Health insurance is a significant incentive for employees, helping businesses to attract and retain workers. In the US, around 78% of the population is eligible for health insurance through their employers. However, the percentage of employees with access to employer-sponsored health insurance varies across states, with a 3-year average low of 70.5% in Wyoming and a high of 97.5% in Hawaii. Small businesses with between one and 50 employees can qualify for group health insurance, which is often more affordable than individual plans. To be eligible for group coverage, businesses must have at least one full-time employee working a minimum of 30 hours per week, and at least 70% of their uninsured, full-time employees must be enrolled.

| Characteristics | Values |

|---|---|

| Number of U.S. private-sector employees with employer-sponsored health insurance | 86% (2020-2022 average) |

| States with highest and lowest percentage of private-sector employees with employer-sponsored health insurance | Hawaii (97.5%), Wyoming (70.5%) |

| States with above-average employer-sponsored health insurance | Alabama, Hawaii, Illinois, Massachusetts, New York, Pennsylvania, Virginia, and the District of Columbia |

| Number of outpatient care centers in the U.S. | 54,642 |

| Number of paid employees in outpatient care centers in the U.S. | 1,225,333 |

| Annual payroll of outpatient care centers in the U.S. | $84.1 billion |

| Percentage of U.S. population eligible for employer-sponsored health insurance | 78% (as of 2022) |

| Most common type of employer-sponsored health insurance | Preferred Provider Organization (PPO) plans |

| Percentage of firms offering PPO plans | 47% (2023) |

| Second most common type of employer-sponsored health insurance | High Deductible Health Plans with Savings Options (HDHP/SO) |

| Percentage of firms offering HDHP/SO plans | 29% (2023) |

| Minimum number of employees for small business health insurance | 1-50 employees |

| Minimum number of employees for QSEHRA | <50 full-time equivalent employees |

| Minimum number of employees for ICHRA | No minimum |

| Percentage of medical premiums paid by employers for single coverage plans | 78% |

| Percentage of medical premiums paid by employees for single coverage plans | 22% |

Explore related products

What You'll Learn

- Small businesses with 1-50 employees can qualify for group health insurance

- Group health insurance is often cheaper than individual plans

- % of private industry workers had access to medical benefits in March 2022

- Employers can reimburse employees tax-free for medical expenses

- Health insurance coverage is a significant recruitment incentive

![]()

Small businesses with 1-50 employees can qualify for group health insurance

There are several benefits to small businesses offering group health insurance. It can be less expensive than individual plans with the same benefits and coverage options. It can also make a business more attractive to potential hires and help retain current employees. Additionally, businesses often qualify for tax advantages when providing group health insurance.

There are some challenges to consider when offering group health insurance. It can be expensive, particularly for very small businesses. There may also be challenges in meeting minimum participation rates required by insurance providers. Managing a group health insurance plan can be time-consuming and complex.

If a small business is concerned about meeting minimum participation rates, there is a window of time when this requirement is waived. If a business enrolls in small business group health insurance from November 15 to December 15, the 70% participation rule does not apply. This means a business can be approved with fewer than 70% of eligible full-time employees enrolled.

Medicaid and Life Insurance Trust Funds: What's the Deal?

You may want to see also

Explore related products

![]()

Group health insurance is often cheaper than individual plans

Additionally, group health insurance can help employers save on administration time when employees purchase and manage their own plans. Employers can also leverage HRAs (Health Reimbursement Arrangements) to help their workers save on their medical expenses. HRAs allow employers to reimburse their employees tax-free for qualifying out-of-pocket costs and, sometimes, individual health insurance premiums.

The Affordable Care Act (ACA) mandates that employers with 50 or more full-time employees, and/or full-time equivalents (FTEs), must offer affordable health insurance that provides minimum value to 95% of their full-time employees and their children up to the age of 26. However, the ACA does not require small businesses to offer health insurance to their employees. A small business is defined as having between one and 50 employees.

Small businesses that wish to provide health insurance to their employees can benefit from group health insurance plans. Group coverage HRAs can help offset the high deductibles that come with high-deductible health plans (HDHPs) by covering co-insurance or deductible expenses, along with other allowable expenses. Additionally, with a QSEHRA, small businesses with fewer than 50 FTEs who don't have a group health plan can reimburse employees for their monthly premium and other eligible out-of-pocket costs.

Medical Insurance: Home Health Aides After Hospitalization?

You may want to see also

Explore related products

![]()

70% of private industry workers had access to medical benefits in March 2022

In the United States, healthcare coverage is a significant incentive for workers when considering job opportunities. While health insurance coverage is a benefit for employees, it is also beneficial to businesses as it helps them to recruit and retain workers.

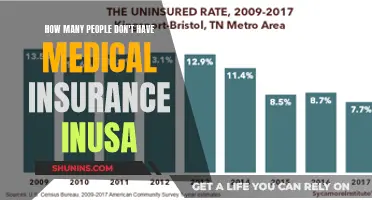

In March 2022, 70% of private industry workers had access to medical benefits. This was an increase from 2017, when 58% of private industry workers had access to medical care. A further breakdown of the 2022 data shows that 47% of workers participated in a medical care plan offered by their employer, resulting in a 66% take-up rate. The take-up rate is the percentage of workers with access to an employer-sponsored benefit who choose to participate in the benefit.

