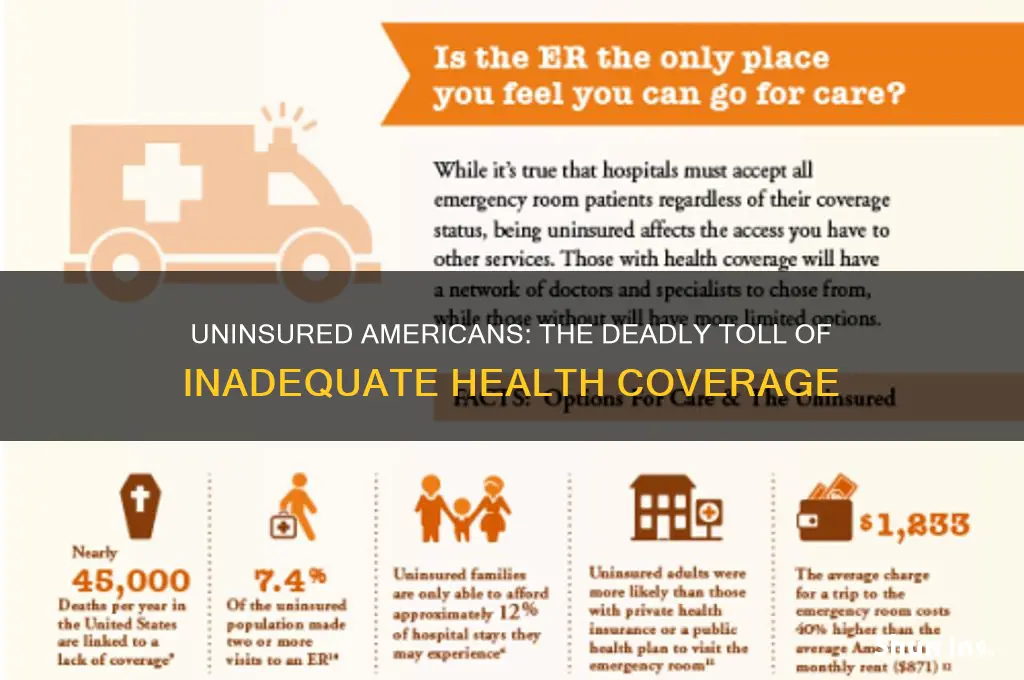

The lack of adequate health insurance in the United States has become a significant contributor to preventable deaths, with studies estimating that thousands of Americans die each year due to barriers in accessing necessary medical care. Research, including a widely cited study from *The American Journal of Public Health*, suggests that uninsured individuals face higher mortality rates compared to those with coverage, often due to delayed diagnoses, forgone treatments, and limited access to preventive services. Factors such as high healthcare costs, gaps in Medicaid expansion, and disparities in coverage disproportionately affect low-income and minority populations, exacerbating health inequities. While exact numbers vary, estimates indicate that tens of thousands of deaths annually could be averted with universal or more comprehensive health insurance, highlighting the urgent need for policy reforms to address this public health crisis.

| Characteristics | Values |

|---|---|

| Annual Uninsured Deaths (2019) | ~20,400 |

| Primary Cause | Lack of health insurance coverage |

| Age Group Most Affected | Working-age adults (18-64) |

| Leading Causes of Preventable Deaths | Heart disease, cancer, diabetes, and stroke |

| Study Source | Commonwealth Fund and Harvard Medical School |

| Year of Study | 2022 (using 2019 data) |

| Comparison to Other Causes | Higher than deaths from kidney disease or Alzheimer's |

| Potential Lives Saved with Coverage | Approximately 20-30% of uninsured deaths |

| Economic Impact | Estimated $176 billion in medical debt annually |

| Policy Implication | Expanding Medicaid and Affordable Care Act coverage could reduce mortality rates |

Explore related products

$0.99

What You'll Learn

- Lack of insurance access increases mortality rates among low-income Americans

- Delayed medical care due to high costs leads to preventable deaths

- Health disparities in uninsured populations worsen chronic disease outcomes

- Inadequate coverage limits access to life-saving treatments and medications

- Preventive care gaps in uninsured individuals contribute to higher fatality rates

