California has made significant strides in expanding health insurance coverage over the past decade, largely due to the implementation of the Affordable Care Act (ACA) and the state's own initiatives, such as Covered California. As of recent data, approximately 93% of Californians have health insurance, a notable increase from pre-ACA levels. This coverage is distributed across various sources, including employer-sponsored plans, Medi-Cal (California's Medicaid program), Medicare, and individual market plans. Despite this progress, disparities persist, particularly among low-income populations, undocumented immigrants, and certain racial and ethnic groups, highlighting ongoing challenges in achieving universal coverage. Efforts to further reduce the uninsured rate continue through policy reforms, outreach programs, and discussions about expanding access to affordable care.

Explore related products

What You'll Learn

![]()

Coverage Rates by Age Group

California's health insurance landscape reveals a striking disparity in coverage rates across age groups, with younger adults often lagging behind their older counterparts. Data from the California Health Interview Survey (CHIS) highlights that while over 95% of Californians aged 65 and older are insured—primarily through Medicare—coverage dips significantly for those aged 26 to 34. In this demographic, only about 85% have insurance, despite being in their prime working years. This gap underscores the challenges young adults face, from navigating employer-based plans to affording individual policies, and points to the need for targeted interventions to bridge this coverage divide.

To address the coverage gap among younger Californians, policymakers and employers must collaborate on solutions tailored to this age group. For instance, expanding access to affordable, short-term plans or enhancing subsidies for those earning just above the Medi-Cal threshold could make a tangible difference. Additionally, educational campaigns aimed at 26- to 34-year-olds—who often lose parental coverage upon aging out—could clarify enrollment processes and emphasize the long-term benefits of continuous insurance. Practical steps, such as simplifying application procedures and integrating enrollment options into digital platforms frequented by this demographic, could further boost participation.

A comparative analysis of age-based coverage rates in California reveals both successes and areas for improvement. While seniors enjoy near-universal coverage, children under 18 also fare well, with over 97% insured, largely due to programs like Medi-Cal and the Children’s Health Insurance Program (CHIP). In contrast, the 19-to-25 age group shows moderate coverage at around 90%, benefiting from provisions allowing them to remain on parental plans. However, the drop-off in the 26-to-34 cohort suggests a systemic issue at the transition to full financial independence, warranting a closer look at policy and market barriers.

Persuasively, closing the coverage gap among younger adults isn’t just a matter of health equity—it’s an economic imperative. Uninsured individuals aged 26 to 34 are more likely to delay preventive care, leading to costlier treatments down the line. By ensuring this group has access to affordable, comprehensive insurance, California can reduce overall healthcare expenditures and foster a healthier, more productive workforce. Employers, too, stand to gain from healthier employees, with reduced absenteeism and improved productivity. Investing in targeted solutions today will yield dividends for both individuals and the state’s economy tomorrow.

Top Companies Offering Gap Insurance: Protect Your Vehicle Investment

You may want to see also

Explore related products

![]()

Employer-Sponsored vs. Individual Plans

In California, approximately 93% of residents have health insurance, with employer-sponsored plans covering about 55% of the insured population. This dominance highlights the critical role workplaces play in providing healthcare access, yet it also underscores the reliance on employment for a fundamental need. For the remaining 45%, individual plans through Covered California or private insurers are the primary options, offering flexibility but often at a higher cost. This divide raises questions about affordability, coverage quality, and the stability of health insurance in a fluctuating job market.

Consider the financial implications: employer-sponsored plans typically share costs between the employer and employee, reducing individual premiums by an average of 70-80%. For a family plan, this could mean saving $10,000 annually compared to an individual market plan. However, these plans are tied to employment, leaving workers vulnerable during job transitions. Individual plans, while pricier, offer portability and customization, such as selecting specific networks or higher deductibles to lower monthly costs. For instance, a healthy 30-year-old might opt for a Bronze plan with a $7,000 deductible, paying $250 monthly instead of $500 for a Gold plan.

The coverage itself differs subtly but significantly. Employer plans often include comprehensive benefits like dental, vision, and wellness programs, whereas individual plans may require purchasing these separately. Additionally, employer plans are less likely to exclude pre-existing conditions due to group underwriting, while individual plans must adhere to ACA standards but may have narrower provider networks. For example, a specialist in Los Angeles might be in-network for an employer plan but out-of-network for an individual plan, impacting out-of-pocket costs.

