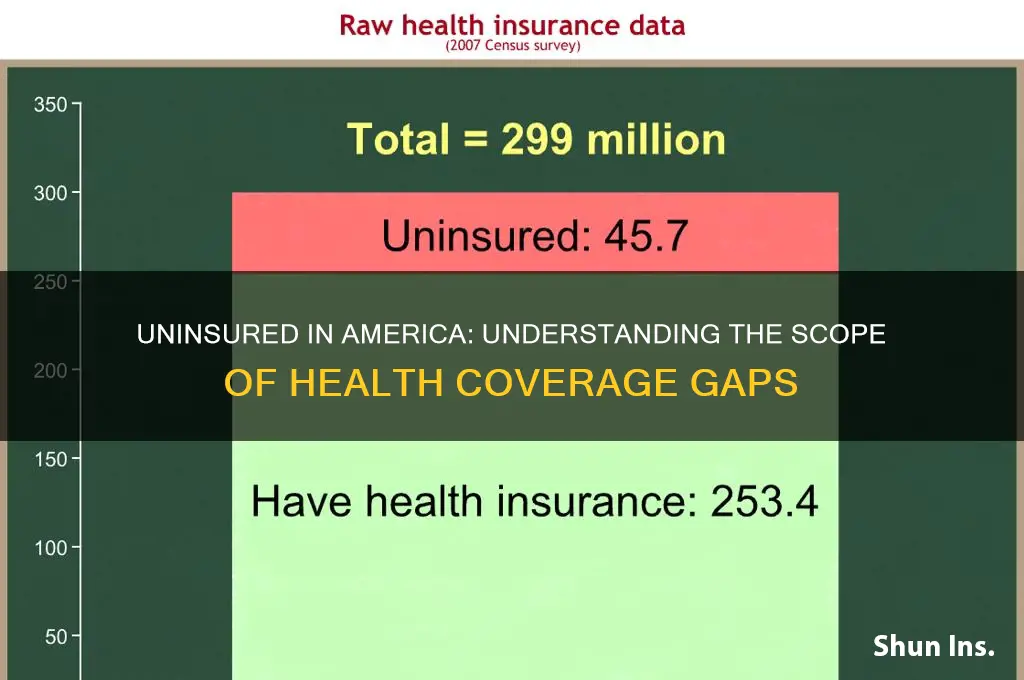

The issue of health insurance coverage in the United States remains a pressing concern, with millions of Americans lacking access to essential healthcare services. Despite efforts to expand coverage through initiatives like the Affordable Care Act, a significant portion of the population still remains uninsured. Understanding the scope of this problem is crucial, as it highlights disparities in access to healthcare and the financial burden faced by those without insurance. Recent data indicates that approximately 8.5% of the U.S. population, or around 28 million people, were uninsured in 2022, a figure that underscores the ongoing challenges in achieving universal healthcare coverage. Factors such as income inequality, employment status, and state policies on Medicaid expansion play a critical role in determining who remains uninsured, making this a complex and multifaceted issue that demands attention and actionable solutions.

| Characteristics | Values (2022) |

|---|---|

| Total Uninsured Population (USA) | Approximately 28.9 million people (8.5% of the population) |

| Age Group with Highest Uninsured | 26-34 years old (13.9%) |

| Age Group with Lowest Uninsured | 65+ years old (1.0%) (due to Medicare eligibility) |

| Uninsured by Race/Ethnicity | Hispanic (18.0%), American Indian/Alaska Native (16.6%), Black (9.9%), White (5.9%), Asian (5.3%) |

| Uninsured by Income Level | Lowest income bracket (<138% FPL): 17.3% uninsured |

| Uninsured by Employment Status | Part-time workers: 20.6% uninsured; Unemployed: 23.1% uninsured |

| Uninsured by State | Texas (18.4%), Oklahoma (14.3%), Georgia (13.4%) (highest rates) |

| Uninsured by Education Level | Less than high school: 25.9% uninsured |

| Children (<18) Uninsured | 5.0% (approximately 3.8 million children) |

| Impact of Medicaid Expansion | States with expansion: 7.3% uninsured; Non-expansion states: 12.6% uninsured |

| Source | U.S. Census Bureau, Current Population Survey (CPS) 2022 |

Explore related products

What You'll Learn

![]()

Uninsured rates by state

Texas leads the nation in uninsured rates, with approximately 18% of its residents lacking health coverage. This stark figure is nearly double the national average, highlighting deep-rooted disparities in access to healthcare. The state’s decision not to expand Medicaid under the Affordable Care Act (ACA) plays a significant role, leaving hundreds of thousands of low-income adults in a coverage gap—earning too much for traditional Medicaid but too little to afford private insurance. High uninsured rates in Texas also correlate with its large population of undocumented immigrants, who are ineligible for most federal health programs. Employers in the state are less likely to offer health benefits compared to national averages, further exacerbating the issue. Addressing this crisis requires policy changes, such as Medicaid expansion, to close the gap and improve public health outcomes.

