The topic of how many artists have health insurance sheds light on a critical yet often overlooked aspect of the creative industry. Artists, including musicians, painters, writers, and performers, frequently face unique challenges in accessing affordable and comprehensive healthcare due to the unpredictable nature of their income, freelance work status, and lack of employer-sponsored benefits. Studies and surveys have shown that a significant portion of artists remain uninsured or underinsured, leaving them vulnerable to financial strain in the event of illness or injury. This issue not only impacts individual artists but also has broader implications for the sustainability and diversity of the arts community. Understanding the scope of this problem is essential for advocating policy changes, creating support systems, and fostering a healthier environment for artists to thrive.

Explore related products

What You'll Learn

- Insurance Rates for Artists: Percentage of artists with health insurance compared to national averages

- Freelance vs. Employed Artists: Coverage differences between independent and employed artists in the industry

- Geographic Disparities: How location impacts artists' access to health insurance options

- Affordable Care Act Impact: Effects of ACA on artists' health insurance enrollment and costs

- Industry Support Programs: Availability of health insurance initiatives tailored for artists and creatives

![]()

Insurance Rates for Artists: Percentage of artists with health insurance compared to national averages

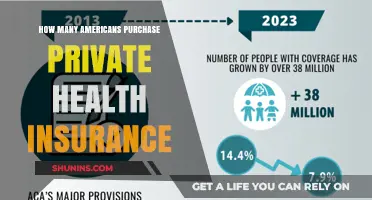

Artists in the United States face a unique challenge when it comes to health insurance coverage. According to a 2020 report by Americans for the Arts, only 29% of artists have employer-sponsored health insurance, compared to 56% of the general workforce. This disparity highlights the precarious nature of artistic careers, where freelance and gig-based work often lack the benefits associated with traditional employment. The result? A significant gap in coverage that leaves many artists vulnerable to financial strain in the event of illness or injury.

To understand the scope of this issue, consider the national averages. As of 2021, approximately 91.4% of Americans had some form of health insurance, whether through employers, government programs, or private plans. When compared to the artist-specific data, it becomes clear that artists are disproportionately uninsured. For instance, while 59% of Americans aged 18–64 have employer-sponsored insurance, artists in the same age group are nearly half as likely to enjoy this benefit. This gap widens further when examining artists in lower-income brackets, who often cannot afford private plans and may not qualify for subsidies.

One practical step artists can take to bridge this gap is to explore state-based health insurance marketplaces, which offer subsidized plans under the Affordable Care Act (ACA). For example, a 30-year-old artist earning $30,000 annually in New York might qualify for a Silver plan with a monthly premium of $150 or less after tax credits. Additionally, organizations like the Actors Fund and Artist Health Insurance Resource Center provide tailored guidance and resources for navigating coverage options. These tools can help artists make informed decisions and secure affordable plans.

However, systemic changes are also necessary to address this disparity. Advocacy groups are pushing for policies that extend employer-sponsored insurance to gig workers and freelancers, who make up a significant portion of the artistic community. For instance, the Freelance Isn’t Free Act, enacted in New York City, ensures payment protections for freelancers but does not yet include health benefits. Expanding such legislation to include insurance provisions could be a game-changer for artists nationwide. Until then, artists must remain proactive in seeking coverage, leveraging available resources, and advocating for their rights.

In conclusion, while the percentage of artists with health insurance lags behind national averages, actionable steps and policy changes can help close this gap. By combining individual initiative with collective advocacy, artists can secure the coverage they need to thrive in their careers without sacrificing their health or financial stability.