The availability of medical benefits varies across the private sector in different states. While the national average is 86%, according to a 3-year average based on 2020-2022 data, the percentage of private-sector employees with access to health insurance ranged from a low of 70.5% in Wyoming to a high of 97.5% in Hawaii. Notably, seven states and the District of Columbia offer health insurance to employees at a rate significantly above the national average.

Small businesses with at least one employee besides the owner can qualify for small business health insurance. This allows them to offer group health insurance, which is often less expensive than individual plans with similar benefits. However, there is typically a requirement to enroll at least 70% of uninsured, full-time employees, although this rule has exceptions. For instance, during the enrollment period from November 15 to December 15, small businesses can be approved with fewer than 70% of eligible full-time employees participating.

Vermont State Insurance: Herpes Medication Coverage Explained

You may want to see also

Explore related products

![]()

Employers can reimburse employees tax-free for medical expenses

Health insurance is a significant incentive for employees, helping businesses to recruit and retain workers. According to a 3-year average based on 2020-2022 data, about 86% of U.S. private-sector employees worked for establishments that offered employer-sponsored health insurance.

A small business must have between one and 50 employees to qualify for small business health insurance. The employees must be full-time or full-time equivalent, working at least 30 hours per week. To offer group coverage, at least 70% of uninsured, full-time employees must be enrolled, though this rule does not apply if enrollment occurs between November 15 and December 15 of the year.

There are several ways in which employers can reimburse employees tax-free for medical expenses. One way is through a Health Reimbursement Arrangement (HRA), an employer-sponsored plan that reimburses participants for eligible medical expenses, including health insurance premiums and other qualified out-of-pocket medical costs, such as prescription drugs and doctor visits. The business owner sets a maximum dollar amount for a coverage period, and the reimbursements are not included in the employee's income. Unused funds can be carried forward or remain with the employer if an employee quits or retires.

Another option is a health stipend, where employers offer employees a fixed, taxable amount of money to help pay for health insurance and other medical expenses. This option is more flexible, as there are fewer compliance requirements, but it is also taxable. A third option is a Qualified Small Employer HRA (QSEHRA), available to employers with fewer than 50 full-time equivalent employees who do not want to offer group health insurance. With a QSEHRA, employers can reimburse employees tax-free for medical expenses, including health insurance premiums, up to a maximum contribution limit.

Finally, an Individual Coverage Health Reimbursement Arrangement (ICHRA) allows businesses of all sizes to reimburse employees tax-free for their healthcare expenses. Employees can choose their own health insurance plan, and the employer reimburses them for premiums and qualified healthcare costs up to a defined amount.

Elected Officials: Free Medical Insurance or Not?

You may want to see also

Explore related products

![]()

Health insurance coverage is a significant recruitment incentive

Health insurance coverage is a significant factor in recruitment, with a comprehensive health benefits package no longer viewed as a mere perk. It is a powerful draw for top talent, representing an employer's dedication to the holistic well-being of their employees. This is particularly relevant in an era where work-life balance and mental health are gaining attention, with prospective employees evaluating potential employers based on their support for overall health and well-being.

In a competitive market, an employer that prioritizes employee health stands out. A study by the Kaiser Family Foundation revealed that employees with access to quality health benefits are significantly less likely to seek employment elsewhere, reducing turnover rates and recruitment expenses. This is especially true for small businesses, which can use health insurance as a tool to compete with larger corporations.

The Medical Expenditure Panel Survey - Insurance Component (MEPS-IC) is the most comprehensive study on health insurance benefits offered by employers. According to MEPS-IC data, about 86% of U.S. private-sector employees worked for companies that offered employer-sponsored health insurance from 2020 to 2022. This percentage varied across states, with a 3-year average low of 70.5% in Wyoming and a high of 97.5% in Hawaii.

There are various ways employers can provide health insurance coverage to their employees. Group health insurance is an option for small businesses with at least one employee besides the owner, and it can often be less expensive than individual plans. Alternatively, employers can use health reimbursement arrangements (HRAs) to reimburse employees tax-free for their medical expenses, including health insurance premiums, up to a maximum contribution limit. This allows employees to choose their own health insurance plan while still receiving financial support from their employer.

Medical Insurance and IVF: What's Covered?

You may want to see also

Frequently asked questions

To qualify for small business health insurance, a company must have between one and 50 employees. The business owner must also be considered an employee, and at least one other employee who is not an owner must exist and enrol in the group health plan.

This depends on the company and the insurance plan. For single coverage plans, employers paid between 76% and 80% of premiums for workers with the lowest 10% of wages, and between 59% and 71% for workers with the highest 10% of wages.

Preferred Provider Organization (PPO) plans are the most common type of health insurance provided by employers, with 47% of all firms offering these plans in 2023.

The insurance industry in the US has seen growth in the number of health insurance employees. However, the number of employees in life insurance has decreased, and the industry as a whole is facing stagnation due to many professionals retiring and positions being left vacant or replaced by automation.

![[8 Pack 4" x 5 Yards] Beige-Self Adhesive Cohesive Bandage Wrap, Self Adherant Non-Woven Wrap Rolls, Atheletic Tape for Wrist, Ankle, Hand, Leg, Premium-Grade Medical Stretch Wrap](https://m.media-amazon.com/images/I/81wGnSXRl8L._AC_UL320_.jpg)