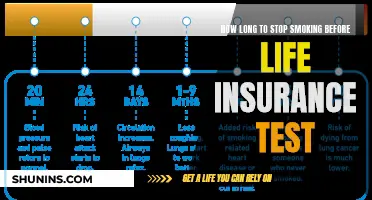

Life insurance is an important financial tool that provides peace of mind and financial security to millions of Americans. However, despite its benefits, a significant number of Americans do not have adequate coverage or any coverage at all. In fact, according to recent studies, about 100 million Americans are uninsured or underinsured when it comes to life insurance. This gap between those who have life insurance and those who need it is significant and highlights the ongoing challenge of addressing misconceptions about cost and educating consumers about the value and potential affordability of life insurance policies.

Explore related products

$92.55 $111

What You'll Learn

- % of women are uninsured, compared to 38% of men

- People with lower incomes are less likely to have life insurance

- Baby boomers are more likely to have life insurance, Gen Z are the least likely

- % of single mothers have life insurance, despite 59% believing they need it

- % of Americans would suffer financially within a month of losing a wage earner

![]()

44% of women are uninsured, compared to 38% of men

A significant number of Americans are uninsured or underinsured when it comes to life insurance. This is particularly true for women, as 44% of women are uninsured, compared to 38% of men. This gender gap has persisted for over a decade, with women consistently trailing men in life insurance ownership since 2011.

Several factors contribute to the gender disparity in life insurance coverage. One reason is that women are less likely to feel knowledgeable about life insurance. Only 22% of women surveyed described themselves as "very" or "extremely" knowledgeable about life insurance, compared to 33% of men. This lack of knowledge may lead to a lack of understanding of the importance of life insurance and the options available to them.

Additionally, women may face higher costs for life insurance than men. Life insurance costs are determined by various factors, including gender, age, health status, and lifestyle choices. Women may pay higher premiums, especially if they have pre-existing health conditions or engage in risky behaviours.

Furthermore, women's lower income levels may also contribute to the gender gap in life insurance coverage. Women are more likely to work in lower-paying jobs and have lower incomes than men, making it challenging for them to afford life insurance premiums.

The consequences of this disparity can be significant. Uninsured women may have inadequate access to care, receive a lower standard of care, and experience poorer health outcomes. They are also less likely to utilise important preventive services, such as mammograms, Pap tests, and timely blood pressure checks.

To address this issue, efforts should be made to improve financial literacy among women, particularly regarding life insurance. Additionally, insurance providers should work towards offering more affordable coverage options and ensuring that their products meet the specific needs of women.

Group Life Insurance: Taxable Benefits and Their Implications

You may want to see also

Explore related products

![]()

People with lower incomes are less likely to have life insurance

Life insurance is a valuable financial planning tool that provides financial protection to the families of the insured. However, a significant number of Americans do not have adequate coverage, with over 100 million Americans either uninsured or underinsured. People in lower-income households are less likely to have the life insurance coverage they need. This is due to a variety of factors, including the cost of insurance, lack of awareness, and other financial priorities.

Income and Insurance Needs

According to the 2024 Insurance Barometer Study, 56% of individuals with a household income of less than $50,000 don't have or don't have enough life insurance coverage. This is the largest need gap across income brackets. As income increases, the percentage of individuals without adequate coverage decreases. For those with a household income between $50,000 and $149,000, 39% report not having enough coverage, while for those with a household income of $150,000 or more, the number drops to 28%. This data suggests that income is a significant factor in an individual's ability to obtain life insurance.

Cost as a Barrier

One of the main reasons people in lower-income households may not have life insurance is the cost. Life insurance is often seen as too expensive, with 42% of Americans reporting that they do not purchase it due to the high cost. This perception of cost as a barrier is even higher among lower-income individuals, with 47% of Gen Z and 44% of Millennials citing it as the top reason for not having life insurance. Additionally, many people overestimate the cost of life insurance, with 82% of Americans guessing the cost to be three times higher than it actually is. This misconception about cost may be preventing lower-income individuals from even considering life insurance as an option.

Other Financial Priorities

For those in lower-income households, other financial priorities may take precedence over life insurance. This is especially true if they are already struggling to make ends meet. The 2024 Insurance Barometer Study found that 20% of individuals without life insurance cited other financial priorities as the reason for not purchasing it. This may include essential expenses such as rent or groceries, as well as other types of insurance like health or car insurance.

Lack of Awareness

Another factor contributing to the lack of life insurance among lower-income individuals is a lack of awareness. Some people may not know about the different types of life insurance available, such as term life insurance or permanent life insurance, and how these options may fit within their budget. Additionally, they may not be aware of the potential benefits of life insurance, such as providing financial protection for their loved ones or supplementing their income.

In conclusion, people in lower-income households are less likely to have life insurance due to a combination of factors, including the cost of insurance, other financial priorities, and a lack of awareness about the potential benefits and options available. Addressing these issues through education and outreach could help increase access to life insurance for lower-income individuals and provide them with valuable financial protection.

Selling Life Insurance Over the Phone: Strategies for Success

You may want to see also

Explore related products

![]()

Baby boomers are more likely to have life insurance, Gen Z are the least likely

Life insurance is an important financial planning tool that provides financial protection to the insured's loved ones. However, a significant number of Americans do not have adequate coverage, with 100 million either lacking insurance or being underinsured.

