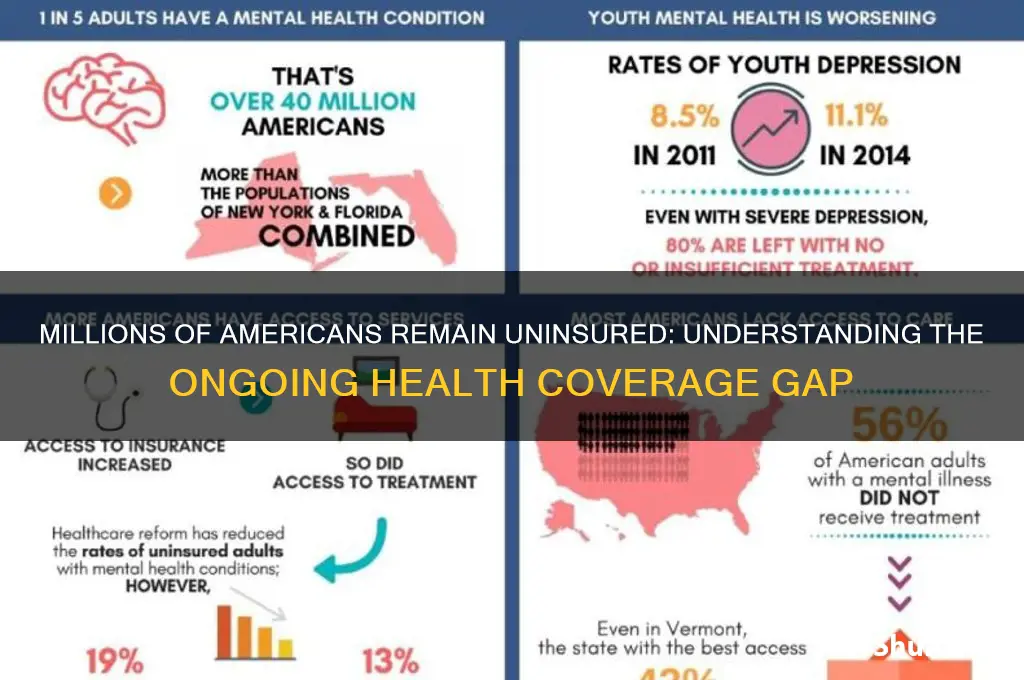

Despite significant strides in healthcare access following the Affordable Care Act, millions of Americans remain uninsured, highlighting persistent gaps in the system. As of recent data, approximately 8.5% of the U.S. population, or roughly 28 million people, lack health insurance, with disparities disproportionately affecting low-income individuals, racial and ethnic minorities, and those in states that have not expanded Medicaid. Factors such as high premiums, limited employer-sponsored coverage, and immigration status contribute to this ongoing issue, leaving many vulnerable to financial hardship and inadequate medical care. Addressing this problem requires targeted policy reforms, expanded affordability measures, and increased awareness to ensure universal access to healthcare.

Explore related products

What You'll Learn

![]()

Uninsured rates by state

As of the latest data, approximately 8.5% of Americans, or about 28 million people, remain uninsured, despite the strides made by the Affordable Care Act (ACA). This national average, however, masks significant disparities across states, with uninsured rates ranging from as low as 2.8% to as high as 14.7%. These variations are influenced by factors such as state policies, economic conditions, and demographic differences. Understanding these state-level disparities is crucial for tailoring solutions to reduce the uninsured population effectively.

Consider Texas, which leads the nation with the highest uninsured rate at 14.7%. This is largely due to the state’s decision not to expand Medicaid under the ACA, leaving a coverage gap for low-income adults who earn too much to qualify for traditional Medicaid but too little to afford private insurance. In contrast, states like Massachusetts, with an uninsured rate of 2.8%, have implemented comprehensive health reforms, including Medicaid expansion and robust state-run marketplaces, ensuring broader access to affordable coverage. This comparison highlights how policy choices directly impact uninsured rates.

