The Affordable Care Act (ACA), commonly known as Obamacare, has significantly expanded health insurance coverage in the United States since its implementation in 2010. By introducing key provisions such as Medicaid expansion, health insurance marketplaces, and subsidies for low- and middle-income individuals, the ACA has enabled millions of previously uninsured Americans to gain access to affordable coverage. As of recent data, an estimated 20 million people have obtained insurance due to the ACA, reducing the uninsured rate to historic lows. This expansion has not only improved access to healthcare but also addressed disparities in coverage, particularly among low-income, minority, and young adult populations. However, challenges remain, including political debates over the ACA's future and varying state-level adoption of Medicaid expansion, which continue to influence the number of insured individuals nationwide.

Explore related products

What You'll Learn

- Increase in Coverage Rates: ACA's impact on reducing uninsured rates across demographics and states

- Medicaid Expansion Effects: How expanded Medicaid under ACA boosted insurance access in participating states

- Individual Mandate Role: The mandate's influence on encouraging enrollment in health insurance plans

- Marketplace Enrollment Trends: Growth in insurance sign-ups through ACA's health insurance marketplaces

- Demographic Shifts: Changes in insured rates among young adults, low-income, and minority groups post-ACA

![]()

Increase in Coverage Rates: ACA's impact on reducing uninsured rates across demographics and states

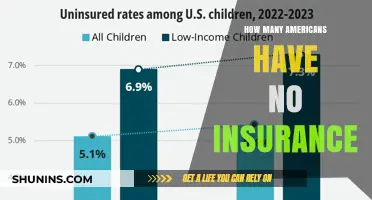

The Affordable Care Act (ACA) has significantly reshaped the American healthcare landscape, particularly in its mission to reduce the number of uninsured individuals. Since its implementation, the ACA has led to a notable increase in coverage rates, benefiting diverse demographics and states. One of the most striking examples is the national uninsured rate, which dropped from 16% in 2010 to 8.6% in 2016, according to the Centers for Disease Control and Prevention (CDC). This reduction is not uniform, however, as certain groups and regions have experienced more pronounced gains.

Analyzing demographic trends reveals the ACA’s targeted impact. Young adults aged 19–25 saw one of the earliest and most dramatic increases in coverage due to the provision allowing them to remain on their parents’ insurance plans. Coverage rates for this age group rose from 67% in 2010 to 82% in 2016. Similarly, low-income individuals have benefited significantly, with Medicaid expansion states witnessing a 25% reduction in uninsured rates among adults with incomes below 138% of the federal poverty level. Non-elderly Black and Hispanic individuals also experienced substantial gains, with uninsured rates dropping by 10 and 12 percentage points, respectively, between 2013 and 2016.

Geographically, the ACA’s impact varies widely, underscoring the importance of state-level decisions regarding Medicaid expansion. States that expanded Medicaid saw uninsured rates fall by an average of 10 percentage points, compared to just 5 percentage points in non-expansion states. For instance, Kentucky, which embraced expansion, reduced its uninsured rate from 14.3% in 2013 to 5.8% in 2016. In contrast, Texas, which opted out, saw a much smaller decline, from 22.1% to 16.6% during the same period. This disparity highlights the critical role of state policies in maximizing the ACA’s potential.

To sustain and build upon these gains, policymakers and advocates must address remaining gaps. For example, states that have not yet expanded Medicaid could reconsider their stance to extend coverage to millions of low-income residents. Additionally, outreach efforts should focus on underserved communities, such as rural areas and non-English speakers, who may face barriers to enrollment. Practical steps include simplifying application processes, increasing funding for navigators, and leveraging community organizations to educate eligible individuals about available options.

In conclusion, the ACA’s impact on reducing uninsured rates is undeniable, but its success is neither uniform nor complete. By examining demographic and geographic trends, stakeholders can identify areas for improvement and implement targeted strategies to ensure broader access to healthcare. The ACA’s legacy lies not just in the numbers, but in its potential to transform lives through equitable coverage.

