The issue of how many Americans have died due to lack of health insurance is a critical yet complex topic that intersects public health, policy, and socioeconomic disparities. Studies suggest that uninsured individuals face higher mortality rates compared to those with coverage, primarily because they often delay or forgo necessary medical care due to cost barriers. Research, including a landmark 2009 study by the American Journal of Public Health, estimated that approximately 45,000 deaths annually in the U.S. were associated with lack of health insurance. These fatalities are attributed to preventable conditions, delayed treatments, and inadequate access to healthcare services. While the Affordable Care Act (ACA) has reduced the uninsured rate, millions of Americans remain without coverage, highlighting persistent gaps in the healthcare system and the ongoing need for policy reforms to address this preventable loss of life.

| Characteristics | Values |

|---|---|

| Estimated Annual Deaths Due to Lack of Health Insurance (2019) | 10,000 - 45,000 |

| Source of Estimate | Various studies, including a 2019 study published in the American Journal of Public Health |

| Age Group Most Affected | Working-age adults (18-64) |

| Primary Causes of Death | Delayed or forgone medical care, untreated chronic conditions, and inability to afford necessary medications |

| Impact on Life Expectancy | Lack of insurance is associated with a reduced life expectancy of approximately 1-2 years |

| Disparities by Race/Ethnicity | Uninsured rates are higher among Hispanic and Black Americans, contributing to higher mortality rates in these communities |

| Economic Impact | Estimated $130 billion in annual economic costs due to lost productivity and increased healthcare expenses |

| Policy Implications | Expanding Medicaid and Affordable Care Act (ACA) coverage has been shown to reduce uninsured rates and associated mortality |

| Latest Data Year | 2019 (most recent comprehensive data available) |

| Note | Estimates vary due to differences in methodology and data sources across studies |

Explore related products

What You'll Learn

- Impact on mortality rates: Uninsured Americans face higher death risks due to delayed or forgone care

- Preventable deaths annually: Thousands die yearly from treatable conditions without insurance access

- Demographic disparities: Low-income, minority groups suffer disproportionately from lack of coverage

- Economic consequences: Uninsured deaths strain healthcare systems and increase societal costs

- Policy implications: Expanding coverage could significantly reduce preventable deaths nationwide

![]()

Impact on mortality rates: Uninsured Americans face higher death risks due to delayed or forgone care

Lack of health insurance doesn't just mean skipping checkups or paying out-of-pocket for prescriptions. It's a matter of life and death. Studies consistently show that uninsured Americans face a significantly higher risk of premature death compared to their insured counterparts. A 2017 analysis by the Commonwealth Fund estimated that 26,100 working-age adults die annually in the U.S. due to lack of health insurance. This staggering number highlights a stark reality: being uninsured isn't just a financial burden, it's a mortal threat.

Imagine a 45-year-old man experiencing chest pains. With insurance, he'd likely seek immediate medical attention, potentially catching a heart attack early. Without insurance, fearing the cost, he might delay seeking help, increasing the risk of a fatal outcome. This scenario isn't hypothetical; it's a tragic reality for thousands.

The reasons behind this increased mortality are multifaceted. Delayed care is a major culprit. Without insurance, individuals often postpone seeking medical attention until symptoms become severe, making conditions harder to treat. A minor infection, left untreated, can escalate into sepsis. A persistent cough, ignored due to cost concerns, could be an early sign of lung cancer. Preventive care, crucial for early detection and management of chronic conditions, is often inaccessible to the uninsured. Regular screenings for cancer, diabetes, and heart disease can identify problems at manageable stages, but without insurance, these lifesaving measures are often out of reach.

Chronic disease management suffers as well. Uninsured individuals with conditions like diabetes, hypertension, or asthma struggle to afford medications and regular monitoring, leading to complications and increased mortality risk.

The impact isn't limited to physical health. The stress and anxiety of being uninsured, coupled with the constant fear of illness or injury, take a toll on mental health. This can lead to depression, anxiety disorders, and even suicidal ideation, further exacerbating the mortality risk.

Addressing this crisis requires a multi-pronged approach. Expanding access to affordable health insurance is paramount. Policies like Medicaid expansion have proven effective in reducing uninsured rates and improving health outcomes. Additionally, increasing funding for community health centers and free clinics can provide a safety net for those who remain uninsured. Finally, promoting health literacy and encouraging preventive care practices can empower individuals to take charge of their health, even with limited resources.