For policymakers and advocates, the data underscores the need for targeted interventions. States with high uninsured rates could benefit from expanding Medicaid, increasing funding for outreach programs, and simplifying enrollment processes. For instance, in states like Oklahoma and Missouri, where Medicaid expansion was recently adopted, uninsured rates are expected to decline significantly. However, success requires addressing not just eligibility but also awareness and accessibility, as many eligible individuals remain unenrolled due to confusion or lack of information.

Individuals living in states with high uninsured rates should explore all available options, including ACA marketplace plans, employer-sponsored insurance, and short-term health plans as a temporary solution. For those in the Medicaid coverage gap, community health centers offer low-cost or sliding-scale services, though these are not a substitute for comprehensive insurance. Staying informed about policy changes, such as special enrollment periods or state-specific initiatives, can also open new pathways to coverage.

Ultimately, the patchwork of uninsured rates by state reveals both the challenges and opportunities in achieving universal health coverage. While federal policies provide a framework, state-level actions are pivotal in closing the gap. By learning from states with low uninsured rates and addressing barriers in those with high rates, the nation can move closer to ensuring that all Americans have access to affordable, quality healthcare.

Understanding Medication Costs: Insurance Billing Explained

You may want to see also

Explore related products

![]()

Impact of income on coverage

Income remains a decisive factor in determining whether Americans have health insurance, with millions still uninsured due to financial constraints. Data from the U.S. Census Bureau reveals that in 2022, approximately 8.5% of the population, or about 28 million people, lacked health coverage. Among these, low-income individuals were disproportionately affected. For instance, households earning below the federal poverty level (FPL) were nearly three times more likely to be uninsured compared to those earning above 400% of the FPL. This disparity underscores how income directly correlates with access to healthcare, as lower earnings often limit the ability to afford premiums, copays, and deductibles.

Consider the mechanics of this relationship: for a family of four earning below the FPL (around $28,000 annually), even subsidized plans under the Affordable Care Act (ACA) can consume a significant portion of their income. For example, a benchmark Silver plan might cost $200 monthly after subsidies, which equates to nearly 9% of their monthly income. This financial strain often forces low-income families to prioritize essentials like rent and food over health insurance. In contrast, higher-income households can more easily absorb these costs, leaving them with greater coverage stability.

To address this gap, policymakers and advocates must focus on targeted solutions. Expanding Medicaid in the 10 states that have not yet done so could immediately cover up to 2 million uninsured low-income adults. Additionally, increasing premium subsidies for ACA plans could make coverage more affordable for those just above the Medicaid eligibility threshold. Practical steps include raising income-based subsidy caps and simplifying enrollment processes to reduce barriers for low-income families. Without such interventions, the income-coverage divide will persist, leaving millions vulnerable to financial and health risks.

A comparative analysis highlights the success of states like California and New York, which have implemented aggressive Medicaid expansions and state-funded subsidies. These states have uninsured rates below the national average, demonstrating that income-based disparities can be mitigated through policy action. Conversely, states like Texas and Florida, with higher uninsured rates, illustrate the consequences of inaction. The takeaway is clear: income-driven coverage gaps are not inevitable but require deliberate, income-specific strategies to close.

UMC Health Insurance Application Guide: Step-by-Step Process and Tips

You may want to see also

Explore related products

![]()

Role of employment status

Employment status is a critical determinant of health insurance coverage in the United States, with millions of Americans relying on employer-sponsored plans as their primary source of healthcare access. As of recent data, approximately 28.9 million non-elderly Americans remain uninsured, and a significant portion of this population is either unemployed, underemployed, or working in jobs that do not offer health benefits. For instance, part-time workers, gig economy participants, and employees in small businesses are often excluded from employer-sponsored insurance, leaving them vulnerable to gaps in coverage. This disparity highlights the inextricable link between job stability and healthcare access, underscoring the need for policy interventions that decouple insurance from employment.