![]()

Lack of insurance access increases mortality rates among low-income Americans

The absence of health insurance is a silent killer, disproportionately affecting low-income Americans. Studies consistently show that uninsured individuals are 40% more likely to die prematurely than their insured counterparts. This stark disparity isn’t merely a statistic—it translates to thousands of preventable deaths annually. For example, a 2017 study published in *The Lancet* estimated that nearly 45,000 excess deaths occur each year among working-age Americans due to lack of health insurance. These deaths are often tied to delayed or forgone medical care, untreated chronic conditions, and limited access to preventive services.

Consider the case of a 45-year-old uninsured individual with hypertension. Without regular check-ups or access to affordable medication, their condition could escalate to a stroke or heart attack. Insured patients, on the other hand, are more likely to manage their blood pressure effectively through consistent monitoring and medication adherence. This scenario isn’t hypothetical—it’s a recurring reality for millions. Low-income Americans, who often work in jobs without employer-sponsored insurance, face a Catch-22: they can’t afford insurance, yet they desperately need it to avoid life-threatening complications.

The financial barrier to insurance is compounded by systemic issues. Medicaid, designed to cover low-income individuals, isn’t universally available due to state-level variations in eligibility criteria. For instance, in states that haven’t expanded Medicaid under the Affordable Care Act, a single adult earning just above the poverty line ($13,590 annually) may still fall into the "coverage gap," earning too much for Medicaid but too little for subsidized marketplace plans. This gap disproportionately affects people of color, who are more likely to live in states with restrictive Medicaid policies, further exacerbating health disparities.

Practical solutions exist, but they require political will and systemic change. Expanding Medicaid in all states would immediately reduce mortality rates by providing coverage to an estimated 2.2 million uninsured adults. Additionally, capping out-of-pocket costs for essential medications and services could make care more accessible for those with limited coverage. Employers can also play a role by offering affordable insurance options or advocating for policy changes that benefit their low-wage workers. Until these steps are taken, the mortality gap will persist, a grim reminder of the human cost of inequitable access to healthcare.

Top Canadian Home Insurance Companies: A Comprehensive Comparison Guide

You may want to see also

Explore related products

![]()

Delayed medical care due to high costs leads to preventable deaths

Each year, an estimated 45,000 Americans die due to lack of health insurance, according to a Harvard study. While this statistic is alarming, it only scratches the surface of a broader issue: delayed medical care due to high costs, even among the insured. High deductibles, copays, and out-of-pocket expenses force many to postpone necessary treatments, turning manageable conditions into life-threatening crises. For instance, a 2021 Kaiser Family Foundation survey revealed that 43% of insured adults delayed or skipped care due to cost, a decision that can have fatal consequences.

Consider the case of a 55-year-old with persistent chest pain. Without insurance, a diagnostic cardiac workup—including an EKG, stress test, and potential angiogram—could cost upwards of $10,000. Even with insurance, a high-deductible plan might require the patient to pay $3,000 upfront. Faced with this financial burden, many delay seeking care, hoping symptoms will resolve on their own. However, untreated angina or early-stage heart disease can progress to myocardial infarction, a condition with a 30-day mortality rate of 7-10%. This scenario isn’t hypothetical; a 2019 study in *Health Affairs* found that delayed cardiovascular care was associated with a 50% higher risk of mortality within five years.

The problem extends beyond acute conditions to chronic illnesses, where consistent management is critical. A Type 2 diabetic requiring insulin faces monthly costs of $300-$500 without insurance assistance. Even with coverage, copays can exceed $100 per prescription. Skipping doses or rationing insulin to save money can lead to diabetic ketoacidosis, a life-threatening complication with a mortality rate of 5%. Similarly, a 2020 JAMA study found that 1 in 4 diabetics reported underusing insulin due to cost, a behavior directly linked to increased hospitalizations and mortality.

