The health insurance penalty, also known as the individual shared responsibility payment, was a fee imposed on individuals who did not have qualifying health coverage for three or more months during the year, as mandated by the Affordable Care Act (ACA). However, starting in 2019, the federal penalty was effectively eliminated due to the Tax Cuts and Jobs Act, which reduced the penalty amount to $0. While the federal penalty no longer applies, some states, such as California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have implemented their own health insurance mandates and penalties for residents who go without coverage. The duration of the penalty typically depends on the number of months an individual remains uninsured, with each month without coverage potentially incurring a separate charge. Understanding these state-specific requirements is crucial for avoiding financial penalties and ensuring compliance with local healthcare regulations.

Explore related products

What You'll Learn

- Penalty Calculation Methods: How the health insurance penalty is calculated based on income and coverage gaps

- Penalty Exemptions: Conditions under which individuals can avoid paying the health insurance penalty

- State vs. Federal Penalties: Differences in penalties between states with and without individual mandates

- Penalty Payment Process: How and when to pay the health insurance penalty on tax returns

- Penalty Changes Over Time: Historical and current trends in health insurance penalty amounts and rules

![]()

Penalty Calculation Methods: How the health insurance penalty is calculated based on income and coverage gaps

The health insurance penalty, often referred to as the individual shared responsibility payment, is calculated using a method that considers both income and coverage gaps. For those who go without qualifying health insurance, the penalty is designed to encourage compliance with the Affordable Care Act’s mandate. The calculation is not one-size-fits-all; it adjusts based on individual circumstances, making it essential to understand the factors at play. For instance, the penalty is either a flat dollar amount or a percentage of household income, whichever is greater, ensuring that it scales with financial capability.

Step 1: Determine the Flat Dollar Amount

The flat dollar amount for the penalty is set annually and varies by age. For example, in 2023, the penalty for an uninsured adult was $750, while for a child, it was $375. These amounts are then capped at a family maximum, typically three times the adult penalty. This method provides a baseline penalty that applies regardless of income, ensuring even those with lower earnings face a consequence for lacking coverage.

Step 2: Calculate the Percentage of Household Income

The income-based penalty is more complex. It is calculated as a percentage of the household income that exceeds the tax filing threshold. For 2023, the penalty was 2.5% of the income above the threshold. For example, if a family’s income was $60,000 and the filing threshold was $27,000, the penalty would apply to $33,000. At 2.5%, this results in an $825 penalty. This method ensures that higher-income individuals face a proportionally larger penalty, aligning the financial consequence with their ability to pay.

Coverage Gaps and Prorated Penalties

The penalty is prorated based on the number of months without coverage. If someone lacks insurance for only part of the year, the penalty is calculated for those specific months. For instance, six months without coverage would result in a penalty that is half of the annual amount. This proration encourages individuals to maintain coverage as consistently as possible, even if they experience gaps.

Practical Tips for Minimizing Penalties

To avoid or minimize penalties, individuals should aim to maintain continuous coverage throughout the year. Short coverage gaps of less than three consecutive months may qualify for a hardship exemption, reducing the penalty. Additionally, enrolling in a qualifying health plan during open enrollment or a special enrollment period can prevent penalties altogether. For those with fluctuating incomes, estimating annual earnings accurately can help in choosing the right coverage to avoid unexpected penalties.

Understanding these calculation methods empowers individuals to make informed decisions about their health insurance, ensuring compliance while minimizing financial strain. By focusing on income, coverage gaps, and prorated penalties, the system balances fairness with accountability.

Adding Your Adopted Child to Farm Bureau Health Insurance: A Guide

You may want to see also

Explore related products

![]()

Penalty Exemptions: Conditions under which individuals can avoid paying the health insurance penalty

In the United States, the Affordable Care Act (ACA) introduced the individual mandate, requiring most individuals to have health insurance or pay a penalty. However, not everyone is subject to this penalty, as certain conditions and circumstances can exempt individuals from paying it. Understanding these exemptions is crucial for those who may struggle to afford health insurance or have unique situations that make coverage impractical.

One of the primary ways to avoid the health insurance penalty is by qualifying for a coverage gap exemption. This exemption applies if you lacked coverage for less than three consecutive months during the year. For instance, if you were without insurance from January to March but then obtained coverage, you might be exempt from the penalty for those months. It’s essential to document these gaps accurately, as the IRS may require proof of your uninsured periods.

Another exemption category is based on financial hardship. If the cost of the cheapest available health insurance plan exceeds 8.5% of your household income, you may qualify for a hardship exemption. This calculation is based on the federal poverty level and the premiums in your area. For example, a single individual earning $30,000 annually in a state with high premiums might find that even the lowest-cost plan exceeds this threshold, making them eligible for an exemption.