Consider the gig economy, where workers are classified as independent contractors rather than employees. Platforms like Uber, Lyft, and DoorDash employ millions, yet these workers rarely receive health benefits. A 2021 study by the Kaiser Family Foundation found that only 29% of gig workers had employer-sponsored insurance, compared to 67% of traditional full-time workers. This gap is further exacerbated by the lack of affordable alternatives, as individual marketplace plans can cost upwards of $400 per month for a single adult—a prohibitive expense for those earning low or unpredictable wages. For gig workers, securing health insurance often requires navigating complex subsidy eligibility rules under the Affordable Care Act (ACA), a process that many find daunting or inaccessible.

To address this issue, policymakers and employers can take specific steps. First, expanding Medicaid in the 10 states that have not yet done so would cover an additional 2.2 million low-income adults, many of whom are unemployed or in low-wage jobs. Second, employers could reclassify gig workers as employees, ensuring they qualify for benefits, though this would require overcoming significant legal and economic hurdles. Third, creating a public health insurance option with premiums capped at 5% of income could provide a safety net for those in precarious employment situations. For individuals, practical tips include exploring ACA subsidies, joining professional associations that offer group plans, or leveraging health savings accounts (HSAs) to offset out-of-pocket costs.

A comparative analysis of countries with universal healthcare systems reveals an alternative model. In Canada and the UK, for example, health insurance is not tied to employment, resulting in uninsured rates below 1%. While implementing such a system in the U.S. would require significant political and economic shifts, incremental reforms—like lowering the Medicaid expansion threshold or extending COBRA subsidies—could mitigate the immediate impact of employment-based disparities. The takeaway is clear: until health insurance is delinked from employment, millions of Americans will continue to face barriers to care, perpetuating health inequities that affect not only individuals but the broader economy.

Applying Insurance to 1800 Contacts: A Simple Guide

You may want to see also

Explore related products

![]()

Racial disparities in access

Despite progress in expanding health insurance coverage, racial disparities persist, leaving millions of Americans uninsured. According to the latest data from the U.S. Census Bureau, approximately 8.6% of the population, or about 28 million people, remain uninsured. Among these, Black and Hispanic individuals are disproportionately affected, with uninsured rates of 9.6% and 18.3%, respectively, compared to 5.9% for non-Hispanic whites. These disparities are not merely numbers; they reflect systemic barriers that limit access to healthcare for communities of color.

Analyzing the Root Causes

Racial disparities in health insurance access stem from a complex interplay of socioeconomic and structural factors. For instance, Black and Hispanic workers are more likely to be employed in low-wage jobs that do not offer employer-sponsored insurance, a primary source of coverage for most Americans. Additionally, states with higher minority populations are more likely to have opted out of Medicaid expansion under the Affordable Care Act, leaving millions in the "coverage gap" ineligible for both Medicaid and subsidized marketplace plans. Historical redlining and discriminatory policies have also concentrated poverty in communities of color, further limiting financial access to healthcare.

Practical Steps to Address Disparities

To close the racial gap in health insurance coverage, targeted interventions are essential. Policymakers should prioritize Medicaid expansion in the 10 remaining non-expansion states, where a disproportionate number of uninsured Black and Hispanic individuals reside. Employers can play a role by offering affordable health benefits to low-wage workers, regardless of full-time status. Community health centers should expand outreach efforts, providing culturally competent enrollment assistance in languages spoken by diverse populations. For individuals, understanding eligibility for programs like CHIP (Children’s Health Insurance Program) or subsidized marketplace plans can be a lifeline.

Comparative Perspective: Lessons from Successful Models

States like California and New York have made strides in reducing racial disparities by implementing aggressive outreach campaigns and simplifying enrollment processes. California, for example, offers subsidized coverage to undocumented immigrants, a group disproportionately represented among the uninsured. These models demonstrate that policy innovation, combined with community engagement, can significantly reduce disparities. Federally, expanding eligibility for premium tax credits and lowering the Medicaid coverage gap could further level the playing field.

