Health insurance coverage is a critical aspect of the American healthcare system, providing individuals and families with access to essential medical services while mitigating financial risks associated with illness or injury. As of recent data, approximately 91% of Americans have some form of health insurance, a significant increase from previous decades due to policy reforms like the Affordable Care Act (ACA). Coverage is primarily obtained through employer-sponsored plans, government programs such as Medicaid and Medicare, or individual marketplace plans. Despite this high coverage rate, disparities persist, with gaps among low-income populations, certain racial and ethnic groups, and individuals in states that have not expanded Medicaid. Understanding the scope and limitations of health insurance coverage in the U.S. is essential for addressing ongoing challenges in healthcare accessibility and equity.

Explore related products

What You'll Learn

- Employer-Sponsored Coverage: Majority of Americans get health insurance through their employers, a common practice

- Government Programs: Medicaid, Medicare, and CHIP provide coverage for eligible low-income and elderly individuals

- Individual Market: Some purchase plans directly from insurers or through Affordable Care Act marketplaces

- Uninsured Rates: Despite coverage options, millions remain uninsured due to cost or eligibility issues

- Coverage Trends: Health insurance rates fluctuate based on policy changes, economic conditions, and healthcare reforms

![]()

Employer-Sponsored Coverage: Majority of Americans get health insurance through their employers, a common practice

In 2022, approximately 155 million Americans—nearly half the population—relied on employer-sponsored health insurance as their primary coverage. This statistic underscores a deeply ingrained system where workplaces act as the gateway to healthcare access. For most employees, this arrangement offers a cost-effective solution: employers cover an average of 83% of premiums for single coverage and 73% for family plans, significantly reducing out-of-pocket expenses. However, this model ties health security to employment, leaving workers vulnerable during job transitions or layoffs.

Consider the mechanics: employer-sponsored plans typically include a mix of HMOs, PPOs, and high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs). Employees often contribute a portion of the premium through payroll deductions, with the employer subsidizing the remainder. For instance, a single employee might pay $100 monthly for a plan costing $600, while the employer covers the $500 difference. This shared-cost structure makes coverage more affordable than individual market plans, which can cost upwards of $400 monthly for comparable benefits.

The system’s prevalence has historical roots in World War II wage controls, when employers began offering health benefits to attract workers. Today, it remains a cornerstone of the U.S. healthcare landscape, with 96% of firms with 100+ employees providing coverage, compared to 50% of small businesses (1–49 employees). However, this disparity highlights a critical gap: workers in smaller firms, part-time roles, or gig economy jobs often lack access, contributing to the 8.5% uninsured rate in 2022.

For those with employer-sponsored insurance, maximizing benefits requires proactive engagement. Review plan details annually during open enrollment, focusing on network providers, prescription drug coverage, and preventive care services, which are often fully covered under the Affordable Care Act. If offered an HDHP, contribute to an HSA to save pre-tax dollars for medical expenses, with 2023 contribution limits at $3,850 for individuals and $7,750 for families. Finally, understand COBRA or state continuation options if you leave your job, though premiums rise sharply without employer subsidies.

Despite its dominance, employer-sponsored coverage is not without flaws. It limits portability, discourages entrepreneurship, and excludes dependents or spouses with better options elsewhere. Policymakers and advocates increasingly debate alternatives, such as expanding Medicare or creating a public option. Yet, for now, this system remains the backbone of American healthcare, blending affordability with accessibility—though not without trade-offs for millions navigating its complexities.

Does Birth Control Impact Insurance Costs? Exploring the Connection

You may want to see also

Explore related products

![]()

Government Programs: Medicaid, Medicare, and CHIP provide coverage for eligible low-income and elderly individuals