Is Catastrophic Health Insurance a Smart Financial Safety Net?

You may want to see also

Explore related products

![]()

Preventable deaths annually: Thousands die yearly from treatable conditions without insurance access

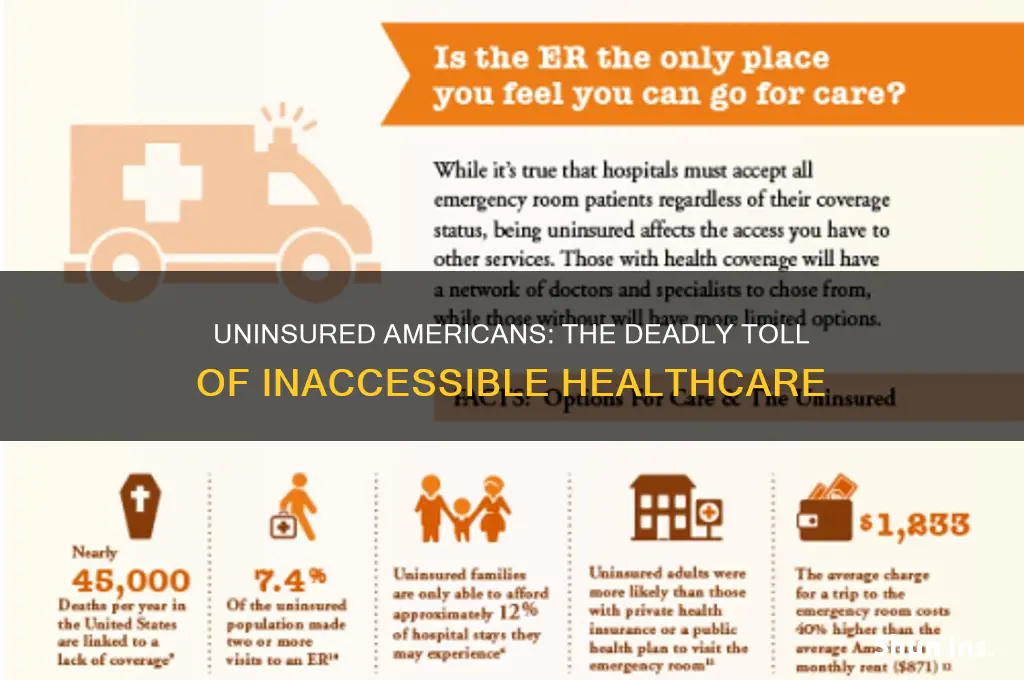

Each year, an estimated 30,000 Americans die prematurely due to lack of health insurance. This staggering number represents lives lost not to untreatable diseases, but to conditions manageable with timely medical intervention. Diabetes, hypertension, and certain cancers, when caught early, have high survival rates. Yet, without insurance, individuals often delay care, forgo screenings, and face financial barriers to life-saving treatments. This isn't merely a statistic—it's a stark reminder of the human cost of systemic gaps in healthcare access.

Consider the case of a 45-year-old uninsured individual with undiagnosed type 2 diabetes. Without regular check-ups, their blood sugar levels go unchecked, leading to complications like kidney failure or heart disease. A simple A1C test, costing around $50, could detect the condition early. Yet, for someone without insurance, this expense is often prohibitive. By the time symptoms become severe enough to seek emergency care, the disease has progressed to a critical stage, drastically reducing survival odds. This scenario isn't rare—it's a recurring tragedy in a system where cost dictates care.

The financial burden of being uninsured extends beyond individual health. Uninsured patients often rely on emergency rooms for treatment, which is not only more expensive but also less effective for chronic conditions. For instance, managing hypertension with regular medication and monitoring costs approximately $500 annually. Without insurance, this expense is unaffordable for many, leading to strokes or heart attacks that could have been prevented. The irony? Treating these emergencies costs tens of thousands of dollars, burdening both the individual and the healthcare system.

Addressing this crisis requires systemic change, but individuals can take steps to mitigate risks. Community health clinics offer low-cost screenings and treatments, though availability varies by region. Non-profit organizations like the HealthWell Foundation provide financial assistance for medications. For those under 65, exploring Affordable Care Act (ACA) plans during open enrollment can offer subsidized coverage. While these solutions aren't perfect, they provide a lifeline for those navigating the precarious landscape of uninsured healthcare.