Certain life events and personal circumstances can also exempt you from the penalty. These include experiencing homelessness, facing eviction or foreclosure, or dealing with domestic violence. Additionally, individuals who are incarcerated, members of certain religious sects with religious objections to insurance, or those with a shortfall in coverage due to errors by the insurance marketplace may qualify. Each of these exemptions requires specific documentation, such as a letter from a shelter or a statement from a religious leader.

For those with income below the tax filing threshold, the penalty does not apply. This exemption is automatically granted if your income is too low to require filing a federal tax return. However, it’s important to note that this threshold varies by filing status and age. For example, in 2023, a single individual under 65 would need to earn less than approximately $12,950 to qualify for this exemption.

Lastly, individuals who are not legally present in the United States, such as undocumented immigrants, are exempt from the penalty. This exemption is automatic and does not require an application. However, lawfully present immigrants, including those with green cards or visas, are subject to the mandate unless they qualify for other exemptions.

By understanding these exemptions, individuals can navigate the complexities of the health insurance penalty and determine whether they can avoid paying it. Each exemption has specific criteria and documentation requirements, so it’s crucial to review your situation carefully and consult resources like the IRS or healthcare.gov for guidance.

Maryland ACA Health Insurance: Licensed Companies for Affordable Care

You may want to see also

Explore related products

![]()

State vs. Federal Penalties: Differences in penalties between states with and without individual mandates

The Affordable Care Act's individual mandate, which required most Americans to have health insurance or pay a penalty, was effectively eliminated at the federal level starting in 2019. However, this shift has created a patchwork of regulations as some states have implemented their own individual mandates and corresponding penalties. Understanding these differences is crucial for residents navigating their tax obligations and healthcare choices.

Analyzing the Divide:

States with individual mandates, like California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have stepped in to fill the void left by the federal government's withdrawal. These states impose penalties on residents who go without qualifying health coverage for more than a specified period, typically a few months. For instance, California's penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child, or 2.5% of household income, whichever is greater.

In contrast, states without individual mandates, which constitute the majority, have no state-level penalties for lacking health insurance. Residents in these states are solely subject to any potential federal changes, which currently do not include penalties for being uninsured.

Practical Implications:

The existence of state-level mandates significantly impacts residents' financial planning and healthcare decisions. In mandate states, individuals must carefully consider their coverage options to avoid penalties. This might involve enrolling in employer-sponsored plans, purchasing insurance through state exchanges, or qualifying for exemptions based on income or other factors.

For residents in non-mandate states, the absence of penalties might seem like a relief, but it's important to remember that going without insurance can leave individuals vulnerable to high medical costs in case of illness or injury.

Looking Ahead:

The landscape of individual mandates and penalties is subject to change. Some states are considering implementing mandates, while others might adjust existing penalties. Staying informed about your state's specific regulations is essential. Regularly checking official state government websites and consulting with tax professionals can help individuals navigate these complexities and make informed decisions about their health coverage.

Genetic Data Privacy: Will Insurers Access Your DNA Information?

You may want to see also

Explore related products

![]()

Penalty Payment Process: How and when to pay the health insurance penalty on tax returns

The health insurance penalty, formally known as the Shared Responsibility Payment, was a fee imposed on individuals who went without qualifying health coverage for more than a short gap during the year. While the federal penalty was eliminated starting in 2019, some states, like California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have reinstated their own penalties for uninsured residents. Understanding how and when to pay these penalties on your tax returns is crucial to avoid additional fines or legal complications.

Steps to Pay the Penalty:

- Determine Your State’s Rules: If you live in a state with a health insurance mandate, check the specific penalty amount and calculation method. For example, California’s penalty is based on a percentage of your household income or a flat fee per uninsured adult and child, whichever is higher.

- File Your State Tax Return: The penalty is typically reported and paid when filing your state income tax return. Use the appropriate forms provided by your state’s tax agency. For instance, California requires Form 540 or 540NR.

- Calculate the Penalty: Multiply the number of months you were uninsured by the monthly penalty rate. For example, if you were uninsured for 6 months in California, the penalty would be 6 times the monthly flat fee or income-based amount.

- Include the Penalty in Your Payment: When submitting your tax return, ensure the penalty amount is added to your total tax due. Failure to pay may result in interest charges or collection actions.

Cautions to Consider:

- Partial Coverage Periods: If you were uninsured for part of a month, most states count that as a full month without coverage. Plan accordingly to avoid underestimating the penalty.

- Exemptions: Some states offer exemptions for financial hardship, religious beliefs, or other qualifying reasons. If eligible, file for an exemption to waive the penalty.

- Federal vs. State Penalties: While the federal penalty no longer applies, state penalties are enforced independently. Don’t assume federal rules apply to your state’s mandate.

