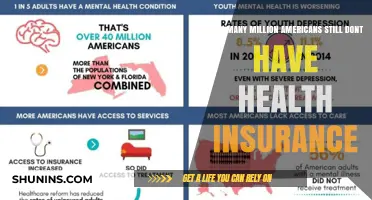

The health insurance market is a complex and dynamic landscape, with numerous insurance companies offering a wide range of policies to cater to diverse consumer needs. When considering the question of how many insurance companies sell health insurance, it's essential to recognize that the number varies significantly by region and country, as each has its own regulatory framework and market conditions. In the United States, for example, there are hundreds of health insurance providers, including national giants like UnitedHealth Group, Anthem, and Aetna, as well as regional and local insurers. Globally, the number is even more extensive, with thousands of companies participating in the health insurance sector, each adapting their offerings to comply with local laws and meet the specific health care demands of their target populations. This diversity in providers ensures competitive pricing and a variety of coverage options but also complicates the decision-making process for consumers seeking the best policy for their individual or family needs.

Explore related products

What You'll Learn

![]()

Major National Insurers Offering Health Plans

In the United States, the health insurance landscape is dominated by a handful of major national insurers that collectively cover millions of Americans. These companies—UnitedHealth Group, Anthem, Aetna, Cigna, and Humana—are the titans of the industry, offering a wide array of health plans tailored to diverse needs. Each insurer operates across multiple states, providing individual, family, and employer-sponsored plans, as well as Medicare and Medicaid options. Their scale allows them to negotiate lower rates with healthcare providers, which can translate to cost savings for policyholders. However, their dominance also raises questions about market competition and consumer choice.

Analyzing their offerings reveals distinct strategies. UnitedHealth Group, the largest by revenue, stands out for its integrated approach, combining insurance with healthcare services through its Optum division. This vertical integration enables them to manage care more efficiently, potentially reducing costs for chronic conditions like diabetes or hypertension. Anthem, on the other hand, focuses on localized plans, leveraging its regional subsidiaries to cater to specific state regulations and demographics. For instance, their Blue Cross Blue Shield plans often include state-specific benefits, such as expanded mental health coverage in California or enhanced maternity care in New York.

For consumers, choosing among these insurers requires careful consideration of plan details. Aetna, for example, is known for its robust provider networks, making it a strong choice for those who prioritize access to a wide range of doctors and specialists. Cigna, meanwhile, excels in global health plans, ideal for expatriates or frequent travelers. Humana specializes in Medicare Advantage plans, offering additional benefits like dental, vision, and fitness programs for seniors. Each insurer’s strengths align with specific consumer profiles, so evaluating your healthcare needs—whether it’s frequent specialist visits, prescription drug coverage, or preventive care—is crucial.

A comparative analysis highlights the importance of plan customization. While all major insurers offer standard HMO and PPO plans, their add-ons and riders differ significantly. For instance, UnitedHealth’s “Rally” digital health platform provides personalized wellness programs, while Anthem’s “LiveHealth Online” offers virtual doctor visits. Cigna’s “Healthy Rewards” program incentivizes healthy behaviors with gift cards or discounts, and Humana’s “SilverSneakers” program provides gym memberships for seniors. These value-added features can enhance overall health outcomes but may come with higher premiums, so weigh the benefits against your budget.

Finally, navigating the enrollment process requires attention to detail. Open enrollment periods, typically in the fall, are the primary time to purchase individual plans, though qualifying life events (e.g., marriage, job loss) allow for special enrollment. Employer-sponsored plans often have different timelines, so consult your HR department. When comparing plans, use the insurer’s online tools to estimate out-of-pocket costs for your expected healthcare usage. For example, if you take a $100 monthly prescription, calculate the annual cost under each plan’s formulary. Additionally, check provider directories to ensure your preferred doctors are in-network, as out-of-network care can significantly increase costs. By leveraging these strategies, you can select a plan from a major national insurer that aligns with your health and financial needs.

Understanding LOB in Medical Insurance: What Does It Mean?

You may want to see also

Explore related products

$63.52 $245.95

![]()

Regional Health Insurance Providers Comparison

The health insurance landscape is fragmented, with thousands of providers operating across the United States alone. However, when comparing regional health insurance providers, the focus shifts from sheer numbers to the nuances of coverage, cost, and customer service that vary by geographic area. For instance, in the Northeast, providers like Blue Cross Blue Shield and Aetna dominate, offering extensive networks and specialized plans tailored to urban populations. In contrast, Southern states often feature more localized providers, such as Florida Blue or Ambetter, which cater to rural and suburban communities with cost-effective options.

Analyzing regional providers requires understanding the unique healthcare needs of each area. In the Midwest, where chronic conditions like diabetes and heart disease are prevalent, insurers like Health Alliance and Medica often include preventive care benefits and wellness programs. Out West, providers such as Kaiser Permanente and Molina Healthcare emphasize integrated care models, leveraging technology to improve access in sprawling, less populated regions. A key takeaway is that regional providers align their offerings with local demographics, making it essential to compare plans based on specific health needs and lifestyle factors.