For those weighing their options, assess job stability and long-term health needs. If you’re in a secure role with a robust benefits package, an employer plan is likely the better value. However, freelancers, part-time workers, or those anticipating career shifts may benefit from the flexibility of an individual plan. Practical tip: use Covered California’s subsidy calculator to estimate potential savings on individual plans, as 70% of enrollees qualify for financial assistance, reducing premiums by an average of $500 monthly.

Ultimately, the choice between employer-sponsored and individual plans hinges on balancing cost, coverage, and personal circumstances. While employer plans offer affordability and comprehensive benefits, individual plans provide stability and customization, particularly for those outside traditional employment structures. Understanding these nuances ensures Californians can navigate their options effectively, securing coverage that aligns with their health and financial needs.

Get Certified for Medical Insurance Jobs in New Jersey

You may want to see also

Explore related products

![]()

Medicaid Enrollment Statistics

California's Medicaid program, known as Medi-Cal, has seen significant enrollment growth over the past decade, reflecting both policy changes and demographic shifts. As of 2023, approximately 14.6 million Californians are enrolled in Medi-Cal, accounting for about 37% of the state’s population. This figure underscores the program’s role as a critical safety net, particularly for low-income individuals, families, and children. The expansion of Medi-Cal under the Affordable Care Act (ACA) in 2014 played a pivotal role in this increase, extending eligibility to adults without dependent children and raising the income threshold to 138% of the federal poverty level. This expansion not only reduced the uninsured rate in California but also highlighted the program’s adaptability to evolving healthcare needs.

Analyzing enrollment trends reveals disparities across age groups and regions. Children under 18 represent the largest demographic, with over 5 million enrollees, as Medi-Cal covers nearly half of California’s pediatric population. Adults aged 19 to 64 make up another substantial portion, with enrollment spiking during the COVID-19 pandemic due to economic hardships and the continuous enrollment provision under the Public Health Emergency. However, rural counties like Madera and Merced report higher enrollment rates compared to urban areas like San Francisco, reflecting varying economic conditions and access to employer-sponsored insurance. These regional differences emphasize the need for targeted outreach and resources to ensure equitable access to Medi-Cal.

A closer look at enrollment statistics also reveals the program’s impact on specific populations. Pregnant women, for instance, benefit from Medi-Cal’s extended coverage, which includes prenatal and postpartum care for incomes up to 213% of the federal poverty level. Similarly, seniors and individuals with disabilities account for a smaller but significant share of enrollees, relying on Medi-Cal for long-term care services not covered by Medicare. Understanding these nuances is crucial for policymakers and advocates working to strengthen the program’s effectiveness and address gaps in coverage.

To maximize Medi-Cal’s reach, practical steps can be taken at both the individual and systemic levels. For individuals, staying informed about eligibility criteria and renewal processes is essential, as redeterminations resumed in 2023 after a pandemic-related pause. Community organizations can play a key role by offering enrollment assistance and translating materials into multiple languages to serve California’s diverse population. At the policy level, maintaining funding for outreach efforts and simplifying the application process could further boost enrollment, particularly among underserved groups. By leveraging these strategies, California can continue to build on Medi-Cal’s success as a cornerstone of its healthcare system.

Medical Insurance Premiums: Social Security Tax Exemption?

You may want to see also

Explore related products

![]()

Uninsured Population Demographics

California boasts one of the lowest uninsured rates in the nation, yet pockets of vulnerability persist. Understanding the demographics of the uninsured is crucial for targeted interventions. Data reveals a disproportionate burden among younger adults aged 18-34, who comprise roughly 30% of the uninsured population despite representing only 22% of the state's total population. This disparity highlights the need for tailored outreach and enrollment strategies that resonate with this age group, potentially leveraging social media and digital platforms.

Income emerges as another critical factor. Individuals living below the federal poverty level are significantly more likely to lack coverage, with nearly 15% of this demographic uninsured compared to just 4% of those with incomes above 400% of the poverty line. This stark contrast underscores the importance of expanding access to affordable coverage options, such as Medi-Cal, and addressing barriers like complex enrollment processes and lack of awareness about available subsidies.

Ethnicity and immigration status further complicate the picture. Latinos, who constitute 39% of California's population, account for a staggering 60% of the uninsured. This disparity is partly attributable to higher rates of undocumented residents within this community, as they are ineligible for most public coverage programs. Addressing this gap requires innovative solutions like state-funded programs or community-based initiatives that provide culturally competent care regardless of immigration status.