In contrast, states like Massachusetts and Vermont boast some of the lowest uninsured rates in the country, hovering around 3% and 4%, respectively. Massachusetts, often cited as a model for healthcare reform, implemented its own health insurance mandate in 2006, which later inspired the ACA. The state’s Health Connector program offers subsidized plans for low- and middle-income residents, while its Medicaid expansion ensures broad coverage for vulnerable populations. Vermont’s success stems from its commitment to a single-payer system, though it has not fully realized this goal. Instead, the state has focused on expanding Medicaid and creating a robust marketplace with low-cost options. Both states demonstrate that a combination of policy innovation, public investment, and a culture of health equity can dramatically reduce uninsured rates.

Southern states, including Mississippi, Georgia, and Florida, cluster at the higher end of uninsured rates, ranging from 12% to 15%. These states share a common thread: they have not expanded Medicaid, leaving millions of residents without affordable coverage options. In Mississippi, for example, nearly 100,000 adults fall into the coverage gap, earning too much for traditional Medicaid but too little to qualify for ACA subsidies. Georgia has taken a unique approach by implementing a partial Medicaid expansion with work requirements, but its impact remains limited. Florida, despite its large population and economic resources, has one of the highest uninsured rates due to political resistance to expansion. These states illustrate how policy decisions directly influence health outcomes, with residents paying the price in terms of delayed care and financial strain.

Even in states with relatively low uninsured rates, disparities persist, particularly among specific demographics. In California, for instance, the overall uninsured rate is around 7%, but it rises to 17% for undocumented immigrants, who are excluded from state and federal programs. Similarly, in New York, while the state’s uninsured rate is 5%, young adults aged 19–34 and part-time workers are more likely to lack coverage due to cost barriers. These examples underscore the importance of targeted solutions, such as state-funded programs for excluded groups or subsidies for young adults. Policymakers must address these gaps to ensure that progress in reducing uninsured rates benefits all residents, not just the majority.

For individuals living in states with high uninsured rates, practical steps can mitigate the lack of coverage. First, explore state-run health insurance marketplaces, which often offer subsidized plans based on income. For example, in Texas, residents earning up to 400% of the federal poverty level may qualify for premium tax credits. Second, consider community health centers, which provide low-cost or sliding-scale services regardless of insurance status. Third, enroll in Medicaid if eligible, even in non-expansion states, as children and some low-income adults may still qualify. Finally, advocate for policy changes at the local and state levels, such as Medicaid expansion, to create systemic solutions. While individual actions can provide temporary relief, collective efforts are essential to address the root causes of high uninsured rates.

Understanding Medical Insurance: Employer Responsibilities and Obligations

You may want to see also

Explore related products

![]()

Impact of income on coverage

Income is a critical determinant of health insurance coverage in the United States, with disparities starkly evident across income brackets. According to the U.S. Census Bureau, in 2022, 8.5% of the population was uninsured, but this rate varied dramatically by income level. Among individuals living below the federal poverty level (FPL), the uninsured rate was 17.3%, compared to just 4.5% for those with incomes at or above 400% of the FPL. This data underscores a clear inverse relationship: as income rises, the likelihood of being uninsured plummets. The Affordable Care Act (ACA) expanded Medicaid to cover more low-income individuals, yet gaps persist due to state-level variations in Medicaid expansion and eligibility criteria. For instance, in states that have not expanded Medicaid, many low-income adults fall into the "coverage gap," earning too much to qualify for Medicaid but too little to afford private insurance.

To illustrate the impact of income on coverage, consider a family of four earning $30,000 annually, which is roughly 125% of the FPL. In a non-expansion state, this family may not qualify for Medicaid, and the cost of private insurance—averaging $20,000 annually for a family plan—is prohibitively expensive. Conversely, a family earning $100,000 (400% of the FPL) can access employer-sponsored insurance or ACA marketplace plans with subsidies, significantly reducing out-of-pocket costs. This disparity highlights how income not only determines access to insurance but also the quality and affordability of coverage. Practical steps for low-income individuals include exploring ACA marketplace plans during open enrollment, applying for Medicaid if eligible, and utilizing community health centers for low-cost care.

