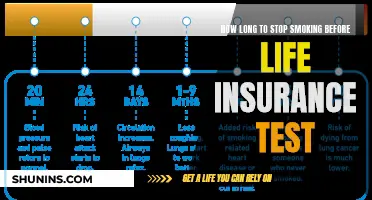

The vetting period for life insurance, also known as the waiting period, is the time between applying for a policy and the moment your coverage begins. This typically lasts between four to six weeks, but it can be longer depending on the type of insurance and the company. During this time, insurers assess your background and health profile to determine your insurance risk and policy cost. While some policies offer immediate coverage, others require thorough underwriting, which can cause delays. It's important to clarify the waiting period with your chosen provider before purchasing a policy.

| Characteristics | Values |

|---|---|

| Waiting period | Time between applying for a policy and the moment your coverage becomes active |

| Waiting period length | 4-6 weeks on average, but can be longer |

| Waiting period for specific insurances | Health insurance: 30-90 days; Dental insurance: preventive care (covered right away), basic care (6 months), major care (1 year) |

| Accelerated underwriting | Coverage with a shorter waiting period or no waiting period |

| Instant issue life insurance | Coverage with no waiting period |

Explore related products

What You'll Learn

- The vetting period for life insurance is called the waiting period

- The waiting period can last anywhere from one month to several months

- The waiting period allows insurance companies to review health and other factors

- The type of policy determines the length of the waiting period

- You can get temporary coverage while you wait for your official policy to become active

![]()

The vetting period for life insurance is called the waiting period

The waiting period allows insurance companies to review an applicant's health and other factors before approving a life insurance policy and preventing fraud. Insurers evaluate policies carefully to better understand the risk of death and prevent insurance fraud. During the waiting period, the insurance company will review your health history, motor vehicle record, and other factors that inform pricing and approval. This evaluation process is called underwriting.

The length of the waiting period depends on the type of insurance and the insurance company. It usually lasts about four to six weeks, which is the time it takes to process a life insurance application. However, it can be longer, ranging from one to several months. Some policies offer immediate coverage, while others require thorough underwriting and may result in delays.

Maximizing Whole Life Insurance: Finding the Elusive Q X

You may want to see also

Explore related products

![]()

The waiting period can last anywhere from one month to several months

The waiting period for life insurance can last anywhere from one month to several months. This is the time between when you apply for a policy and when your coverage begins. During this time, insurers evaluate your background and health profile to assess your insurance risk and determine your premium.

The length of the waiting period depends on the type of insurance and the insurance company. Some policies offer immediate coverage after the first premium payment, while others require thorough underwriting and may have delays. Full underwriting can take time, and if any disqualifying factors are found, coverage may not take effect during the waiting period.

To avoid a long waiting period, you can consider a simplified issue policy, which has a shorter health questionnaire, or a policy with accelerated underwriting, which will provide an application decision almost immediately. You can also add temporary life insurance to your policy to cover you during the waiting period.

Life Insurance for the Young: A Smart Move?

You may want to see also

Explore related products

![]()

The waiting period allows insurance companies to review health and other factors

The waiting period in life insurance is the time between applying for a policy and the start of your coverage. This period allows insurance companies to review your health and other factors to assess your insurance risk and determine your premium. It also helps prevent fraud.

During the waiting period, insurers evaluate your background and health profile, including your health history and motor vehicle record. This process is called underwriting, and it can be thorough or simplified. Full underwriting can take a considerable amount of time, and if any disqualifying factors are found, your coverage will not take effect during the waiting period. Simplified issue policies, on the other hand, involve a shorter health questionnaire but may result in higher premiums and limited death benefits.

The length of the waiting period depends on the type of insurance and the insurance company. It typically ranges from one to several months. For example, health insurance often has an initial waiting period of 30 to 90 days, while dental insurance may have different waiting periods for preventive, basic, and major care.

During the waiting period, you do not have life insurance coverage, and your beneficiaries will not receive any insurance money if you pass away. To bridge this gap, you can add temporary life insurance to your policy. Alternatively, you can explore accelerated underwriting or instant issue life insurance policies, which offer shorter or no waiting periods.