Family History: Life Insurance Impact

You may want to see also

Explore related products

![]()

Medicaid Expansion Effects: How expanded Medicaid under ACA boosted insurance access in participating states

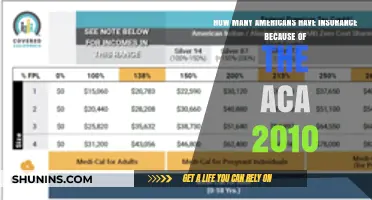

The Affordable Care Act's (ACA) Medicaid expansion has been a game-changer for millions of low-income Americans, particularly in states that opted to expand their programs. As of 2023, 38 states and the District of Columbia have implemented Medicaid expansion, providing coverage to individuals with incomes up to 138% of the federal poverty level (FPL). This threshold translates to an annual income of approximately $18,754 for a single individual, making it a crucial safety net for those who previously fell into the "coverage gap" – earning too much for traditional Medicaid but not enough to afford private insurance.

Consider the impact in Kentucky, one of the earliest expansion states. Between 2013 and 2015, the state's uninsured rate plummeted from 14.3% to 5.8%, with over 400,000 residents gaining coverage through the expanded Medicaid program. This dramatic increase in insurance access has had a ripple effect, improving not only individual health outcomes but also the financial stability of healthcare providers, particularly in rural areas. Hospitals in expansion states have reported significant reductions in uncompensated care costs, with some studies estimating savings of up to $6.2 billion annually.

However, the benefits of Medicaid expansion extend far beyond the healthcare sector. A 2021 study published in the Journal of Health Economics found that expansion states experienced a 6.5% reduction in mortality rates among low-income adults aged 55-64, compared to non-expansion states. This age group, often referred to as the "near-elderly," is particularly vulnerable to health disparities, as they are not yet eligible for Medicare but may face age-related health challenges. By providing access to preventive care and chronic disease management, expanded Medicaid has become a vital tool in addressing these disparities.

To maximize the impact of Medicaid expansion, states should consider implementing targeted outreach and enrollment strategies. For instance, partnering with community-based organizations can help reach underserved populations, such as non-English speakers or individuals with limited health literacy. Additionally, streamlining the enrollment process through online platforms and same-day coverage options can reduce barriers to access. States like California and New York have successfully utilized these approaches, achieving uninsured rates below 5% among eligible low-income residents. As more states consider expanding their Medicaid programs, these best practices can serve as a roadmap for ensuring that the ACA's promise of accessible, affordable healthcare becomes a reality for all.

Ultimately, the success of Medicaid expansion under the ACA highlights the importance of state-level policy decisions in shaping healthcare access. By embracing expansion, states not only improve the health and well-being of their residents but also contribute to a more equitable and sustainable healthcare system. As the debate over healthcare reform continues, the evidence from expansion states provides a compelling case for prioritizing policies that prioritize coverage and accessibility, particularly for the most vulnerable populations.

Pregnant and Want Life Insurance? It's Possible

You may want to see also

Explore related products

![]()

Individual Mandate Role: The mandate's influence on encouraging enrollment in health insurance plans

The Affordable Care Act's (ACA) individual mandate, a cornerstone of the legislation, requires most Americans to have health insurance or pay a penalty. This provision has been instrumental in shaping the health insurance landscape, particularly in encouraging enrollment among previously uninsured individuals. By introducing this mandate, the ACA aimed to address the issue of adverse selection, where only those with higher health risks or immediate medical needs would seek coverage, potentially destabilizing the insurance market.

The Mechanism of Encouragement

The individual mandate operates as a nudge, leveraging the power of financial incentives to motivate compliance. Initially, the penalty for non-compliance was structured as a percentage of income or a flat fee, whichever was higher. For instance, in 2014, the penalty started at $95 per adult and $47.50 per child, up to a maximum of $285 per family, or 1% of family income above the tax return filing threshold. This financial consequence was designed to make purchasing insurance a more attractive option than paying the penalty, especially for younger, healthier individuals who might otherwise forgo coverage.