A comparative analysis of income and coverage reveals systemic barriers that exacerbate inequities. High premiums, deductibles, and out-of-pocket costs disproportionately affect lower-income households, often forcing them to forgo insurance altogether. For example, a study by the Kaiser Family Foundation found that 45% of uninsured adults cited cost as the primary reason for lacking coverage. In contrast, higher-income individuals benefit from employer-sponsored plans, which cover an average of 70% of premiums, making insurance more accessible. This divide is further compounded by occupational disparities, as low-wage workers are less likely to be offered employer-sponsored insurance. Policymakers could address this by expanding Medicaid in all states and increasing premium subsidies for low-income individuals, ensuring coverage is not a luxury but a universal right.

Persuasively, the argument for income-based coverage solutions is strengthened by the long-term societal benefits. Uninsured individuals often delay or forgo necessary care, leading to poorer health outcomes and higher costs for the healthcare system. For instance, untreated chronic conditions like diabetes or hypertension can result in costly emergency room visits, which are 10 times more expensive than preventive care. By ensuring low-income populations have access to affordable coverage, the nation could reduce overall healthcare spending and improve public health. A descriptive example is the success of Medicaid expansion in states like Kentucky and Arkansas, where uninsured rates dropped by over 50% post-expansion, demonstrating the transformative potential of income-targeted policies.

In conclusion, the impact of income on health insurance coverage is a multifaceted issue requiring targeted solutions. From expanding Medicaid to increasing premium subsidies, addressing income disparities can bridge the coverage gap and ensure equitable access to care. For individuals, understanding eligibility criteria and available resources is crucial. For policymakers, prioritizing income-based reforms is not just a moral imperative but a strategic investment in a healthier, more equitable society.

Diabetics: Choosing the Right Medical Insurance Plan

You may want to see also

Explore related products

![]()

Racial disparities in insurance

Racial and ethnic minorities in the United States face significant disparities in health insurance coverage, perpetuating broader inequalities in healthcare access and outcomes. According to the U.S. Census Bureau, as of 2022, 8.0% of the total population was uninsured. However, this figure masks stark differences: 9.3% of Hispanic individuals, 9.0% of American Indian and Alaska Native individuals, and 6.5% of Black individuals lacked coverage, compared to 5.4% of non-Hispanic White individuals. These gaps highlight systemic barriers that disproportionately affect communities of color.

One key driver of these disparities is the intersection of race with socioeconomic factors. Minority groups are more likely to work in low-wage jobs that do not offer employer-sponsored insurance, the primary source of coverage for most Americans. For example, 44% of Hispanic workers and 38% of Black workers are employed in service occupations, where health benefits are often unavailable. Additionally, states with higher minority populations are more likely to have opted out of Medicaid expansion under the Affordable Care Act, leaving millions in the "coverage gap"—earning too much to qualify for Medicaid but too little to afford private insurance.

Policy solutions must address these structural inequities directly. Expanding Medicaid in the 10 remaining non-expansion states would immediately reduce uninsured rates among minorities, as these states are home to a disproportionate share of uninsured Black and Hispanic individuals. Simultaneously, increasing funding for community health centers in underserved areas can provide a safety net for those without insurance. Employers can also play a role by offering affordable health benefits to low-wage workers, regardless of their racial or ethnic background.

Beyond policy, addressing racial disparities in insurance requires tackling implicit biases and systemic racism within healthcare systems. Studies show that minority patients are less likely to receive adequate care, even when insured, due to provider biases and cultural misunderstandings. Training healthcare professionals in cultural competency and implementing anti-bias protocols can improve outcomes for insured minority patients while encouraging uninsured individuals to seek care when needed.

Ultimately, closing the racial gap in health insurance coverage is not just a moral imperative but a practical one. Uninsured minority populations face higher rates of chronic conditions, delayed care, and preventable hospitalizations, driving up overall healthcare costs. By ensuring equitable access to insurance, the U.S. can improve health outcomes for marginalized communities while building a more sustainable healthcare system for all.

Long-Term Health Insurance: Impact on Medicaid Eligibility

You may want to see also

Explore related products

![]()

Effect of policy changes

Policy changes have a direct and measurable impact on the number of uninsured individuals in the United States. For instance, the Affordable Care Act (ACA), implemented in 2010, led to a significant reduction in the uninsured rate, dropping from 16% in 2010 to 8.6% in 2016. This was achieved through expanded Medicaid eligibility, the establishment of health insurance marketplaces, and subsidies for low- and middle-income individuals. The ACA’s mandate requiring individuals to have health insurance or pay a penalty further incentivized enrollment. However, subsequent policy shifts, such as the elimination of the individual mandate penalty in 2019, contributed to a slight uptick in uninsured rates, demonstrating the sensitivity of coverage levels to legislative changes.