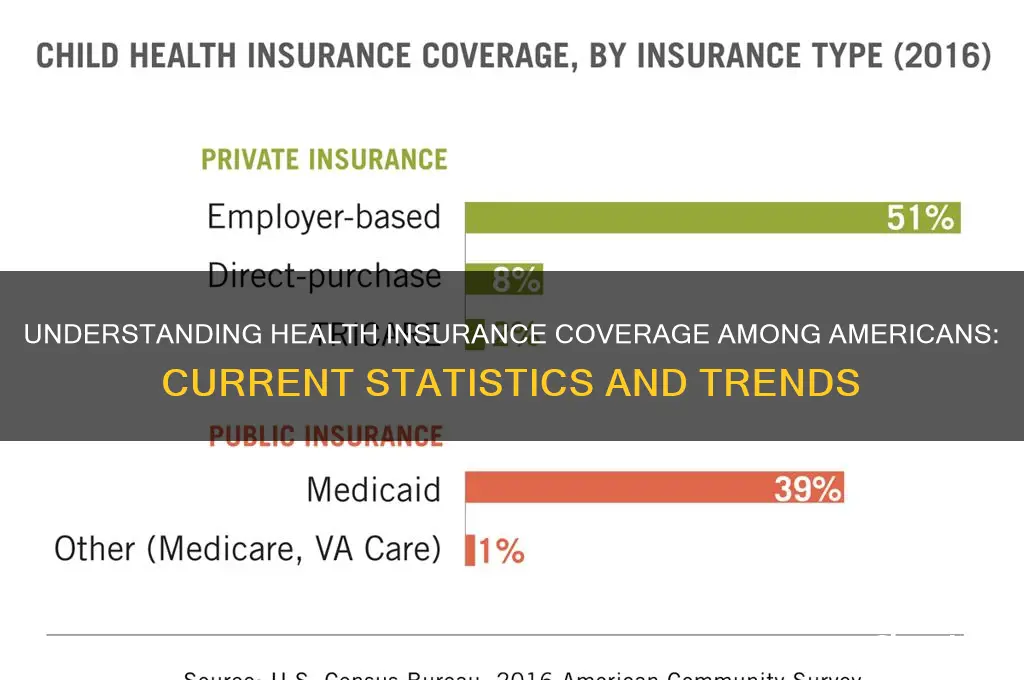

In 2022, approximately 92% of Americans had health insurance, a figure that reflects the combined efforts of private insurers and government programs. Among these, Medicaid, Medicare, and the Children’s Health Insurance Program (CHIP) play a critical role in covering vulnerable populations. Together, these programs insure over 130 million people, or roughly 40% of the insured population, ensuring that low-income families, children, pregnant women, and the elderly have access to essential healthcare services.

Medicaid, the largest of these programs, serves as a safety net for over 80 million Americans, including low-income adults, children, pregnant women, and individuals with disabilities. Eligibility criteria vary by state but generally target households earning up to 138% of the federal poverty level (FPL). For example, a family of four in 2023 could qualify with an annual income of $38,295 or less. Medicaid covers a broad range of services, from preventive care to long-term care, and has been instrumental in reducing disparities in healthcare access since its expansion under the Affordable Care Act.

Medicare, on the other hand, is designed for individuals aged 65 and older, as well as younger people with certain disabilities or end-stage renal disease. With over 65 million beneficiaries, Medicare is divided into parts: Part A (hospital insurance), Part B (medical insurance), and Part D (prescription drug coverage). While Part A is typically premium-free for those who paid Medicare taxes, Part B requires a monthly premium, averaging $164.90 in 2023. Medicare Advantage plans, offered by private insurers, provide an alternative to traditional Medicare, often including additional benefits like vision and dental care.

CHIP bridges the gap for children in families who earn too much to qualify for Medicaid but cannot afford private insurance. Covering approximately 9 million children, CHIP ensures access to pediatric care, immunizations, and dental services. Eligibility thresholds vary, but most states cover children in families earning up to 200% of the FPL. For instance, a family of three in 2023 could qualify with an annual income of up to $48,000. CHIP’s success lies in its ability to reduce the uninsured rate among children to historic lows, currently below 5%.

While these programs are effective, challenges remain. Medicaid’s state-based structure leads to inconsistencies in coverage and eligibility, leaving some low-income individuals in a "coverage gap" in states that did not expand the program. Medicare faces long-term financial sustainability concerns due to rising healthcare costs and an aging population. CHIP, though successful, requires periodic reauthorization, creating uncertainty for families and providers. Addressing these issues through policy reforms, such as standardizing Medicaid eligibility or strengthening Medicare’s funding mechanisms, could further enhance the impact of these programs.