Impact on Enrollment Trends

Analyzing enrollment data reveals the mandate's effectiveness. In the first year of ACA implementation, approximately 8 million individuals signed up for health insurance through the marketplaces, with an additional 4.8 million young adults gaining coverage under their parents' plans. This surge in enrollment can be partly attributed to the individual mandate, which created a sense of urgency and highlighted the potential financial repercussions of remaining uninsured. Studies suggest that the mandate's influence was particularly pronounced among low-income individuals and those with pre-existing conditions, who stood to benefit the most from the ACA's protections and subsidies.

A Comparative Perspective

To understand the mandate's role better, consider the contrast with states that expanded Medicaid under the ACA. While Medicaid expansion provided a direct pathway to coverage for low-income individuals, the individual mandate targeted a broader population, including those with incomes above Medicaid eligibility thresholds. This dual approach ensured that the ACA's impact on insurance rates was not limited to a specific demographic but rather created a more comprehensive shift towards universal coverage. For example, in states that embraced both Medicaid expansion and actively promoted the individual mandate, uninsured rates dropped significantly, often reaching single-digit percentages.

Practical Considerations and Takeaways

The individual mandate's success in encouraging enrollment highlights the importance of policy design in achieving public health goals. However, it's crucial to acknowledge that the mandate's effectiveness may vary across different population segments. Younger adults, for instance, might require additional incentives or education to appreciate the long-term benefits of health insurance. Furthermore, the mandate's impact should be continually assessed and adjusted to account for changing economic conditions and healthcare needs. As the ACA evolves, policymakers must consider refining the mandate to ensure it remains a relevant and effective tool in promoting health insurance enrollment, ultimately contributing to a healthier, more insured population.

Mastering Windstorm Insurance: Smart Shopping Tips for Homeowners

You may want to see also

Explore related products

![]()

Marketplace Enrollment Trends: Growth in insurance sign-ups through ACA's health insurance marketplaces

Since the Affordable Care Act (ACA) established health insurance marketplaces, enrollment trends have revealed a steady and, at times, remarkable growth in sign-ups. The 2023 open enrollment period saw a record-breaking 16.3 million people select plans through Healthcare.gov and state-based marketplaces, a 13% increase from the previous year. This surge in enrollment defied predictions of stagnation, highlighting the enduring demand for affordable, comprehensive coverage.

Analyzing the Drivers of Growth

Several factors contribute to this upward trend. Firstly, the ACA's subsidies, which are income-based and designed to reduce premium costs, have become increasingly effective in making coverage accessible. For instance, during the 2023 enrollment period, 89% of enrollees received subsidies, with an average monthly premium reduction of $533. Secondly, the ACA's expansion of Medicaid in many states has created a ripple effect, raising awareness about the availability of affordable health insurance options and encouraging previously uninsured individuals to explore their coverage possibilities.

A Comparative Perspective: State-Based Marketplaces vs. Healthcare.gov

State-based marketplaces have consistently outperformed Healthcare.gov in terms of enrollment growth. States like California and New York, which operate their own exchanges, have implemented innovative outreach strategies, such as targeted marketing campaigns and in-person assistance, to drive sign-ups. In contrast, Healthcare.gov, which serves 33 states, has relied heavily on digital platforms and partnerships with community organizations. However, the recent growth in Healthcare.gov enrollment suggests that these efforts are gaining traction, particularly among younger, healthier individuals who may have previously opted out of coverage.

Practical Tips for Maximizing Enrollment Opportunities

To capitalize on the growing trend of marketplace enrollment, individuals should:

- Assess their eligibility for subsidies: Use the ACA's subsidy calculator to estimate potential premium reductions based on income and household size.

- Compare plans carefully: Evaluate not only premiums but also out-of-pocket costs, provider networks, and prescription drug coverage.

- Seek assistance if needed: Utilize free resources like navigators, brokers, or community health centers to help navigate the enrollment process and identify the best plan for their needs.