To mitigate these risks, patients must adopt proactive strategies. First, understand your insurance plan’s coverage, including deductibles, copays, and out-of-pocket maximums. For high-cost medications, inquire about manufacturer assistance programs or generic alternatives. For example, Eli Lilly’s Insulin Lispro costs $137 per vial, while its authorized generic version is priced at $25. Second, leverage preventive care services, which are often fully covered under the Affordable Care Act. Annual check-ups, cancer screenings, and vaccinations can detect issues early, reducing the need for costly interventions later. Finally, explore community health clinics or telehealth services, which offer affordable alternatives for non-emergency care.

While systemic reforms are necessary to address the root causes of high healthcare costs, individuals can take steps to minimize the risk of preventable deaths. Delaying care due to cost is a gamble with dire consequences, but informed decision-making and resource utilization can save lives. The choice between financial stability and health should never be a choice at all.

Midland Medical: Understanding Insurance Coverage and Options

You may want to see also

Explore related products

![Mortality of the Western Hemisphere. 1915 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![On the medical selection of lives for assurance [a lecture]](https://m.media-amazon.com/images/I/91JnALRBNgL._AC_UY218_.jpg)

![]()

Health disparities in uninsured populations worsen chronic disease outcomes

Lack of health insurance doesn't just delay care; it creates a cascade of consequences that disproportionately harm those already vulnerable. Chronic diseases, which require consistent management and preventive measures, become particularly deadly in uninsured populations.

Imagine diabetes, a condition manageable with medication, regular checkups, and lifestyle adjustments. For the uninsured, the reality is starkly different. Without access to affordable medication, blood sugar levels spiral out of control, leading to complications like kidney failure, blindness, and amputations. A study by the Commonwealth Fund found that uninsured adults with diabetes are twice as likely to experience these devastating complications compared to their insured counterparts.

This isn't an isolated example. Hypertension, asthma, and heart disease follow a similar pattern. Without preventive screenings, early detection becomes a luxury, allowing diseases to progress unchecked. Access to specialist care, crucial for managing complex chronic conditions, is often out of reach. The result? Uninsured individuals are more likely to experience severe disease progression, hospitalizations, and premature death.

The human cost is immeasurable, but the economic impact is staggering. Untreated chronic conditions lead to emergency room visits, costly interventions, and lost productivity, burdening both individuals and the healthcare system.

Addressing this disparity requires a multi-pronged approach. Expanding access to affordable insurance is paramount. Programs like Medicaid expansion have shown promising results in reducing disparities and improving health outcomes for low-income individuals. Additionally, community health centers play a vital role in providing primary care and preventive services to underserved populations.

Finally, we must address the social determinants of health that contribute to insurance disparities. Poverty, lack of education, and racial inequities create barriers to accessing healthcare. By tackling these root causes, we can create a system where chronic disease management is a right, not a privilege, and where preventable deaths become a relic of the past.

Top-Rated Homeowners Insurance Companies: Customer Reviews and Satisfaction

You may want to see also

Explore related products

![]()

Inadequate coverage limits access to life-saving treatments and medications

Uninsured and underinsured Americans often face a stark reality: life-saving treatments and medications are financially out of reach. A 2019 study published in the *American Journal of Public Health* estimated that approximately 45,000 deaths annually in the U.S. are attributable to lack of health insurance. For those with inadequate coverage, high deductibles, copays, and exclusions create barriers to essential care. Consider a scenario where a 55-year-old with Stage 3 colorectal cancer requires a $10,000-per-month immunotherapy drug. Without sufficient coverage, they may forgo treatment entirely, reducing their 5-year survival rate from 70% to less than 15%. This isn’t an edge case—it’s a systemic issue affecting millions.

The problem extends beyond catastrophic illnesses to chronic conditions like diabetes, where insulin prices can exceed $300 per vial. A 2021 Yale study found that 1 in 4 diabetics ration insulin due to cost, a practice linked to fatal complications like diabetic ketoacidosis. For a 30-year-old Type 1 diabetic, skipping doses to save money isn’t a choice—it’s a survival gamble. Similarly, preventive medications like statins for heart disease or antivirals for HIV are often unaffordable for the underinsured, turning manageable conditions into death sentences. The irony? These medications are cheaper to provide than the emergency care required when conditions worsen.