Ultimately, the thousands of preventable deaths each year are a call to action. They highlight the moral and practical failures of a system that ties health to wealth. Until comprehensive reform is achieved, raising awareness, advocating for policy changes, and utilizing available resources remain critical. Lives depend on it—not in the abstract, but in the concrete reality of neighbors, friends, and family members who deserve access to care that could save them.

Oscar Insurance and Medicaid: What You Need to Know

You may want to see also

Explore related products

$9.97

$8.27 $12.99

![]()

Demographic disparities: Low-income, minority groups suffer disproportionately from lack of coverage

The lack of health insurance in the United States disproportionately affects low-income and minority communities, exacerbating existing health disparities. Studies indicate that uninsured individuals are more likely to delay or forgo necessary medical care, leading to poorer health outcomes and higher mortality rates. For instance, a 2009 study published in the *American Journal of Public Health* estimated that approximately 45,000 deaths annually in the U.S. were associated with lack of health insurance, with low-income and minority groups bearing the brunt of these fatalities. This disparity highlights the urgent need to address systemic barriers to healthcare access.

Consider the case of African American and Hispanic populations, who are twice as likely as their white counterparts to be uninsured. These groups often face intersecting challenges, such as lower wages, limited job benefits, and geographic barriers to healthcare facilities. For example, in rural areas, where 15% of the population is uninsured compared to 9% in urban areas, minority groups are overrepresented. Without insurance, preventive services like cancer screenings, diabetes management, and hypertension control become inaccessible, leading to preventable complications and deaths. A 2020 analysis revealed that uninsured Black adults were 30% less likely to receive timely cancer diagnoses, significantly reducing survival rates.

To combat these disparities, targeted interventions are essential. Expanding Medicaid eligibility under the Affordable Care Act (ACA) has proven effective, reducing uninsured rates among low-income adults by 50% in states that adopted the expansion. However, 10 states have yet to expand Medicaid, leaving millions of eligible individuals—disproportionately people of color—without coverage. Community health centers, which serve 1 in 5 low-income Americans, play a critical role but require sustained funding to meet demand. Additionally, culturally competent outreach programs can improve enrollment rates by addressing language barriers and mistrust of healthcare systems.

A comparative analysis of health outcomes between insured and uninsured populations underscores the stakes. Uninsured individuals are 25% more likely to die prematurely from treatable conditions like heart disease and stroke. For low-income families, the financial burden of medical debt often compounds health issues, creating a cycle of poverty and illness. Practical steps, such as enrolling in ACA marketplace plans during open enrollment or utilizing sliding-scale clinics, can mitigate risks. Policymakers must also prioritize closing coverage gaps by addressing racial and economic inequities embedded in healthcare systems.

Ultimately, the demographic disparities in health insurance coverage are not merely statistical anomalies but reflections of deeper systemic injustices. Low-income and minority groups face structural barriers that limit their access to life-saving care, resulting in preventable deaths. By implementing evidence-based policies, increasing funding for safety-net programs, and fostering community engagement, society can begin to dismantle these disparities. The lives saved will not only be a measure of policy success but a testament to the value of equity in healthcare.

Mental Health Rider: A Crucial Addition to Disability Insurance Coverage

You may want to see also

Explore related products

![]()

Economic consequences: Uninsured deaths strain healthcare systems and increase societal costs

The economic toll of uninsured deaths in the United States extends far beyond individual tragedies, creating a ripple effect that strains healthcare systems and inflates societal costs. Studies estimate that approximately 45,000 Americans die annually due to lack of health insurance, a statistic that underscores the human cost of inaccessibility. These preventable deaths are not isolated incidents but symptoms of a systemic issue that perpetuates financial burdens on hospitals, taxpayers, and the broader economy. When uninsured individuals forgo preventive care or delay treatment, their conditions often worsen, leading to more expensive emergency interventions that could have been avoided with timely, affordable care.

Consider the financial mechanics of this crisis. Uninsured patients frequently rely on emergency departments as their primary source of care, a costly alternative to routine outpatient services. For instance, treating an advanced stage of diabetes or cancer in an emergency setting can cost upwards of $50,000 per episode, compared to a fraction of that for early intervention. Hospitals absorb much of this uncompensated care, shifting the burden to insured patients through higher premiums and to taxpayers via government subsidies. This cost-shifting mechanism not only destabilizes healthcare financing but also reduces resources available for other critical services, such as mental health programs or rural healthcare initiatives.