In practice, understanding these programs is key to maximizing their benefits. For instance, Medicare beneficiaries can reduce out-of-pocket costs by enrolling in Part D during their initial eligibility period to avoid late penalties. Medicaid enrollees should stay informed about their state’s renewal processes to avoid coverage lapses. Parents applying for CHIP can use online tools like the Healthcare.gov screener to determine eligibility quickly. By leveraging these programs effectively, millions of Americans can secure the healthcare they need, contributing to a healthier, more equitable society.

Does DoorDash Raise Insurance Rates? What Drivers Need to Know

You may want to see also

Explore related products

![]()

Individual Market: Some purchase plans directly from insurers or through Affordable Care Act marketplaces

In the individual health insurance market, millions of Americans bypass employer-sponsored plans, opting instead to purchase coverage directly from insurers or through the Affordable Care Act (ACA) marketplaces. This route offers flexibility but requires careful navigation of plan options, costs, and enrollment periods. For those ineligible for employer-sponsored insurance or government programs like Medicaid, this market is often the primary pathway to securing health coverage.

Consider the enrollment process, which demands attention to detail. Open enrollment for ACA marketplace plans typically runs from November 1 to January 15, though qualifying life events (e.g., marriage, job loss) may trigger a special enrollment period. When purchasing directly from insurers, availability varies by state, and plans may not adhere to ACA regulations, such as covering pre-existing conditions. For instance, a 35-year-old in Texas might find a non-ACA plan with lower premiums but higher out-of-pocket costs, while a similar plan on the marketplace could offer subsidies reducing monthly payments to under $100.

A critical factor is understanding plan tiers—Bronze, Silver, Gold, and Platinum—which dictate cost-sharing. Silver plans, for example, cover roughly 70% of healthcare costs, making them a middle-ground option. However, pairing a Silver plan with Cost-Sharing Reduction (CSR) subsidies can significantly lower deductibles and copays for individuals earning up to 250% of the federal poverty level. This strategy is particularly beneficial for those with chronic conditions requiring frequent care.

One practical tip: use the ACA marketplace’s “window-shopping” feature to compare plans before creating an account. Input your estimated income and household size to see if you qualify for premium tax credits or CSR subsidies. For direct purchases, consult an independent broker who can access plans from multiple insurers, ensuring you’re not missing better-priced options.

Finally, beware of short-term health plans marketed as affordable alternatives. While premiums may be lower, these plans often exclude essential health benefits like maternity care or prescription drugs and can deny coverage for pre-existing conditions. For long-term security, prioritize ACA-compliant plans, especially if you have ongoing health needs or anticipate significant medical expenses. This approach balances cost and comprehensive coverage, ensuring you’re protected without overpaying.

Does Nationwide Offer Motorcycle Insurance? Coverage Options Explained

You may want to see also

Explore related products

![]()

Uninsured Rates: Despite coverage options, millions remain uninsured due to cost or eligibility issues

In 2022, approximately 8% of Americans, or about 26 million people, lacked health insurance, according to the U.S. Census Bureau. This statistic is particularly striking given the existence of programs like Medicaid, the Affordable Care Act (ACA) marketplaces, and employer-sponsored plans. While these options have significantly reduced uninsured rates since the ACA’s implementation in 2010, millions remain uncovered, often due to financial barriers or eligibility gaps. For instance, in states that have not expanded Medicaid, many low-income adults fall into the "coverage gap," earning too much to qualify for Medicaid but too little to afford private insurance. This highlights a systemic issue: even when coverage options exist, they are not universally accessible.

Consider the case of a 35-year-old in Texas, a non-expansion state, earning $15,000 annually. This income is above the Medicaid eligibility threshold but below the level required to receive ACA premium subsidies. Without employer-sponsored insurance, this individual faces premiums that can consume 20–30% of their income, making coverage unaffordable. Such scenarios underscore the limitations of current policies, which often fail to address the needs of those in the lowest income brackets. Even for those with slightly higher incomes, high deductibles and out-of-pocket costs can render insurance functionally useless, leading many to forgo coverage altogether.