To address this, patients must navigate a labyrinth of assistance programs, each with stringent eligibility criteria. For instance, the HealthWell Foundation offers copay assistance for cancer treatments but caps annual grants at $15,000—a fraction of many drug costs. Pharmaceutical patient assistance programs (PAPs) exist but exclude those on Medicare, leaving seniors particularly vulnerable. Practical tips include verifying coverage for specific medications using tools like GoodRx, appealing denied claims with detailed medical necessity documentation, and exploring state-based prescription drug assistance programs (SPAPs). However, these solutions are Band-Aids on a hemorrhaging system.

Comparatively, countries with universal healthcare systems, such as Canada or the UK, report significantly lower mortality rates from treatable conditions. In Canada, where insulin costs $30 per vial, diabetic mortality is 40% lower than in the U.S. This disparity underscores the moral and economic failure of tying life-saving care to insurance coverage. Until systemic reforms are enacted, Americans will continue to die not from incurable diseases, but from the inability to afford cures that exist. The takeaway is clear: inadequate coverage isn’t just a financial burden—it’s a death sentence.

Does DoorDash Offer Health Insurance? Benefits for Dashers Explained

You may want to see also

Explore related products

![]()

Preventive care gaps in uninsured individuals contribute to higher fatality rates

Lack of health insurance creates a stark divide in access to preventive care, a disparity that directly translates to higher fatality rates among uninsured Americans. Studies consistently show that uninsured individuals are significantly less likely to receive routine screenings for conditions like cancer, diabetes, and heart disease. These screenings, often covered by insurance plans, are crucial for early detection when treatment is most effective. For example, a 2018 study published in the American Journal of Public Health found that uninsured women were 30-50% less likely to receive mammograms, leading to later-stage breast cancer diagnoses and poorer survival rates.

A similar pattern emerges for colorectal cancer screening. The American Cancer Society recommends colonoscopies starting at age 45, yet uninsured individuals are far less likely to undergo this potentially life-saving procedure. This delay in detection often results in advanced-stage diagnoses, where treatment options are limited and survival rates plummet.

The impact of preventive care gaps extends beyond cancer. Uninsured individuals are less likely to receive vaccinations, including those for influenza and pneumonia, leaving them vulnerable to preventable illnesses. They also face barriers to managing chronic conditions like diabetes and hypertension. Without regular check-ups and medication access, these conditions can spiral out of control, leading to complications like heart attacks, strokes, and kidney failure.

Imagine a 55-year-old uninsured man with undiagnosed high blood pressure. Without regular monitoring and medication, his risk of a fatal heart attack skyrockets. This scenario is not hypothetical; it's a tragic reality for countless uninsured Americans.

Addressing these preventive care gaps requires a multi-pronged approach. Expanding access to affordable health insurance is paramount. Policies like Medicaid expansion have demonstrably increased access to preventive services and improved health outcomes in participating states. Additionally, community health centers play a vital role in providing preventive care to uninsured populations, but they often face funding shortages. Increased investment in these centers is crucial. Finally, public health campaigns promoting the importance of preventive care and available resources can empower individuals to take control of their health, even without insurance.

Is the Health Insurance Penalty Gone for Good? Find Out Now

You may want to see also

Frequently asked questions

Studies estimate that approximately 30,000 to 45,000 Americans die annually due to lack of health insurance, as uninsured individuals often delay or forgo necessary medical care.

The main causes include delayed treatment for conditions like heart disease, cancer, diabetes, and preventable illnesses, as well as lack of access to preventive care and medications.

Lack of health insurance is a significant contributor to mortality, comparable to other risk factors like obesity and smoking, particularly among low-income populations.

Yes, low-income individuals, racial and ethnic minorities, and those in states without Medicaid expansion are disproportionately affected by deaths related to lack of health insurance.

Expanding coverage, such as through Medicaid expansion or universal healthcare, would improve access to preventive care, early diagnosis, and timely treatment, potentially saving thousands of lives annually.