The Takeaway: A Bright Future for ACA Marketplace Enrollment

The growth in insurance sign-ups through ACA marketplaces is a testament to the act's enduring impact on expanding access to affordable healthcare. As enrollment continues to rise, it is essential to maintain and build upon the policies and strategies that have driven this success. By addressing remaining barriers to coverage, such as awareness gaps and affordability concerns, policymakers and stakeholders can ensure that the ACA's promise of accessible, comprehensive health insurance is realized for an even greater number of Americans.

Life Insurance Brokers: Where to Find Informative Resources

You may want to see also

Explore related products

![]()

Demographic Shifts: Changes in insured rates among young adults, low-income, and minority groups post-ACA

The Affordable Care Act (ACA) has significantly reshaped the American healthcare landscape, particularly for young adults, low-income individuals, and minority groups. One of the most notable impacts has been the expansion of health insurance coverage, but the changes haven’t been uniform across demographics. Young adults, aged 18 to 34, have seen a substantial increase in insured rates, largely due to provisions like the ability to stay on parental plans until age 26 and the availability of subsidized marketplace plans. This age group, historically less likely to have employer-sponsored insurance, benefited from the ACA’s focus on affordability and accessibility. For instance, the uninsured rate among young adults dropped from 29% in 2010 to 13% by 2020, a testament to the policy’s targeted effectiveness.

Low-income individuals have also experienced dramatic shifts in insured rates, particularly in states that expanded Medicaid under the ACA. In expansion states, the uninsured rate among low-income adults (those earning below 138% of the federal poverty level) fell by nearly 50%, compared to modest declines in non-expansion states. This disparity highlights the critical role of state-level decisions in amplifying the ACA’s impact. However, gaps remain, especially in states that opted out of Medicaid expansion, where millions of low-income individuals still lack coverage. Practical steps to address this include advocating for state-level policy changes and leveraging community health centers that offer sliding-scale fees for uninsured patients.

Minority groups, including Hispanic, Black, and Native American populations, have seen mixed but generally positive trends in insured rates post-ACA. For example, the uninsured rate among Hispanics dropped from 32% in 2013 to 19% in 2019, while Black Americans saw a decline from 21% to 11% during the same period. These improvements are partly due to Medicaid expansion and outreach efforts targeting underserved communities. However, disparities persist, with minority groups often facing barriers like language, cultural stigma, and limited access to healthcare providers. To bridge these gaps, culturally tailored outreach programs and increased funding for community health workers have proven effective in states like California and New York.

A comparative analysis reveals that while the ACA has made strides in reducing uninsured rates across these demographics, systemic challenges remain. Young adults, for instance, still face higher premiums relative to older age groups, which can deter enrollment. Low-income individuals in non-expansion states are caught in a coverage gap, ineligible for both Medicaid and marketplace subsidies. Minority groups continue to grapple with historical inequities that the ACA alone cannot fully address. Addressing these issues requires a multi-faceted approach, including policy reforms, targeted interventions, and sustained investment in healthcare infrastructure.

In conclusion, the ACA has undeniably transformed insured rates among young adults, low-income individuals, and minority groups, but its success is uneven. Policymakers, healthcare providers, and advocates must focus on closing remaining gaps by addressing affordability, accessibility, and equity. Practical steps include expanding Medicaid in holdout states, increasing subsidies for young adults, and implementing culturally competent outreach strategies for minority communities. By doing so, the promise of universal healthcare can move closer to reality, ensuring that no demographic is left behind.

Does the Oppressor MK2 Include Insurance Coverage? Find Out Here

You may want to see also

Frequently asked questions

As of 2023, the ACA has helped over 20 million previously uninsured Americans gain health coverage through expanded Medicaid, the Health Insurance Marketplace, and other provisions.

The ACA reduced the uninsured rate from approximately 16% in 2010 to around 8% in recent years, with millions benefiting directly from its provisions.

Over 15 million people have gained Medicaid coverage in states that expanded the program under the ACA, significantly reducing uninsured rates in those states.

As of 2023, more than 16 million people have enrolled in health insurance plans through the ACA Marketplace, with many receiving subsidies to make coverage affordable.