Health insurance in the United States is a complex issue, with many factors influencing an individual's access to healthcare services. While employer-sponsored health insurance is common, it is not universal, and the specific plans offered vary greatly. The size of the company, the industry it operates in, and the state it is located in can all impact the availability and quality of health insurance plans for employees. This article will explore the landscape of job-based health insurance in the US, examining the factors that determine eligibility and coverage, and discussing the implications for Americans' financial and physical well-being.

| Characteristics | Values |

|---|---|

| Percentage of U.S. private-sector employees whose employers offer health insurance | 86% |

| States with the lowest percentage of private-sector employees offered health insurance | Wyoming (70.5%) |

| States with the highest percentage of private-sector employees offered health insurance | Hawaii (97.5%) |

| Types of health insurance plans offered by employers | PPO, HDHP/SO, HMO, and POS |

| Most common type of health insurance plan offered by employers | PPO |

| Factors influencing the type of health insurance plan chosen | Type of medical service, network status of healthcare provider, coverage percentage, company size, industry |

| Percentage of the U.S. population eligible for health insurance through their employers | 78% |

| Average monthly cost for an individual with employer-sponsored health insurance | $100 |

| Average monthly cost for a family with health insurance | $1,200 |

Explore related products

What You'll Learn

![]()

Group health insurance is common

Group health insurance, or employer-sponsored health insurance, is prevalent in the United States. It is a significant recruitment and retention incentive, with about 86% of US private-sector employees working for companies that offer such benefits, according to 2020-2022 data. This figure varies across US states, with a 3-year average low of 70.5% in Wyoming and a high of 97.5% in Hawaii.

The specific health insurance plan, such as a preferred provider organization (PPO) or a health maintenance organization (HMO), influences the coverage percentage. PPO plans are the most common, followed by HDHP/SO plans, while HMO and POS plans are less common but still significant. The plan's tier or level (bronze, silver, gold, or platinum) can also impact coverage percentages. Other factors affecting coverage include the type of medical service, the provider's network status, and whether the service is in-network or out-of-network.

Company size and industry also play a role in the coverage available in employer-sponsored plans. Larger companies often secure comprehensive coverage with lower premiums, providing employees with a broader network of providers and lower out-of-pocket costs. In contrast, smaller companies may offer basic plans with higher deductibles and copayments.

While group health insurance is common, it is rarely completely free for employees. Full-time employees often pay a portion of the coverage premium, ranging from $250 to $300 per month, plus deductibles and copayments. However, the average single-person contribution with employer-sponsored insurance is about $100/month.

The significance of employer-sponsored health insurance lies in its ability to provide financial protection and access to healthcare services for employees, helping them maintain their health and well-being. It reduces the financial burden of medical expenses, offering peace of mind and ensuring they can seek necessary care without incurring excessive costs. Employers benefit by attracting and retaining top talent, boosting morale and productivity, and enjoying potential tax incentives.

Understanding Insurance and Medicaid: Working Together

You may want to see also

Explore related products

![]()

Employer-sponsored health insurance

In the United States, employer-sponsored health insurance is health coverage provided to employees (and their dependents) by their employer. This type of insurance is the most common type of health coverage in the country, with nearly half of the American population having employer-sponsored insurance. It is often referred to as ESI (employer-sponsored health insurance).

The Medical Expenditure Panel Survey - Insurance Component (MEPS-IC) is the most comprehensive study on health insurance benefits offered by employers in the US. According to the MEPS-IC, about 86% of US private-sector employees worked for companies that offered employer-sponsored health insurance from 2020 to 2022. At the state level, the percentage of employees in establishments offering health insurance ranged from a low of 70.5% in Wyoming to a high of 97.5% in Hawaii.

The Affordable Care Act, signed into law in 2010, includes an employer mandate that requires businesses with at least 50 full-time equivalent employees to offer affordable, minimum-value insurance to their full-time (30+ hours per week) workers. Employers can purchase small-group or large-group coverage, depending on the number of employees they have. They can also choose to self-insure, which means paying for employees' medical claims out of pocket rather than purchasing coverage from an insurer. In 2023, the average employer-sponsored health plan had a monthly premium of $703 for a single employee and $1,997 for family coverage. On average, employees contribute a portion of the premiums through payroll deductions, copays, coinsurance, and/or deductibles.

Employers may also offer an ICHRA (Individual Coverage Health Reimbursement Arrangement), where they reimburse employees for some or all of the costs of obtaining individual market coverage. Additionally, employers often provide supplemental coverage, such as dental, vision, life, and disability insurance.

Insurance Coverage for Weight Loss Medication: What's Included?

You may want to see also

Explore related products

![]()

Health insurance as a recruitment incentive

Health insurance has become an important recruitment incentive for companies in the United States. In a job market where skilled talent has multiple options, an employer that prioritises employee health stands out. This is especially true for younger generations entering the workforce, who increasingly prioritise health and wellness when choosing an employer.

According to data from the Insurance Component of the Medical Expenditure Panel Survey (MEPS-IC), about 86% of US private-sector employees worked for companies that offered employer-sponsored health insurance from 2020 to 2022. At the state level, the percentage of private-sector employees who had access to health insurance ranged from a low of 70.5% in Wyoming to a high of 97.5% in Hawaii.