Practical Tips:

- Keep Records: Document periods of coverage and exemptions to simplify penalty calculations and provide evidence if audited.

- Estimate Early: Use your state’s tax calculator to estimate the penalty before filing. This helps in budgeting and avoiding surprises.

- Seek Assistance: If unsure about the process, consult a tax professional or use state-provided resources to ensure accuracy.

By following these steps and precautions, you can navigate the penalty payment process efficiently, ensuring compliance with your state’s health insurance mandate while minimizing financial strain.

Report an Accident to Grange Insurance: Step-by-Step Guide

You may want to see also

Explore related products

![The Penalty [Blu-ray]](https://m.media-amazon.com/images/I/91fZ8MEHZ4L._AC_UY218_.jpg)

![]()

Penalty Changes Over Time: Historical and current trends in health insurance penalty amounts and rules

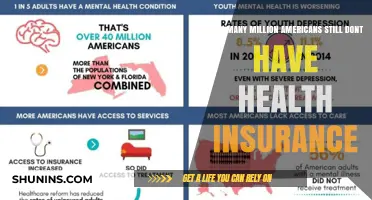

The Affordable Care Act's individual mandate penalty, once a fixed percentage of income or a flat fee (whichever was higher), has undergone significant transformations since its inception. Initially set at 1% of household income or $95 per adult ($47.50 per child) in 2014, the penalty escalated to 2.5% of income or $695 per adult ($347.50 per child) by 2016, with a family cap. This punitive structure aimed to encourage enrollment in health insurance plans, but its effectiveness was a subject of debate. The penalty was designed to be collected by the IRS, adding a layer of enforcement that made non-compliance financially risky for many.

However, the landscape shifted dramatically with the Tax Cuts and Jobs Act of 2017, which reduced the federal penalty to $0 starting in 2019. This change effectively eliminated the federal mandate penalty, though it didn’t abolish the requirement to have health insurance. States responded by implementing their own penalty systems to maintain coverage rates. For instance, California, New Jersey, and Massachusetts introduced state-level mandates with penalties mirroring the former federal structure, often calculated as a percentage of income or a flat fee. These state penalties are enforced through state tax returns, ensuring compliance remains a financial consideration for residents.

Analyzing these trends reveals a shift from federal to state-level enforcement, reflecting broader political and policy disagreements. The elimination of the federal penalty was framed as a reduction in government overreach, but it also led to concerns about increased uninsured rates and higher premiums for those remaining in the market. States with mandates have seen more stable insurance markets, suggesting that penalties remain an effective tool for encouraging coverage. However, the absence of a federal penalty has created a patchwork of rules, complicating compliance for individuals moving across state lines.

For those navigating this evolving landscape, understanding the rules in your state is crucial. If you live in a state with a mandate, calculate your potential penalty by reviewing the state’s formula—typically a percentage of income or a flat fee. For example, in California, the penalty for 2023 is the greater of $800 per adult ($400 per child) or 2.5% of household income over the tax filing threshold. Practical tips include enrolling in a qualifying health plan during open enrollment or a special enrollment period if you experience a life event, such as losing job-based coverage. Additionally, consider consulting a tax professional to ensure compliance and explore exemptions, such as those for financial hardship or short coverage gaps (less than three months).

In conclusion, the health insurance penalty has evolved from a federally enforced mandate to a state-by-state approach, with varying amounts and rules. This shift underscores the importance of staying informed about local regulations to avoid unexpected financial consequences. Whether you’re in a state with a penalty or not, maintaining continuous coverage remains a prudent strategy for both financial and health security.

HealthShares and Tax: Do They Qualify as Health Insurance?

You may want to see also

Frequently asked questions

The health insurance penalty, also known as the individual shared responsibility payment, is a fee imposed on individuals who do not have qualifying health insurance coverage and do not qualify for an exemption.

The penalty is calculated in one of two ways: as a percentage of your household income or as a flat fee per person, whichever is higher. For 2023, the penalty is 2.5% of your household income or $695 per adult and $347.50 per child, up to a maximum of $2,085 per family.

The health insurance penalty is assessed on a monthly basis. If you are uninsured for only part of the year, you will only be responsible for paying the penalty for the months you were uninsured.

Yes, there are several exemptions from the health insurance penalty, including financial hardship, short coverage gaps (less than 3 months), and certain life events such as divorce or loss of coverage. You may also qualify for an exemption based on your income or if you are a member of certain religious sects.

The health insurance penalty is reported and paid when you file your federal income tax return. If you owe a penalty, you will need to complete Form 8965, Health Coverage Exemptions and Form 1095, Health Insurance Marketplace Statement, and submit them with your tax return. Note that the penalty is no longer being assessed at the federal level as of 2019, but some states have implemented their own penalties for not having health insurance.