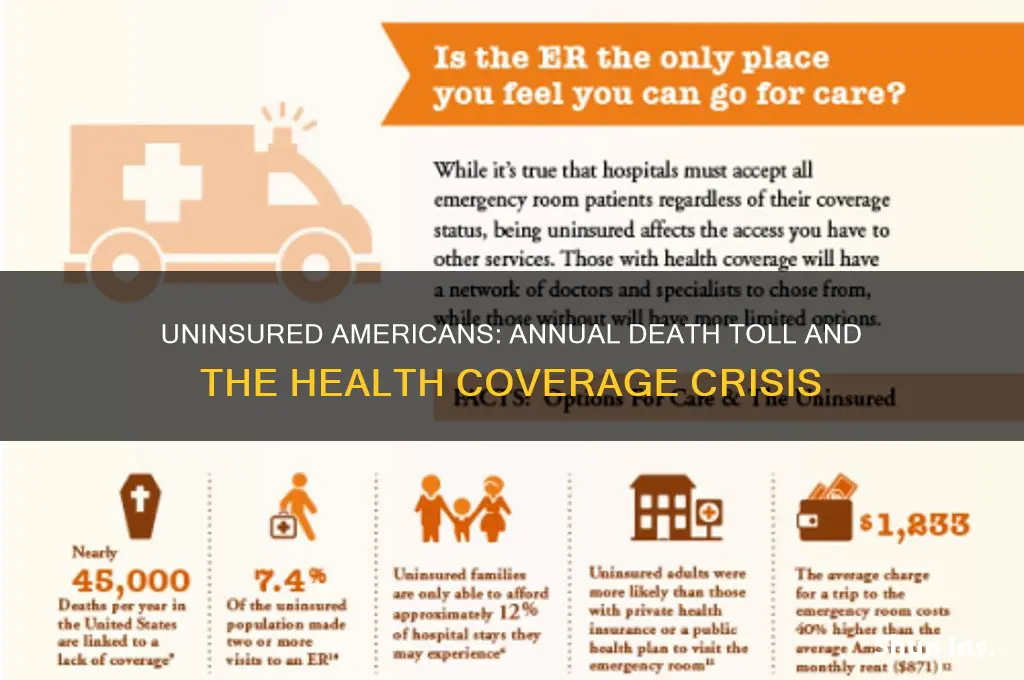

Every year, a significant number of Americans face dire health outcomes due to lack of health insurance, a stark reality that underscores the critical intersection of healthcare access and mortality. Studies suggest that tens of thousands of Americans die annually as a result of being uninsured, with estimates varying widely depending on the methodology and data sources used. These deaths are often attributed to delayed or forgone medical care, untreated chronic conditions, and inability to afford necessary treatments. The uninsured are more likely to experience preventable hospitalizations, complications from manageable illnesses, and reduced life expectancy compared to their insured counterparts. This issue highlights the profound impact of health insurance coverage—or lack thereof—on individual and public health, raising urgent questions about healthcare equity and policy reform in the United States.

| Characteristics | Values |

|---|---|

| Estimated Annual Deaths (Uninsured) | Approximately 10,000 to 45,000 (varies by study and methodology) |

| Primary Causes of Preventable Deaths | Delayed or forgone medical care, lack of preventive services |

| Age Groups Most Affected | Working-age adults (18-64 years old) |

| Racial/Ethnic Disparities | Higher rates among Hispanic and Black populations |

| Gender Disparities | Men are slightly more likely to be uninsured and affected |

| Geographic Disparities | Higher rates in Southern and rural states |

| Economic Impact | Increased healthcare costs and reduced productivity |

| Policy Impact | Deaths reduced in states with Medicaid expansion under ACA |

| Comparative Context | Uninsured deaths are preventable with access to healthcare |

| Latest Data Year | 2021-2023 (depending on the study) |

Explore related products

What You'll Learn

- Lack of Preventive Care: Uninsured skip check-ups, leading to undetected health issues and preventable deaths

- Delayed Treatment: Without insurance, people postpone care, worsening conditions and increasing mortality risk

- Financial Barriers: High medical costs deter uninsured individuals from seeking life-saving treatments

- Chronic Disease Management: Uninsured struggle to manage conditions like diabetes, raising death rates

- Emergency Care Reliance: Uninsured often use ERs for primary care, leading to poorer outcomes

![]()

Lack of Preventive Care: Uninsured skip check-ups, leading to undetected health issues and preventable deaths

Each year, an estimated 45,000 Americans die prematurely due to lack of health insurance, according to a Harvard study. A significant portion of these deaths stem from one critical factor: the absence of preventive care. Without insurance, millions skip routine check-ups, screenings, and vaccinations, allowing treatable conditions to escalate into life-threatening crises. This isn’t just a statistic—it’s a preventable tragedy rooted in systemic barriers to healthcare access.