For consumers, the comparison process should start with evaluating network coverage. Regional providers often have stronger relationships with local hospitals and specialists, which can translate to lower out-of-pocket costs. For example, in the Southeast, providers like UnitedHealthcare and Cigna offer tiered networks, where staying within their preferred providers significantly reduces expenses. However, this can limit flexibility, so individuals should weigh the trade-offs between cost savings and provider choice. Practical tip: Use provider directories to verify if your preferred doctors and hospitals are in-network before enrolling.

Another critical factor is the cost structure, which varies widely by region. Premiums in high-cost-of-living areas like California or New York tend to be higher, but regional providers may offset this with subsidies or state-specific programs. For instance, New York’s Essential Plan offers low-cost coverage to individuals earning up to 200% of the federal poverty level. In contrast, Texas-based providers like Community Health Choice focus on affordable plans for low-income families. When comparing, consider not just premiums but also deductibles, copays, and out-of-pocket maximums to determine the best value.

Finally, customer service and satisfaction ratings should not be overlooked. Regional providers often outperform national competitors in localized support, as they have a deeper understanding of state-specific regulations and community needs. For example, PacificSource in the Northwest is consistently rated highly for its responsive customer service and claims processing. To make an informed decision, check reviews on platforms like J.D. Power or the National Committee for Quality Assurance (NCQA). Practical tip: Prioritize providers with high ratings in areas that matter most to you, whether it’s claims handling, customer support, or digital tools.

In summary, comparing regional health insurance providers involves more than just counting how many exist. It requires a targeted approach, considering local healthcare needs, network coverage, cost structures, and customer service. By focusing on these specifics, consumers can select a plan that not only fits their budget but also provides the care they need in their region.

Understanding Medical Expenses: Insurance Deductibles and Tax Deductions

You may want to see also

Explore related products

![]()

Online-Only Health Insurance Companies Overview

The rise of online-only health insurance companies has disrupted the traditional insurance landscape, offering consumers a streamlined, digital-first alternative to brick-and-mortar providers. These companies, often referred to as insurtechs, leverage technology to simplify the purchasing process, reduce overhead costs, and provide personalized plans. For instance, companies like Oscar Health and Bright Health Group have gained traction by offering user-friendly platforms, transparent pricing, and integrated telehealth services. This shift reflects a broader trend toward digital health solutions, particularly among tech-savvy consumers who prioritize convenience and accessibility.

Analyzing the business model of online-only insurers reveals their competitive edge. By eliminating physical offices and relying on digital infrastructure, these companies can offer lower premiums while maintaining profitability. For example, Lemonade, initially known for renters and homeowners insurance, expanded into health insurance with a focus on AI-driven claims processing and instant policy issuance. This efficiency not only reduces costs but also enhances customer satisfaction through faster service. However, the lack of in-person support may be a drawback for individuals who prefer face-to-face interactions or require assistance navigating complex policies.

From a consumer perspective, choosing an online-only health insurance company requires careful consideration. Prospective buyers should evaluate the provider’s network size, as some digital insurers may have limited partnerships with healthcare providers. Additionally, understanding the scope of coverage is crucial, especially for specialized care or pre-existing conditions. For instance, while many online insurers offer comprehensive plans, some may exclude certain treatments or require higher out-of-pocket costs. Practical tips include reading customer reviews, comparing telehealth options, and verifying the company’s regulatory compliance to ensure reliability.

Comparatively, online-only insurers often excel in catering to younger, healthier demographics who seek affordable, no-frills plans. For example, companies like Clover Health target seniors with tech-enabled Medicare Advantage plans, while others focus on individual or family coverage. In contrast, traditional insurers may offer more extensive networks and specialized plans but at a higher cost. The takeaway is that online-only options are ideal for those comfortable with digital tools and willing to trade some flexibility for cost savings. However, individuals with complex health needs or preferences for established brands may find traditional insurers more suitable.

To maximize the benefits of online-only health insurance, consumers should adopt proactive strategies. Regularly updating personal health information on the platform ensures accurate premium calculations and tailored plan recommendations. Leveraging integrated telehealth services can provide convenient access to care, particularly for minor ailments or routine consultations. Additionally, staying informed about policy changes and utilizing digital tools for claims submission can streamline the insurance experience. By embracing these practices, policyholders can fully capitalize on the efficiency and affordability that online-only insurers offer.

Understanding the Role of a Financial Advisor in Insurance Companies

You may want to see also

Explore related products

$26.77

![]()

Specialized Health Insurance for Specific Groups

Specialized health insurance plans are increasingly tailored to meet the unique needs of specific demographic, occupational, or health-condition groups. For instance, athletes often require policies covering sports-related injuries, while freelancers seek plans with flexible premiums and comprehensive outpatient care. These niche offerings reflect a shift from one-size-fits-all models to targeted solutions, addressing gaps in traditional health insurance. By focusing on specific groups, insurers can provide more relevant coverage, reducing out-of-pocket costs for policyholders and improving overall health outcomes.