Baby boomers, born between 1946 and 1964, are the generation with the highest rate of life insurance ownership. They have accumulated substantial wealth, benefiting from the US's emergence as a global economic superpower, and have a strong presence in the real estate market. As they approach retirement, baby boomers are less likely to perceive a need for additional coverage, with only 27% indicating a need for more insurance. Their high ownership rates are also attributed to their life stage, as they have likely gone through milestones such as marriage, childbirth, and home purchases, which trigger the purchase of life insurance. Additionally, they have a longer career history, enabling them to afford coverage more easily.

In contrast, Gen Z, born between 1997 and 2012, has the lowest ownership rates and the highest need gap. Nearly half of Gen Z (49%) reported needing life insurance, but they face barriers such as affordability and a lack of understanding of insurance products. Their lower ownership rates can be attributed to their younger age and the fact that they are just beginning to experience significant life milestones. As they grow older and accumulate more assets and responsibilities, their interest in and need for life insurance are expected to increase.

The generational gap in life insurance ownership can be partly explained by the different life stages and financial situations of baby boomers and Gen Z. Baby boomers, being older, have had more time to accumulate wealth and are more likely to have dependents and financial commitments. On the other hand, Gen Z is still relatively young and may not have the same level of financial responsibilities or understanding of insurance needs. However, as Gen Z ages and their financial concerns evolve, their interest in life insurance is likely to grow, narrowing the gap with baby boomers.

VA Life Insurance: Who is Automatically Covered?

You may want to see also

Explore related products

![]()

41% of single mothers have life insurance, despite 59% believing they need it

Single mothers are among the most vulnerable groups in the United States, with a high financial concern. Despite this, they are significantly less likely to have life insurance than the general population. Only 41% of single mothers have a life insurance policy, compared to 52% of American adults overall. This disparity is concerning, given the crucial role that life insurance can play in providing financial protection for dependents.

The low rate of life insurance coverage among single mothers may be due to a variety of factors, including a lack of knowledge about life insurance products, the perception of high costs, and other financial priorities. According to the data, 40% of Gen Z parents, which includes many single mothers, say they don't have life insurance because they don't know what type to buy or how much coverage they need. Additionally, single mothers may face challenges such as lower incomes and limited access to affordable insurance options.

However, it is encouraging to see that 59% of single mothers recognize the need for life insurance. This indicates a growing awareness of the importance of financial planning and security among this demographic. By obtaining life insurance, single mothers can help ensure that their children will be financially protected in the event of their death.

The insurance industry also has a role to play in addressing this gap. By developing more accessible and affordable life insurance options specifically tailored to the needs of single mothers, insurance providers can help improve coverage rates and provide much-needed financial security for this vulnerable group.

In the United States, life insurance is an important tool for financial planning and protection. However, a significant number of Americans do not have adequate coverage. According to recent studies, about 52% of Americans have a life insurance policy, while 30% of adults need life insurance but do not have it. This gap between those who have coverage and those who need it is significant, with about 100 million Americans being uninsured or underinsured.

The main barriers to obtaining life insurance are perceived high costs, other financial priorities, and a lack of understanding about the necessary coverage amount. Additionally, there are disparities in life insurance ownership based on income, gender, and race and ethnicity. Lower-income households, women, and racial and ethnic minorities are less likely to have adequate coverage.

The COVID-19 pandemic has also influenced Americans' views on life insurance, with many people recognizing the importance of financial preparedness and an increased interest in obtaining affordable coverage. The life insurance industry has responded to these changing dynamics, adapting to meet the evolving needs of consumers.

Life Insurance and Taxes: What's the Write-Off Story?

You may want to see also

Explore related products

![]()

30% of Americans would suffer financially within a month of losing a wage earner

Life insurance is an important financial planning tool, but a significant number of Americans do not feel like they have adequate coverage. In fact, 30% of Americans would suffer financially within a month of losing a wage earner. This is due to a variety of factors, including the high cost of insurance, other financial priorities, and uncertainty about the necessary coverage amount.

The annual Insurance Barometer Study, produced by LIMRA and Life Happens, provides valuable insights into the insurance market landscape. The study found that 30% of non-owners recognize the need for life insurance but have not purchased it, mainly due to perceived high costs. This is a persistent issue, as the proportion of respondents citing cost as a barrier has remained stable since 2022.

The study also revealed that 10% of policyholders feel they need more coverage, suggesting a significant opportunity for the industry to better serve existing customers. Overall, there is a significant gap between those who have life insurance and those who need it, emphasizing the need for education and addressing misconceptions about cost.

The issue of insufficient coverage is particularly acute for younger generations. Gen Z and millennials are more likely to own term life insurance and have a higher need for more coverage, with 49% and 47% respectively indicating they need more. This is partly due to a lack of knowledge about life insurance products, as over a quarter of these generations cite this as a barrier to ownership.

Single mothers also face a higher need for life insurance, as they are often the sole source of financial support for their children. Less than half (41%) of single mothers have life insurance, and 59% say they need coverage or more of it.

The impact of life insurance ownership is significant. 71% of insured parents would feel financially secure if a primary wage earner passed away, compared to only 48% of uninsured parents. This highlights the importance of life insurance in providing financial security for families.

In conclusion, while life insurance is a valuable tool, there are still many Americans who are underserved by the industry. Addressing the issues of cost, education, and coverage gaps is essential to ensuring that more people have the protection they need.

Does the FBI Offer Life Insurance Policies to Agents?

You may want to see also

Frequently asked questions

48% of Americans don't have life insurance.

Over 100 million Americans are uninsured or underinsured.

The average cost of a $250,000, 20-year term life insurance policy for a healthy 30-year-old is $152 per year.

The primary use of life insurance is to provide financial protection to those who rely on the insured for financial support.

The common reasons for not having life insurance are the perceived high costs, other financial priorities, and uncertainty about the necessary coverage amount.