Consider the case of a 45-year-old uninsured individual with no symptoms of hypertension. Without a routine check-up, their elevated blood pressure goes undetected. Over time, this untreated condition increases the risk of heart attack or stroke. A simple $20 blood pressure cuff and a 10-minute consultation could have identified the issue, but without insurance, the cost of a doctor’s visit—often $150 or more—becomes an insurmountable barrier. This scenario isn’t rare; it’s a recurring pattern that contributes to thousands of avoidable deaths annually.

The consequences of skipping preventive care extend beyond individual health. Uninsured patients often delay care until symptoms become severe, leading to emergency room visits that are far more costly—both financially and medically. For instance, untreated diabetes can progress to kidney failure, requiring dialysis at a cost of $80,000 per year, compared to $500 annually for preventive management. This financial burden not only affects the individual but also strains the healthcare system, as taxpayers subsidize uncompensated emergency care.

To address this issue, practical steps can be taken. Community health clinics offer low-cost or sliding-scale preventive services, including blood pressure screenings, cholesterol tests, and cancer screenings. Programs like the CDC’s Colorectal Cancer Control Program provide no-cost screenings for eligible uninsured individuals aged 45–64. Additionally, pharmacies like CVS and Walgreens offer free blood pressure checks and diabetes risk assessments. While these resources aren’t a substitute for comprehensive insurance, they serve as critical lifelines for those without coverage.

Ultimately, the lack of preventive care among the uninsured is a solvable problem. Expanding Medicaid, subsidizing insurance premiums, and increasing funding for community health programs could significantly reduce preventable deaths. Until systemic changes occur, individuals must proactively seek out available resources. Skipping check-ups isn’t just a personal choice—it’s a symptom of a broken system that demands urgent reform.

Understanding Medicare Enrollment Periods: Change Your Insurance

You may want to see also

Explore related products

![]()

Delayed Treatment: Without insurance, people postpone care, worsening conditions and increasing mortality risk

Lack of health insurance doesn't just mean skipping checkups; it often translates to delaying critical treatment until it's too late. Imagine a 45-year-old man with persistent chest pain, ignoring it for months because a doctor's visit would mean financial ruin. This scenario isn't hypothetical. Studies show uninsured individuals are 25% more likely to postpone care, even for potentially life-threatening symptoms.

This delay has dire consequences. Conditions like heart disease, cancer, and diabetes, when caught early, often have manageable treatment paths. Left untreated, they progress rapidly, requiring more aggressive (and expensive) interventions. A 2019 study estimated that 13.6% of diabetes-related deaths among uninsured adults could have been prevented with timely access to care. That's not just a statistic; it's thousands of lives lost prematurely.

Think of it as a ticking time bomb. Every day without treatment, the damage compounds. A small, treatable tumor becomes inoperable. Manageable high blood pressure leads to a stroke. The human cost is immeasurable, the financial burden on society staggering.

This isn't just about individual choices; it's a systemic failure. Fear of debt traps people in a cycle of avoidance, leading to worse health outcomes and higher long-term costs for everyone. We need solutions that prioritize preventative care and make healthcare accessible to all, not just those with insurance.

Obtaining Your 1095-B Form: A Guide for Medical Insurance Customers

You may want to see also

Explore related products

![]()

Financial Barriers: High medical costs deter uninsured individuals from seeking life-saving treatments

Each year, an estimated 30,000 Americans die prematurely due to lack of health insurance, according to a Harvard study. This staggering number highlights a grim reality: financial barriers to healthcare can be a matter of life and death. High medical costs often deter uninsured individuals from seeking necessary treatments, even when those treatments are potentially life-saving. For instance, a single diagnostic MRI can cost upwards of $2,600, while a course of chemotherapy can exceed $100,000. Without insurance, these costs are insurmountable for many, leading to delayed or forgone care.

Consider the case of a 45-year-old uninsured individual diagnosed with early-stage colorectal cancer. The recommended treatment includes surgery, followed by six months of chemotherapy. However, faced with a $50,000 surgical bill and additional chemotherapy costs, this person might opt to skip treatment altogether. Studies show that uninsured cancer patients are 80% more likely to die within five years of diagnosis compared to their insured counterparts. This isn’t merely a financial decision—it’s a survival one, forced by economic constraints.

The problem extends beyond catastrophic illnesses. Routine preventive care, such as mammograms or diabetes screenings, often goes unaddressed due to cost concerns. A mammogram can cost $250 without insurance, while annual diabetes management can exceed $1,000. These seemingly small expenses add up, creating a cycle where uninsured individuals avoid care until symptoms become severe—and often irreversible. For example, untreated hypertension can lead to heart attacks or strokes, conditions that are far more expensive to treat than regular medication and monitoring.

To address this crisis, practical steps can be taken. First, uninsured individuals should explore community health clinics, which offer sliding-scale fees based on income. Programs like the Hill-Burton Free and Reduced-Cost Care Program provide discounted services for low-income patients. Second, pharmaceutical assistance programs, such as RxAssist, can reduce medication costs. Finally, advocacy for policy changes, such as expanding Medicaid or creating a public health insurance option, could alleviate systemic financial barriers.