Consider occupational groups like firefighters or miners, who face higher risks of respiratory diseases or musculoskeletal injuries. Specialized plans for these professions often include enhanced coverage for preventive screenings, rehabilitation services, and mental health support. For example, a firefighter’s policy might cover annual lung function tests and PTSD counseling, while a miner’s plan could include physical therapy benefits and hearing loss treatments. These tailored features ensure that high-risk workers receive proactive care, minimizing long-term health complications.

Age-specific plans are another growing segment, particularly for seniors and young adults. Seniors may opt for policies with higher prescription drug coverage limits, in-home care benefits, and chronic disease management programs. Conversely, young adults might prioritize plans with lower premiums, telehealth access, and wellness incentives like gym memberships or mental health apps. For instance, a 65-year-old with diabetes could benefit from a plan covering insulin pumps and nutritionist consultations, while a 25-year-old freelancer might choose a policy with discounted therapy sessions and fitness trackers.

Chronic condition-specific insurance is also gaining traction, catering to individuals with diabetes, cancer, or autoimmune disorders. These plans often include specialized medications, frequent specialist visits, and disease management tools. For example, a diabetes-specific policy might cover continuous glucose monitors (CGMs), insulin supplies, and annual eye exams to prevent retinopathy. Similarly, cancer-specific plans may offer access to experimental treatments, genetic testing, and survivorship care. Such targeted coverage ensures that individuals with complex health needs receive comprehensive support without financial strain.

When evaluating specialized health insurance, it’s crucial to assess the plan’s network of providers, exclusions, and out-of-pocket limits. For instance, a plan for mental health professionals might offer extensive coverage for therapy sessions but exclude certain alternative treatments. Always compare premiums, deductibles, and co-pays against your anticipated healthcare usage. Practical tips include checking for rider options (e.g., maternity coverage for young professionals) and verifying if pre-existing conditions are covered. By aligning the plan’s features with your specific needs, you can maximize benefits while minimizing costs.

Managing High Blood Pressure: Can Insurance Deny You?

You may want to see also

Explore related products

$9.97

$8.27 $12.99

![]()

Number of Insurers by State Regulations

The number of health insurance companies operating within a state is not merely a matter of market competition but a direct reflection of regulatory environments. States with fewer regulatory barriers, such as streamlined licensing processes and flexible benefit mandates, tend to attract more insurers. For instance, Texas, known for its business-friendly policies, hosts over 100 health insurance providers, while highly regulated states like New York have fewer than 30. This disparity underscores how state-specific rules shape market entry and consumer choice.

Consider the role of state-mandated benefits, which require insurers to cover specific services, such as maternity care or mental health treatment. While these mandates protect consumers, they also increase operational costs for insurers. In California, for example, over 50 mandated benefits contribute to higher premiums and fewer insurers willing to compete. Conversely, states like Wyoming, with fewer than 10 mandates, often see a broader range of insurers offering more affordable plans. Understanding these trade-offs is crucial for policymakers aiming to balance consumer protection and market accessibility.

Another critical factor is the state’s approach to rate regulation. States with strict rate review processes, like Oregon, often limit insurer profitability, discouraging new entrants. In contrast, states like Florida, which allow insurers more flexibility in setting premiums, attract a larger number of competitors. This dynamic highlights the need for a nuanced approach to regulation—one that ensures fair pricing without stifling market participation. For consumers, this means that the number of available insurers can directly impact the cost and variety of health plans.

Practical tips for navigating this landscape include researching your state’s regulatory environment before purchasing health insurance. Tools like the Kaiser Family Foundation’s state health facts database provide insights into local mandates and insurer participation. Additionally, consider consulting a broker who specializes in your state’s market, as they can identify lesser-known insurers offering competitive rates. Finally, advocate for balanced regulations that encourage competition without compromising essential protections, ensuring a healthier insurance market for all.

Understanding Medicare: How It Differs From Regular Insurance

You may want to see also

Frequently asked questions

There are over 900 health insurance companies operating in the United States, ranging from large national providers to smaller regional carriers.

No, not all insurance companies sell health insurance. Many specialize in other areas like auto, home, or life insurance, while others focus exclusively on health coverage.

The U.S. health insurance market is dominated by about 10 major companies, including UnitedHealth Group, Anthem, Aetna, and Humana, which collectively hold a significant share of the market.

Yes, some companies, like Oscar Health and Bright Health, focus solely on providing health insurance products and do not offer other types of insurance.

The number varies by state, but on average, most states have between 2 to 5 health insurance companies offering plans on the ACA Marketplace, with some states having more or fewer options.