The Human Cost and Urgent Need for Action

Behind the statistics are real people facing preventable health crises. Uninsured Black and Hispanic individuals are less likely to receive preventive care, leading to higher rates of chronic conditions like diabetes and hypertension. For example, Black adults are 60% more likely than white adults to be diagnosed with diabetes, yet they are less likely to have consistent access to management tools like insulin or regular check-ups. Addressing racial disparities in health insurance is not just a moral imperative but a public health necessity, as untreated conditions strain the healthcare system and deepen inequities.

Racial disparities in health insurance access are a solvable problem, but they require concerted effort across sectors. By dismantling structural barriers, expanding coverage options, and prioritizing equity in healthcare policy, we can ensure that no community is left behind. The millions of uninsured Americans deserve more than incremental change—they need transformative solutions that reflect the urgency of their situation.

A Step-by-Step Guide to Applying for Health Insurance in Connecticut

You may want to see also

Explore related products

![]()

Effects of policy changes

Policy changes aimed at expanding health insurance coverage have yielded mixed results, with millions of Americans still uninsured despite significant legislative efforts. The Affordable Care Act (ACA), for instance, reduced the uninsured rate from 16% in 2010 to 8.6% in 2016, covering approximately 20 million previously uninsured individuals. However, recent data from the U.S. Census Bureau indicates that around 29 million Americans remained uninsured in 2021. This persistence of uninsured populations highlights the limitations of policy interventions and the need for targeted adjustments to address gaps in coverage.

One critical effect of policy changes is the disproportionate impact on specific demographics. For example, states that expanded Medicaid under the ACA saw greater reductions in uninsured rates among low-income adults compared to non-expansion states. In expansion states, the uninsured rate for adults with incomes below 138% of the federal poverty level dropped to 10%, while in non-expansion states, it remained at 21%. This disparity underscores how policy decisions at the state level can either amplify or mitigate federal efforts, leaving millions in non-expansion states without access to affordable coverage.

Another consequence of policy shifts is the unintended creation of coverage gaps. The ACA’s individual mandate, which required most Americans to have health insurance or pay a penalty, was effectively eliminated in 2019 when the penalty was reduced to $0. While this change provided relief for some, it also contributed to a slight uptick in uninsured rates, particularly among younger, healthier individuals who opted out of coverage. Policymakers must balance the need for broad participation with the financial realities of individuals to avoid such gaps.

Practical steps to address these effects include enhancing outreach and education efforts to inform eligible individuals about available coverage options, such as Medicaid and ACA marketplace plans. For instance, targeted campaigns in underserved communities could increase enrollment by 15-20%, according to a Kaiser Family Foundation study. Additionally, reinstating a modified individual mandate or introducing incentives for enrollment could encourage broader participation. States could also consider adopting innovative models, like auto-enrollment programs, to streamline access and reduce administrative barriers.

Ultimately, the effects of policy changes on uninsured rates reveal a complex interplay of federal and state actions, demographic factors, and individual behavior. While progress has been made, the persistence of millions without coverage demands a nuanced approach that addresses both systemic barriers and localized challenges. By learning from past policy impacts and implementing data-driven solutions, policymakers can work toward closing the coverage gap and ensuring health insurance for all Americans.

Why Insurance Companies Insist on Seeing Injured Drivers After Accidents

You may want to see also

Frequently asked questions

As of 2023, approximately 8-10 million Americans remain uninsured, though the exact number fluctuates based on economic conditions, policy changes, and survey methodologies.

Reasons include high insurance costs, lack of employer-sponsored coverage, gaps in Medicaid eligibility in non-expansion states, and immigration status barriers.

The number has fluctuated; it decreased significantly after the Affordable Care Act (ACA) but has seen slight increases in recent years due to factors like policy changes and economic shifts.

Low-income individuals, young adults, people of color, and those living in states that did not expand Medicaid are disproportionately uninsured.

Efforts include expanding Medicaid, enhancing Affordable Care Act subsidies, promoting public awareness of available coverage options, and advocating for policy reforms to close coverage gaps.