Ultimately, the link between high medical costs and avoidable deaths is undeniable. While individual solutions like community clinics and assistance programs provide temporary relief, systemic reform is essential. Until healthcare becomes accessible to all, thousands will continue to face impossible choices between financial ruin and life-saving treatment. The cost of inaction isn’t just measured in dollars—it’s measured in lives.

Switching Medical Insurance Mid-Year: What You Need to Know

You may want to see also

Explore related products

![]()

Chronic Disease Management: Uninsured struggle to manage conditions like diabetes, raising death rates

Each year, approximately 45,000 Americans die due to lack of health insurance, a stark reminder of the life-or-death consequences of being uninsured. Among these deaths, a significant portion stems from the inability to manage chronic conditions like diabetes, which require consistent care, medication, and monitoring. Without insurance, the uninsured face insurmountable barriers to accessing the tools and treatments necessary to keep their conditions in check, leading to complications that are often fatal.

Consider the daily regimen of a diabetic patient: insulin injections, blood glucose monitoring, and regular doctor visits. For the uninsured, these essentials become luxuries. Insulin, a life-sustaining medication, can cost upwards of $300 per vial without insurance, forcing many to ration doses or skip them entirely. Blood glucose monitors and test strips, critical for tracking sugar levels, add another layer of expense. Over time, uncontrolled diabetes leads to complications like kidney failure, heart disease, and stroke, all of which contribute to higher mortality rates among the uninsured.

The struggle doesn’t end with medication costs. Uninsured individuals often lack access to preventive care, such as annual eye exams to detect diabetic retinopathy or foot exams to prevent ulcers. Without early intervention, these complications progress unchecked, leading to blindness, amputations, and other severe outcomes. For example, a 45-year-old uninsured diabetic is twice as likely to experience a heart attack compared to an insured peer, simply due to inadequate disease management.

Practical steps can mitigate some risks, even without insurance. Community health clinics often offer sliding-scale fees for basic care, and prescription assistance programs like NeedyMeds can reduce medication costs. Generic versions of certain diabetes drugs, such as metformin, are available for as little as $4 per month at pharmacies like Walmart. However, these solutions are stopgaps, not substitutes for comprehensive insurance coverage.

The takeaway is clear: the uninsured face a chronic disease management system rigged against them, with financial barriers at every turn. Until systemic changes address affordability and access, thousands will continue to die unnecessarily each year. For those without insurance, proactive steps—like seeking out low-cost resources and prioritizing diet and exercise—can help, but they cannot replace the safety net of consistent, affordable healthcare.

Emergency Room Visits: Medical Insurance Coverage Explained

You may want to see also

![]()

Emergency Care Reliance: Uninsured often use ERs for primary care, leading to poorer outcomes

Lack of health insurance doesn't just mean skipping checkups. For millions of uninsured Americans, it means relying on emergency rooms (ERs) as their primary source of healthcare. This isn't just inconvenient; it's dangerous.

ERs are designed for acute, life-threatening situations, not routine care. A 2017 study published in the *American Journal of Public Health* found that uninsured individuals were 50% more likely to use the ER for preventable conditions compared to those with insurance. This includes treatable issues like asthma attacks, diabetes management, and even minor infections that could be addressed by a primary care physician.

Imagine managing a chronic condition like diabetes without regular doctor visits, bloodwork, or medication adjustments. An ER visit for a diabetic crisis is far more costly and traumatic than consistent, preventative care. This pattern of delayed, reactive treatment leads to poorer health outcomes, including higher rates of complications, hospitalizations, and even death.

The problem isn't just about individual health. ER reliance by the uninsured strains the entire healthcare system. A 2018 study in *Health Affairs* estimated that uncompensated ER care cost hospitals over $35 billion annually. This financial burden often gets passed on to insured patients through higher premiums and out-of-pocket costs.

It's a vicious cycle: lack of insurance leads to ER reliance, which worsens health and drives up costs for everyone.

Breaking this cycle requires expanding access to affordable, preventative care. This could involve:

- Expanding Medicaid: States that have expanded Medicaid under the Affordable Care Act have seen significant reductions in uninsured rates and ER visits for preventable conditions.

- Community Health Centers: These centers provide primary care services on a sliding scale, making them accessible to low-income individuals.

- Telehealth Services: Remote consultations can bridge the gap for those in rural areas or with limited mobility.

Addressing the root cause of ER reliance – lack of insurance – is crucial for improving individual health, reducing healthcare costs, and creating a more equitable system.

Why Loan Companies Risk Losing Their Insurers: Key Factors Explained

You may want to see also

Frequently asked questions

Studies estimate that approximately 45,000 Americans die annually due to lack of health insurance, as reported by peer-reviewed research, including a 2009 study published in *The American Journal of Public Health*.

Uninsured individuals often delay or forgo necessary medical care, leading to untreated conditions, late diagnoses, and inadequate management of chronic illnesses, which significantly increase the risk of mortality.

The number has fluctuated with changes in healthcare policy and coverage rates. While the Affordable Care Act (ACA) reduced uninsured rates, recent policy shifts and economic factors have led to some increases in uninsured populations, potentially impacting mortality figures.