Texas Health Insurance Guide: Simple Steps to Apply and Enroll

You may want to see also

Explore related products

![]()

Freelance vs. Employed Artists: Coverage differences between independent and employed artists in the industry

The health insurance landscape for artists is starkly divided between freelancers and their employed counterparts. Employed artists, often tied to institutions like theaters, galleries, or media companies, typically enjoy employer-sponsored health plans. These plans, mandated by the Affordable Care Act for companies with 50+ employees, cover essentials like doctor visits, prescriptions, and hospitalization. For instance, a full-time museum curator might pay 20-30% of a premium costing $600/month, with the employer covering the rest. Freelancers, however, face a different reality. Without an employer to subsidize costs, they must navigate the individual market, where premiums average $452/month for a benchmark plan in 2023. This disparity leaves many independent artists uninsured or underinsured, with 24% lacking coverage compared to just 8% of employed artists, according to a 2022 Americans for the Arts report.

Consider the case of a freelance graphic designer versus a salaried art director. The art director, employed by a marketing firm, likely receives a health plan with a $2,000 deductible and access to a preferred provider network. The freelancer, earning $40,000 annually, might opt for a bronze-level ACA plan with a $7,000 deductible to keep monthly premiums under $300. This higher deductible means the freelancer pays more out-of-pocket before coverage kicks in, often delaying necessary care. Additionally, freelancers must allocate time to research plans, manage enrollment periods, and handle all paperwork—tasks an HR department would typically oversee for employed artists.

The coverage gap extends beyond premiums and deductibles. Employed artists often receive supplemental benefits like dental, vision, and mental health services as part of their package. Freelancers, even when insured, frequently face limited provider networks or exclusions for specialized care. For example, a dancer with a work-related injury might find physical therapy capped at 20 sessions annually under a freelance plan, while an employed dancer’s plan could offer unlimited visits. This disparity highlights how employment status directly impacts access to comprehensive care, particularly in fields where physical health is integral to the job.

To bridge this gap, freelancers can explore alternatives like joining professional organizations that offer group health plans. The Freelancers Union, for instance, provides members access to plans with reduced rates through collective bargaining. Another strategy is leveraging tax deductions for health insurance premiums, available to self-employed individuals who meet IRS criteria. Employed artists, meanwhile, should maximize their benefits by understanding their plan’s specifics—for example, using flexible spending accounts (FSAs) to cover copays or prescription costs. Both groups must stay informed about policy changes, such as ACA subsidies extended through 2025, which can significantly lower costs for freelancers earning up to 200% of the federal poverty level.

Ultimately, the freelance-employed divide in health coverage underscores the need for systemic solutions. While employed artists benefit from structured support, freelancers must advocate for themselves, piecing together coverage in a fragmented system. Policymakers, arts organizations, and artists themselves must collaborate to expand affordable options, ensuring that health insurance becomes a right, not a privilege, for all creators. Until then, understanding these differences empowers artists to make informed choices, protecting both their health and their careers.

Aetna Medical Insurance: Dental Implant Coverage Explained

You may want to see also

Explore related products

$72.06 $129.99

$62.15 $116.95

![]()

Geographic Disparities: How location impacts artists' access to health insurance options

Artists in rural areas face starkly different health insurance landscapes compared to their urban counterparts. In the United States, for instance, rural artists often contend with limited access to healthcare providers, which directly affects their insurance options. Many rural counties lack hospitals or clinics, forcing artists to travel long distances for care. This geographic isolation not only increases out-of-pocket costs but also discourages regular check-ups, preventive care, and timely treatment. For example, a study by the National Endowment for the Arts found that rural artists are 20% less likely to have health insurance compared to urban artists. This disparity highlights how location can exacerbate financial and health vulnerabilities for artists already operating on tight budgets.

In contrast, urban artists benefit from denser healthcare networks and a wider array of insurance plans. Cities like New York, Los Angeles, and Chicago offer marketplaces with multiple insurers, including plans tailored to freelancers and gig workers. However, affordability remains a challenge. Urban living expenses, including high premiums, often outpace artists’ earnings. For instance, a freelance musician in New York City might spend upwards of $400 monthly on a mid-tier plan, a significant portion of their income. Despite these costs, urban artists are statistically more likely to be insured due to greater awareness of available options and proximity to resources like healthcare navigators or artist advocacy groups.