To address these gaps, policymakers could explore targeted solutions. For example, expanding Medicaid in the 10 remaining non-expansion states would cover an estimated 2.2 million uninsured adults. Additionally, capping ACA marketplace premiums at a lower percentage of income—say, 5% for those earning below 200% of the federal poverty level—could make coverage more affordable. Employers could also play a role by offering more robust health benefits or contributing to individual market premiums for low-wage workers. These steps, while not exhaustive, would directly tackle the cost and eligibility barriers that persist.

A comparative analysis reveals that countries with universal healthcare systems, such as Canada or the UK, have uninsured rates near zero, demonstrating that systemic design can eliminate coverage gaps. While the U.S. operates on a mixed model, lessons from these systems suggest that incremental reforms, like automatic enrollment in affordable plans or simplifying eligibility criteria, could significantly reduce uninsured rates. For individuals navigating this landscape, practical tips include exploring state-specific programs, using ACA open enrollment periods to reassess options, and leveraging nonprofit organizations that offer enrollment assistance. Ultimately, the persistence of uninsured rates is not a lack of options but a failure to ensure those options are truly within reach.

Life Insurance Renewal: Late Fee Explained

You may want to see also

Explore related products

![]()

Coverage Trends: Health insurance rates fluctuate based on policy changes, economic conditions, and healthcare reforms

Health insurance coverage in the United States is not static; it ebbs and flows in response to a complex interplay of policy shifts, economic tides, and healthcare reforms. For instance, the Affordable Care Act (ACA) of 2010 expanded coverage to millions by introducing marketplaces, subsidies, and Medicaid expansion. By 2016, the uninsured rate dropped to a historic low of 8.6%. However, subsequent policy changes, such as the elimination of the individual mandate penalty in 2019, led to a slight uptick in uninsured rates, reaching 9.2% by 2020. This example underscores how legislative actions directly influence coverage trends, often with immediate and measurable impacts.

Economic conditions also play a pivotal role in shaping health insurance rates. During the 2008 recession, for example, employer-sponsored insurance—the primary coverage source for most Americans—declined as job losses soared. The uninsured rate climbed from 14.4% in 2008 to 16.3% in 2010. Conversely, economic recovery post-2010, coupled with ACA implementation, reversed this trend. Today, as inflation and rising healthcare costs strain household budgets, many individuals are opting for lower-cost plans or forgoing insurance altogether. This highlights the delicate balance between economic stability and access to affordable coverage.

Healthcare reforms, beyond federal legislation, also drive fluctuations in insurance rates. State-level decisions, such as whether to expand Medicaid, have significant localized impacts. As of 2023, 40 states and the District of Columbia have adopted Medicaid expansion, covering millions of low-income adults. States like Texas and Florida, which have not expanded Medicaid, continue to see higher uninsured rates, particularly among adults aged 19–64. These disparities illustrate how regional policy choices can either bridge or widen coverage gaps, even within the same national framework.

To navigate these fluctuating trends, individuals and families should stay informed about policy changes and economic indicators that may affect their coverage options. Practical steps include regularly reviewing employer-sponsored plans during open enrollment, exploring ACA marketplace subsidies if income qualifies, and understanding state-specific Medicaid eligibility criteria. For those nearing age 65, enrolling in Medicare during the initial enrollment period is critical to avoid penalties. Additionally, leveraging health savings accounts (HSAs) can provide financial relief for out-of-pocket costs, especially during uncertain economic times.

In conclusion, health insurance coverage trends are a dynamic reflection of broader systemic forces. By understanding the interplay of policy changes, economic conditions, and healthcare reforms, individuals can make informed decisions to maintain or secure coverage. While fluctuations are inevitable, proactive awareness and strategic planning can mitigate their impact, ensuring continued access to essential healthcare services.

Does PIP Raise Your Insurance? Understanding the Impact on Premiums

You may want to see also

Frequently asked questions

As of the latest data, approximately 91% of Americans have health insurance, covering around 300 million people.

About 9% of Americans, or roughly 30 million people, are uninsured, according to recent statistics.

Elderly Americans aged 65 and older have the highest health insurance coverage rate, primarily due to Medicare, with nearly 100% coverage.

The ACA significantly reduced the uninsured rate, increasing coverage by expanding Medicaid and creating health insurance marketplaces, resulting in millions more Americans gaining insurance since its implementation.