From a societal perspective, the economic consequences of uninsured deaths extend into lost productivity and workforce depletion. Premature deaths among working-age adults rob the economy of contributors, reducing tax revenues and straining social safety nets like Social Security and Medicare. For example, a 40-year-old uninsured worker who dies from untreated hypertension represents not only a personal loss but also an estimated $1.2 million in lost lifetime earnings and economic contributions. Multiply this by thousands of cases annually, and the macroeconomic impact becomes staggering, hindering growth and exacerbating income inequality.

Addressing this crisis requires a dual approach: expanding access to affordable insurance and incentivizing preventive care. Policymakers could consider subsidizing premiums for low-income individuals or implementing community health programs that offer screenings and early interventions at minimal cost. Employers can play a role by providing wellness initiatives that reduce risk factors for chronic diseases, potentially lowering healthcare costs for both workers and companies. While these solutions demand upfront investment, they pale in comparison to the long-term savings achieved by reducing preventable deaths and their associated economic fallout.

Ultimately, the economic consequences of uninsured deaths are a stark reminder that healthcare is not just a moral imperative but a financial one. By treating this issue as a systemic problem rather than a series of individual failures, society can alleviate the strain on healthcare systems, reduce societal costs, and foster a more resilient economy. The price of inaction is measured not only in lives lost but in dollars wasted—a cost no nation can afford to ignore.

Escape IRS Medical Insurance: Strategies for Opting Out

You may want to see also

Explore related products

$9.98 $12.99

$14.8 $18.99

![]()

Policy implications: Expanding coverage could significantly reduce preventable deaths nationwide

Lack of health insurance is a silent killer in the United States, contributing to an estimated 30,000 preventable deaths annually. This staggering number highlights a critical gap in the healthcare system, where financial barriers often stand between individuals and life-saving care. Expanding health insurance coverage isn’t just a policy goal—it’s a moral imperative with the potential to save tens of thousands of lives each year. By ensuring access to preventive care, early disease detection, and timely treatment, expanded coverage could dramatically reduce mortality rates tied to conditions like heart disease, cancer, and diabetes.

Consider the practical steps required to achieve this goal. Policymakers could start by lowering eligibility barriers for Medicaid, ensuring that low-income adults in all states have access to affordable coverage. Simultaneously, subsidies for private insurance plans under the Affordable Care Act should be expanded to make premiums more manageable for middle-income families. For example, increasing the income threshold for subsidies from 400% to 600% of the federal poverty level could cover an additional 4 million uninsured Americans. Pairing these measures with public awareness campaigns about enrollment opportunities could further bridge the coverage gap.

Critics often argue that expanding coverage would strain state and federal budgets, but the long-term cost savings are undeniable. Preventive care reduces the need for expensive emergency treatments, while early disease management lowers hospitalization rates. For instance, a study by the Urban Institute found that states expanding Medicaid saw a 6% reduction in preventable hospitalizations within just two years. By investing in coverage expansion, policymakers aren’t just saving lives—they’re creating a healthier, more productive population that contributes to economic growth.

Finally, the moral and ethical dimensions of this issue cannot be ignored. In a nation with the resources to provide universal healthcare, allowing preventable deaths due to lack of insurance is a failure of collective responsibility. Expanding coverage isn’t just about numbers—it’s about ensuring that no one is left behind. Practical tips for advocates include highlighting success stories from states with expanded Medicaid, such as Kentucky, where uninsured rates dropped by 50% and mortality rates declined significantly. By framing this as both a policy and humanitarian issue, advocates can build a compelling case for immediate action.

Keeping College Students Covered: Health Insurance Tips for Parents

You may want to see also

Frequently asked questions

Studies estimate that approximately 45,000 Americans die annually due to lack of health insurance, as reported by peer-reviewed research such as the 2009 study published in *The American Journal of Public Health*.

Uninsured individuals often delay or forgo necessary medical care, leading to untreated conditions, late diagnoses, and inadequate management of chronic illnesses, which contribute to higher mortality rates.

Yes, the Affordable Care Act (ACA) reduced the uninsured rate, potentially saving lives. However, recent policy changes and gaps in coverage mean the issue persists, though the exact impact on mortality varies by study.

Yes, low-income individuals, racial and ethnic minorities, and those in states without Medicaid expansion are disproportionately affected by higher mortality rates due to lack of health insurance.