Health benefits are not just a recruitment tool but also a means to ensure a healthy and productive workforce. By providing comprehensive health coverage, employers can reduce absenteeism, improve employee morale, and enhance overall productivity. Additionally, in an era where work-life balance and mental health are gaining attention, offering comprehensive health benefits is seen as a commitment to these values.

Wellness incentive plans are a strategy used by companies to promote workforce well-being. These plans offer rewards in the form of direct compensation, reduced medical premiums, or other cost-sharing discounts for completing a particular health promotion activity. Alternatively, some incentive programs charge employees higher fees for not engaging in health improvement activities or refraining from unhealthy behaviours.

A notable example of a company successfully using health benefits as a strategic tool in recruitment is a tech giant that offers comprehensive medical coverage, mental health support, and wellness programs. This sets a benchmark in the industry and makes the company a desirable place to work. A study by the Kaiser Family Foundation revealed that employees with access to quality health benefits are significantly less likely to seek employment elsewhere, highlighting the importance of health benefits as a retention tool in addition to recruitment.

Understanding Medical Billing: Insurance Collection Timeframes

You may want to see also

Explore related products

![]()

Affordability issues

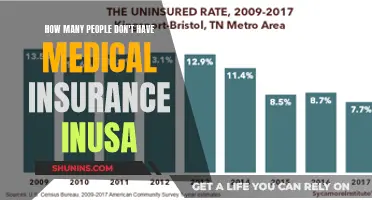

The cost of healthcare in the United States is a significant burden for many US families, with around half of US adults finding it difficult to afford healthcare costs. This has led to many Americans struggling with medical debt, with around 4 in 10 adults reporting debt due to medical or dental bills. This debt is owed to credit card companies, collection agencies, family and friends, banks, and other lenders. Healthcare affordability is a pressing issue, with many voters wanting to hear presidential candidates discuss it during the 2024 election.

Healthcare costs influence decisions about insurance coverage and care-seeking behaviours. The high costs and the prospect of unexpected medical bills are the top financial concerns for adults and their families. Lowering out-of-pocket healthcare costs is the public's top healthcare priority. Many Americans with insurance still struggle with the burden of healthcare costs, with around half of insured adults worrying about affording their monthly health insurance premiums.

The cost of healthcare leads some people to delay or avoid seeking necessary care. One in four adults has skipped or postponed healthcare due to cost in the past year, and this figure rises to 6 in 10 for uninsured adults. The cost of prescription drugs also prevents some people from filling prescriptions, with around one in five adults not filling a prescription due to cost. Some people opt for over-the-counter alternatives, while others cut pills in half or skip doses to make their prescriptions last longer.

The relentless growth in healthcare costs, driven by prices paid to providers and for pharmaceuticals, is at the root of the nation's medical debt and affordability crisis. Private payers, federal and state policymakers, and employers all have a role to play in slowing cost growth and improving coverage. For example, employers can adjust premiums and cost-sharing based on employee income, and states can explore policies such as rate regulation to limit premium growth.

Captain D's Employee Benefits: Medical Insurance Offered?

You may want to see also

Explore related products

$19.99 $19.99

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

![]()

Part-time work and health insurance

While health insurance is a valuable workplace benefit, not all employers in the United States offer it to their part-time workers. By law, employers of a certain size must provide health insurance to full-time workers, but this does not always extend to those working fewer hours per week. However, some companies do provide health insurance to their part-time employees, and there are other ways for part-time workers to access health insurance.

According to the Affordable Care Act (ACA), or Obamacare, "full-time" is defined as 30 hours or more per week. Therefore, if you work 30 hours or more per week and your employer is large enough, they should provide you with health insurance. Some employers may market this as a perk, but it is actually an obligation. However, it is important to note that not all employers are required to provide health insurance for their part-time employees, even if they offer coverage to full-time staff.

If your employer does not offer you health insurance, you can explore other options. One option is to purchase health insurance through the Health Insurance Marketplace. You may qualify for savings or premium tax credits based on your income, household size, and whether the coverage is offered to spouses and dependents. Additionally, you can look for part-time jobs with companies that are known to offer health insurance to their part-time employees. For example, companies like Activision Blizzard, the American Red Cross, Aquent, Costco, and CVS Health offer health insurance to part-time workers who work at least 20 to 30 hours per week.

Another option for part-time workers seeking health insurance is to consider working for the federal government. No matter how few hours you work, as long as your position is permanent, you will be eligible for the same health insurance benefits as full-time employees. The percentage of your premium covered by the government will depend on the number of hours you work, with part-time employees paying a greater percentage. You can find federal government jobs at agencies such as the Postal Service, the Internal Revenue Service, the Federal Bureau of Investigation, and the Department of Veterans Affairs.

Arizona's OHP-Style Medical Insurance: What You Need to Know

You may want to see also

Frequently asked questions

No, not all jobs in the US offer health insurance. However, according to the Insurance Component of the Medical Expenditure Panel Survey (MEPS-IC), about 86% of US private-sector employees work for companies that offer employer-sponsored health insurance.

Yes, the size of the company can influence the availability and type of health insurance plans offered. Larger companies often have more negotiating power to secure comprehensive coverage with lower premiums, while smaller companies may offer more basic plans with higher deductibles and copayments.

Employer-sponsored health insurance provides financial protection and access to healthcare services for employees, helping them maintain their health and well-being. It reduces the financial burden of medical expenses, offering peace of mind and ensuring employees can seek necessary medical care without incurring excessive costs.