Geographic disparities also play a role. Rural counties, particularly in the Central Valley and Inland Empire, consistently report higher uninsured rates than urban areas. Limited provider networks, transportation challenges, and lower median incomes contribute to this divide. Expanding telehealth services, incentivizing healthcare providers to practice in underserved areas, and increasing funding for community health centers are essential strategies to bridge this gap.

Ultimately, dismantling barriers to coverage requires a multi-pronged approach that acknowledges the intersecting demographics of the uninsured. By tailoring solutions to the unique needs of specific populations – whether through targeted outreach, expanded eligibility, or innovative service delivery models – California can continue to make strides toward universal healthcare access. This demands collaboration between policymakers, healthcare providers, community organizations, and advocates to ensure that no Californian is left behind.

Understanding Medicare Broker Payment Structures

You may want to see also

Explore related products

![]()

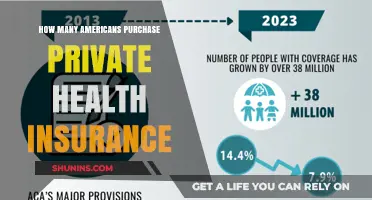

Impact of Affordable Care Act

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the healthcare landscape in California, particularly in terms of insurance coverage. Since its implementation, the uninsured rate in the state has plummeted from 17% in 2013 to approximately 7% in recent years, according to data from the California Health Care Foundation. This dramatic reduction highlights the ACA’s role in expanding access to health insurance, especially for low-income individuals and families. By establishing Covered California, the state’s health insurance marketplace, the ACA provided a platform for residents to compare and purchase affordable plans, often with subsidies that reduced monthly premiums. For example, a family of four earning up to $106,000 annually may qualify for premium tax credits, making insurance more attainable for middle-class households.

One of the ACA’s most impactful provisions in California has been the expansion of Medicaid, known as Medi-Cal in the state. Prior to the ACA, Medicaid eligibility was strictly limited, leaving many low-income adults without coverage. The expansion extended eligibility to adults earning up to 138% of the federal poverty level, which in 2023 equates to roughly $20,120 for an individual. This change alone has enrolled over 5 million additional Californians in Medi-Cal, ensuring that vulnerable populations have access to essential healthcare services. However, challenges remain, such as provider shortages in rural areas, which can limit the practical benefits of expanded coverage.

Beyond enrollment numbers, the ACA has also improved the quality of health insurance in California by mandating essential health benefits, including preventive care, maternity care, and mental health services. Before the ACA, many plans excluded these services or charged exorbitant out-of-pocket fees. For instance, a 30-year-old woman in California can now access prenatal care without additional costs, a benefit that was previously unavailable in many plans. This shift has not only improved health outcomes but also reduced financial strain on individuals and families, as out-of-pocket maximums are now capped at $9,100 for individuals and $18,200 for families in 2023.

Critics of the ACA often point to rising premiums as a drawback, but it’s essential to contextualize these increases. While benchmark premiums in California have risen by an average of 5% annually since 2014, this rate is lower than pre-ACA trends. Moreover, subsidies have offset much of this growth for eligible enrollees. For example, in 2023, 90% of Covered California enrollees received financial assistance, with an average monthly premium of just $150 after subsidies. This underscores the ACA’s dual role in expanding coverage and making it financially feasible for millions of Californians.

Looking ahead, the ACA’s impact on California’s health insurance landscape will likely continue to evolve. Recent policy changes, such as the American Rescue Plan’s expansion of subsidies, have further reduced costs for enrollees. However, ongoing challenges, including healthcare affordability for those not eligible for subsidies and disparities in access to care, require sustained attention. By addressing these issues, California can build on the ACA’s successes and move closer to achieving universal healthcare coverage for its residents.

Annual Insurance Applications: Are They Necessary?

You may want to see also

Frequently asked questions

As of the most recent data, approximately 93% of Californians have health insurance, representing over 37 million people.

About 7% of California’s population, or roughly 2.7 million people, remain uninsured.

California’s insured rate has significantly increased over the past decade, largely due to the implementation of the Affordable Care Act (ACA) and the expansion of Medi-Cal.

The primary sources of health insurance in California are employer-based coverage, Medi-Cal (Medicaid), Covered California (the state’s ACA marketplace), and Medicare.