Is Illinois' Insurance Exam Challenging?

You may want to see also

Explore related products

![]()

The type of policy determines the length of the waiting period

The type of life insurance policy you choose will determine the length of the waiting period before your coverage becomes active. The waiting period is the time between when you apply for a policy and when your coverage begins. This period allows insurance companies to review your health and other factors to evaluate your background and health profile, thus determining your insurance risk.

Some policies offer immediate coverage after the first premium payment, while others require thorough underwriting and may have delays. Full underwriting can take time, and if any disqualifying factors are found, coverage may not take effect during the waiting period. Simplified issue policies have a shorter health questionnaire but may result in higher premiums and limited death benefits.

Workplace coverage eligibility also varies, with some offering immediate coverage and others having waiting periods of up to 90 days. Life insurance policies often require thorough underwriting, where the insurance company will review your health history, motor vehicle record, and other factors that inform pricing and approval.

If you're healthy, waiting for approval may be worthwhile for potentially more affordable premiums. After submitting an application and paying your first premium, you might qualify for temporary conditional coverage immediately, but this depends on specific requirements. If you don't meet the criteria, the insurer will need to conduct a review.

With accelerated underwriting, you may get an application decision almost immediately, but there may be limitations on the maximum death benefit.

Does AARP's Guaranteed Life Insurance Offer Cash Value?

You may want to see also

Explore related products

![]()

You can get temporary coverage while you wait for your official policy to become active

The life insurance vetting period or waiting period is the time between applying for a policy and the moment your coverage begins or becomes active. This period typically lasts four to six weeks but can be longer, depending on the type of policy and coverage amount. During this time, insurance companies review your health history, motor vehicle record, and other factors to determine your insurance risk and premium.

Since you don't have coverage during the waiting period, you can get temporary life insurance to protect your beneficiaries while you wait for your official policy to become active. Here's how it works:

Temporary life insurance, also known as a temporary insurance agreement (TIA), is short-term coverage you can buy during the life insurance application process. It protects your beneficiaries if you pass away before your final application is approved and your official policy becomes active. The death benefit is usually equal to the coverage amount you applied for, up to a limit (often $1 million).

You can add temporary coverage when you initially apply for life insurance, and it can begin as soon as you sign your application and receive a temporary insurance receipt.

Temporary life insurance generally lasts up to 90 days, giving the insurer enough time to review your policy application. However, it may end earlier if:

- Your official policy becomes active.

- Your application is declined or denied.

- You receive an offer but decide not to proceed with coverage.

- You don't respond to insurer requests for information in a timely manner.

- You pass away, and the insurer pays out the temporary life insurance death benefit.

The cost of temporary coverage is typically based on your quoted premiums for the official policy. For example, if your quoted premium is $30 per month, your temporary coverage will also cost $30. Some insurers don't require upfront payment for temporary coverage and will only need your banking information.

Once your official policy premium is determined during underwriting, the payment you made for temporary coverage will be credited toward your first month's premium.

Getting temporary life insurance while waiting for your official policy ensures your beneficiaries receive a death benefit payout, even if you pass away before your actual policy activates. It provides peace of mind during the underwriting process and prevents any loss before your official coverage is approved.

However, keep in mind that temporary life insurance may not be necessary if you're looking for immediate coverage. In that case, consider no-exam life insurance or instant decision life insurance, which offer faster coverage by skipping the medical exam.

Understanding Life Insurance Dividends Calculation Process

You may want to see also

Frequently asked questions

The vetting period for life insurance, also known as the waiting period, typically lasts between four to six weeks but can be longer. This is the time it takes for the insurance company to process your application, evaluate your background and health profile, and determine your insurance risk.

During the vetting period, the insurance company will review your health history, motor vehicle record, and other factors that inform pricing and approval. They may also look into your background and health profile to assess your insurance risk.

Yes, you can add temporary life insurance to your policy to cover you during the vetting period. Some insurers also offer accelerated underwriting or instant issue life insurance policies, which provide coverage with a shorter waiting period or no waiting period at all.