Internationally, geographic disparities in health insurance for artists become even more pronounced. In countries with universal healthcare, such as Canada or the UK, artists in remote regions still face barriers like long wait times and limited specialist availability. Conversely, in countries without universal coverage, like Mexico or India, artists in rural areas are often entirely uninsured, relying on out-of-pocket payments or community health programs. For example, in Mexico, only 30% of artists in rural areas report having any form of health insurance, compared to 60% in urban centers like Mexico City. This global perspective underscores how national healthcare policies interact with geography to shape artists’ access to care.

To navigate these disparities, artists must adopt location-specific strategies. Rural artists can explore telehealth services, which bridge the gap in provider availability, though this requires reliable internet access. Urban artists, meanwhile, should leverage local artist collectives or unions that negotiate group insurance rates. For instance, the Actors Fund in the U.S. offers subsidized plans for performing artists in major cities. Internationally, artists in countries without universal healthcare can seek out NGO-sponsored programs or cross-border insurance options, though these often come with restrictions. Regardless of location, artists must proactively research and advocate for their health insurance needs, as geographic disparities will persist without systemic change.

Top Pregnancy Health Insurance Plans: Comprehensive Coverage for Expecting Moms

You may want to see also

Explore related products

![]()

Affordable Care Act Impact: Effects of ACA on artists' health insurance enrollment and costs

The Affordable Care Act (ACA) has significantly reshaped the health insurance landscape for artists, a demographic historically underserved by traditional employer-based coverage. Before the ACA, many artists relied on sporadic freelance work, making them ineligible for group plans and often unable to afford individual policies. The ACA’s introduction of subsidies, guaranteed issue, and expanded Medicaid eligibility addressed these barriers, increasing enrollment rates among artists. For instance, states that expanded Medicaid saw a 24% increase in coverage for low-income adults, a category many artists fall into due to fluctuating incomes. This shift underscores the ACA’s role in making health insurance more accessible to this creative workforce.

One of the ACA’s most impactful provisions for artists is the premium tax credit, which reduces monthly insurance costs for individuals earning between 100% and 400% of the federal poverty level. For a single artist earning $30,000 annually, this could translate to savings of $200–$300 per month on a benchmark Silver plan. However, the complexity of navigating these subsidies remains a challenge. Artists often struggle to estimate their annual income accurately, risking over- or underpayment of premiums. To mitigate this, tools like the Healthcare.gov subsidy calculator and consultations with certified navigators can help artists maximize their benefits while avoiding repayment penalties during tax season.

Despite the ACA’s advancements, out-of-pocket costs remain a hurdle for many artists. High deductibles and copays can deter individuals from seeking care, even with subsidized premiums. For example, a Bronze plan, often the most affordable option, may have a deductible exceeding $7,000, leaving artists vulnerable to financial strain in the event of a medical emergency. To address this, some artists have turned to health sharing ministries or short-term plans, though these alternatives lack ACA protections like coverage for pre-existing conditions. Balancing affordability with comprehensive coverage requires careful consideration of individual health needs and financial stability.

A comparative analysis reveals that the ACA’s impact on artists varies by state, particularly regarding Medicaid expansion. In expansion states, artists earning up to $18,754 annually (for a single individual) qualify for Medicaid, offering near-zero-cost coverage. In non-expansion states, however, artists in the “coverage gap”—earning too much for Medicaid but too little for subsidies—face limited options. This disparity highlights the need for federal and state collaboration to close coverage gaps and ensure equitable access. For artists in non-expansion states, exploring local clinics, sliding-scale providers, or artist-specific health funds can provide temporary relief while advocating for policy change.