Consider the Medicaid expansion as a case study in policy impact. States that expanded Medicaid under the ACA saw uninsured rates drop by an average of 10 percentage points more than non-expansion states. For example, Kentucky’s uninsured rate fell from 14.3% in 2013 to 5.8% in 2016 after expanding Medicaid. In contrast, states like Texas, which opted not to expand, experienced smaller reductions. This disparity highlights how state-level policy decisions can exacerbate or alleviate coverage gaps, particularly among low-income populations. Policymakers should note that expanding Medicaid not only reduces uninsured rates but also improves access to preventive care and financial stability for vulnerable groups.

To maximize the impact of policy changes, a multi-pronged approach is essential. First, restore and strengthen the individual mandate or introduce alternative incentives for enrollment, such as tax credits for maintaining coverage. Second, encourage remaining non-expansion states to adopt Medicaid expansion by highlighting its economic benefits, including reduced uncompensated care costs for hospitals. Third, simplify enrollment processes by streamlining applications and increasing outreach efforts, particularly in underserved communities. For example, California’s Covered California program reduced uninsured rates by offering multilingual support and in-person assistance, a model other states could replicate.

A cautionary note: policy changes must consider unintended consequences. For instance, while the ACA expanded coverage, some individuals faced higher premiums or limited provider networks, leading to dissatisfaction. Policymakers should balance expanding access with ensuring affordability and quality. Additionally, frequent policy reversals create uncertainty, discouraging enrollment. A stable, long-term policy framework is crucial for sustained reductions in uninsured rates. By learning from past successes and failures, policymakers can design effective strategies that address the root causes of uninsurance.

Mastering Health Insurance Project Explanations in Job Interviews

You may want to see also

![]()

Uninsured children statistics

As of recent data, approximately 4.3 million children in the United States lack health insurance, a figure that underscores a persistent gap in coverage despite broader national efforts to expand access. This statistic is particularly alarming when considering the long-term health and developmental consequences for uninsured children, who are less likely to receive preventive care, immunizations, and timely treatment for illnesses. The disparity is not evenly distributed; children in low-income families, racial and ethnic minority groups, and those living in states that have not expanded Medicaid are disproportionately affected. For instance, Hispanic children account for nearly 40% of uninsured children nationwide, highlighting systemic barriers to access.

Analyzing the data reveals a critical interplay between state policies and child insurance rates. States that have expanded Medicaid under the Affordable Care Act (ACA) have seen significant reductions in uninsured children, with rates as low as 2% in some regions. Conversely, states that have not expanded Medicaid report uninsured rates for children exceeding 7%. This variation suggests that policy decisions at the state level have a direct and measurable impact on children’s access to healthcare. For parents and advocates, understanding these geographic disparities is essential for targeting efforts to improve coverage.

From a practical standpoint, enrolling uninsured children in available programs requires navigating a complex landscape of options. The Children’s Health Insurance Program (CHIP) and Medicaid are the primary safety nets, offering low-cost or free coverage for eligible families. However, many parents remain unaware of these programs or face administrative hurdles during the application process. Simplifying enrollment procedures, such as allowing year-round sign-ups and reducing documentation requirements, could significantly increase participation. Schools and community organizations can play a pivotal role by hosting enrollment events and providing multilingual resources to reach underserved populations.

A comparative perspective highlights the stark contrast between the U.S. and other high-income countries, where universal healthcare ensures near-total coverage for children. In the U.K., for example, the National Health Service (NHS) provides automatic access to healthcare from birth, eliminating the risk of children going uninsured. While the U.S. system differs structurally, this comparison underscores the feasibility of achieving universal child coverage through policy reforms. Advocates argue that closing the insurance gap for children is not only a moral imperative but also an economic one, as uninsured children are more likely to require costly emergency care later in life.

Ultimately, addressing the issue of uninsured children requires a multifaceted approach that combines policy reform, community engagement, and public awareness. Policymakers must prioritize expanding Medicaid in non-expansion states and streamline enrollment processes to reduce barriers. Simultaneously, grassroots efforts to educate families about available programs and assist with applications can bridge the gap in access. By focusing on these strategies, the U.S. can move closer to ensuring that every child has the healthcare they need to thrive.

Health Insurance Truths: Debunking Common Myths and Misconceptions

You may want to see also

Frequently asked questions

As of 2023, approximately 8-10% of the U.S. population, or around 27-30 million people, are estimated to be without health insurance, though numbers may vary by source.

The primary reasons include high insurance costs, lack of employer-sponsored coverage, ineligibility for public programs like Medicaid, and gaps in coverage due to job changes or income fluctuations.

States with the highest uninsured rates include Texas, Florida, Georgia, and Oklahoma, often due to stricter Medicaid eligibility rules and lower enrollment in public health programs.