Ultimately, the ACA has been a game-changer for artists’ health insurance enrollment, but its success is incomplete. While enrollment rates have risen, cost barriers persist, and awareness of available resources remains low. Artists can take proactive steps by enrolling during the annual Open Enrollment Period (November 1–January 15), leveraging state-based marketplaces for localized options, and joining advocacy groups like the Artists’ Health Insurance Resource Center. By combining individual action with collective advocacy, artists can further amplify the ACA’s impact and secure a healthier, more sustainable future for their community.

Disability Insurance and Medicaid: Can You Have Both?

You may want to see also

Explore related products

$19.98 $26.99

$9.09 $10.99

![]()

Industry Support Programs: Availability of health insurance initiatives tailored for artists and creatives

Artists and creatives often face unique challenges in accessing health insurance due to the freelance and gig-based nature of their work. Unlike traditional employees, many artists do not have employer-sponsored plans, leaving them to navigate the complex and often costly individual insurance market. This gap in coverage has spurred the development of industry-specific support programs designed to address their needs. Initiatives like these are not just about providing insurance; they aim to foster sustainability in creative careers by ensuring artists can focus on their work without the constant worry of healthcare costs.

One notable example is the Artists’ Health Insurance Resource Center (AHIRC), which offers tailored guidance and resources for artists to find affordable coverage. AHIRC collaborates with organizations like the Actors Fund and Freelancers Union to provide state-specific options, subsidies, and even group plans for artists. For instance, in New York, the Artists’ Health Insurance Access Program subsidizes premiums for eligible artists, reducing monthly costs by up to 50%. Such programs demonstrate how targeted initiatives can bridge the gap between artists’ financial realities and the need for comprehensive healthcare.

Another innovative approach is the Freelancers Insurance Company, a nonprofit insurer created by the Freelancers Union. This program offers health, dental, and vision plans specifically designed for independent workers, including artists. By pooling freelancers into a collective, the program negotiates lower rates and provides plans that cater to fluctuating incomes. For example, artists can choose plans with lower monthly premiums and higher deductibles during slower work periods, adjusting coverage as their income changes. This flexibility is crucial for a workforce with unpredictable earnings.

However, the availability of such programs varies widely by region, leaving many artists in underserved areas without access. In states with fewer resources, artists often rely on federal programs like the Affordable Care Act (ACA) marketplace, where they may qualify for subsidies based on income. For instance, an artist earning 200% of the federal poverty level ($28,000 annually for a single individual in 2023) could receive substantial premium tax credits, making insurance more affordable. Yet, navigating these options requires time and expertise, underscoring the need for localized support systems.

To maximize the impact of these initiatives, artists should proactively research and engage with available programs. Start by checking state-specific resources, such as arts councils or creative worker alliances, which often maintain updated lists of insurance options. Additionally, joining professional organizations like the National Endowment for the Arts or Americans for the Arts can provide access to exclusive benefits, including discounted insurance plans. Finally, artists should consider forming cooperatives or advocacy groups to push for expanded coverage options, as collective action has proven effective in driving policy changes.

In conclusion, while health insurance remains a significant challenge for artists, industry-specific support programs offer viable solutions. From subsidized plans to flexible coverage options, these initiatives are tailored to the unique needs of creatives. By leveraging available resources and advocating for broader access, artists can secure the healthcare they need to thrive in their careers.

Applying for Welfare Insurance: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Studies suggest that only about 30-40% of artists in the U.S. have consistent health insurance, often due to freelance or gig-based work and lack of employer-provided benefits.

Many artists work independently or in part-time roles that do not offer health benefits, and the cost of private insurance is often prohibitive for those with fluctuating or low incomes.

Yes, organizations like the Actors Fund, Artists’ Health Insurance Resource Center, and state-based marketplaces offer resources and assistance for artists to find affordable health insurance options.

Without health insurance, artists often delay or forgo medical care, which can lead to untreated health issues, financial strain, and reduced productivity, ultimately affecting their ability to sustain their careers.