Before the implementation of the Affordable Care Act (ACA), commonly known as Obamacare, millions of Americans struggled to afford health insurance due to high costs, pre-existing condition exclusions, and limited access to employer-sponsored plans. In 2010, approximately 48 million people, or about 16% of the U.S. population, were uninsured, with many unable to secure coverage due to financial barriers. Low-income individuals, part-time workers, and those with chronic health conditions were disproportionately affected, often facing unaffordable premiums or outright denials from insurers. The ACA aimed to address these disparities by expanding Medicaid, creating health insurance marketplaces, and implementing subsidies to make coverage more accessible and affordable for millions of previously uninsured Americans.

| Characteristics | Values |

|---|---|

| Year | 2010 (pre-ACA implementation) |

| Number of Uninsured Individuals (Total) | Approximately 48.6 million |

| Percentage of Population Uninsured | 16.3% |

| Uninsured by Age Group | - 18-24: 27.9% - 25-34: 28.4% - 35-44: 18.3% - 45-54: 14.3% - 55-64: 10.8% |

| Uninsured by Income Level | - Below 138% FPL: 30.6% - 138-250% FPL: 24.5% - Above 250% FPL: 8.9% |

| Uninsured by Race/Ethnicity | - Hispanic: 32.4% - Black: 20.8% - White: 12.4% - Asian: 17.0% |

| Uninsured by Employment Status | - Part-time workers: 28.9% - Self-employed: 21.3% - Unemployed: 27.6% |

| Uninsured by State | Ranged from 8.5% (Massachusetts) to 24.6% (Texas) |

| Primary Reason for Being Uninsured | Cost of insurance (majority) |

Explore related products

What You'll Learn

- Uninsured rates by income: Lower-income individuals faced higher uninsured rates pre-Obamacare due to cost barriers

- Uninsured rates by age: Young adults were disproportionately uninsured before ACA due to limited employer coverage

- Uninsured rates by state: Southern and Western states had higher uninsured populations pre-ACA due to policy differences

- Impact on minorities: Racial and ethnic minorities faced higher uninsured rates due to systemic disparities pre-Obamacare

- Uninsured with pre-existing conditions: Millions lacked coverage pre-ACA due to denials for pre-existing health conditions

![]()

Uninsured rates by income: Lower-income individuals faced higher uninsured rates pre-Obamacare due to cost barriers

Before the Affordable Care Act (ACA), commonly known as Obamacare, took effect, the disparity in uninsured rates among different income groups was stark. Data from the U.S. Census Bureau reveals that in 2010, approximately 29.8% of individuals in households earning below $25,000 annually were uninsured, compared to just 8.9% of those in households earning $75,000 or more. This gap underscores a critical issue: lower-income individuals faced significantly higher barriers to accessing health insurance, primarily due to cost. For many in this demographic, the choice between paying for health insurance and covering basic necessities like rent, food, or utilities was a harsh reality.

The cost of health insurance pre-ACA was prohibitive for lower-income families, who often lacked employer-sponsored coverage or access to affordable plans. For instance, a family of four earning $24,000 annually would have struggled to afford a private plan that averaged $13,770 in 2010, according to the Kaiser Family Foundation. Even with subsidies or assistance programs, the out-of-pocket costs, including deductibles and copays, remained out of reach for many. This financial strain forced lower-income individuals to either forgo insurance entirely or rely on sporadic, inadequate care, exacerbating health disparities.

To illustrate, consider a single parent working a minimum-wage job, earning roughly $15,000 a year. Pre-ACA, this individual would likely fall into a coverage gap, earning too much to qualify for Medicaid in many states but too little to afford private insurance. Without access to affordable options, they would often delay or avoid medical care, leading to untreated conditions and higher long-term costs for both the individual and the healthcare system. This cycle of inaccessibility and delayed care disproportionately affected lower-income populations, widening the health equity gap.

Addressing this issue requires understanding the systemic barriers lower-income individuals faced. The ACA’s expansion of Medicaid and introduction of subsidized marketplace plans aimed to bridge this gap, but pre-ACA, such solutions were largely absent. Practical steps to mitigate these challenges included advocating for policy changes, expanding community health programs, and increasing awareness of available resources. However, without structural reforms, the cost barrier remained insurmountable for millions, highlighting the necessity of comprehensive healthcare legislation like the ACA.

In conclusion, the pre-ACA era exposed a glaring inequality in uninsured rates, with lower-income individuals bearing the brunt of cost barriers. This disparity was not merely a statistical anomaly but a reflection of deeper systemic issues in healthcare accessibility. By examining these trends, it becomes clear that affordable, inclusive policies are essential to ensuring that financial constraints do not dictate one’s ability to access essential healthcare. The ACA marked a pivotal step toward addressing this inequity, but understanding the pre-existing challenges remains crucial for ongoing efforts to improve healthcare access for all.

Jobs Report, Health Insurance, and IRS: What You Need to Know

You may want to see also

Explore related products

![]()

Uninsured rates by age: Young adults were disproportionately uninsured before ACA due to limited employer coverage

Before the Affordable Care Act (ACA), young adults aged 19 to 25 faced a stark reality: they were nearly twice as likely to be uninsured compared to the general population. This disparity wasn’t random. Many in this age group were caught in a coverage gap—too old for dependent coverage under a parent’s plan but often in entry-level jobs that didn’t offer health benefits. For example, in 2010, nearly 30% of young adults lacked insurance, compared to 18% of the overall population. This vulnerability wasn’t just a statistic; it translated to delayed care, untreated illnesses, and financial strain for millions.

The root of this issue lay in the structure of employer-based insurance, which dominated the U.S. system pre-ACA. Young adults were overrepresented in part-time, gig, or low-wage jobs—sectors where health benefits were rare. Even when offered, these plans were often unaffordable on entry-level salaries. Without access to employer coverage, many turned to the individual market, where premiums were prohibitively expensive or policies excluded pre-existing conditions. This left young adults with few options, forcing them to gamble on their health or forgo coverage entirely.

The ACA addressed this crisis directly by allowing young adults to stay on their parents’ insurance until age 26. This single provision reduced the uninsured rate among 19- to 25-year-olds by nearly half within five years of implementation. Beyond this, the ACA’s expansion of Medicaid and creation of health insurance marketplaces offered additional pathways to coverage. For instance, a 22-year-old earning $25,000 annually could qualify for premium tax credits, slashing monthly costs from $200 to as low as $50 in some cases.

However, the pre-ACA era highlights a critical lesson: age-based disparities in insurance aren’t just numbers—they reflect systemic gaps in how coverage is structured. Young adults, often healthy but financially precarious, were disproportionately penalized by a system reliant on employer-sponsored plans. The ACA’s reforms didn’t just expand coverage; they redefined who had access to it, ensuring that age no longer dictated one’s ability to afford care. This shift underscores the importance of policies that address demographic vulnerabilities, not just broad population needs.

Teachers' Medical Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

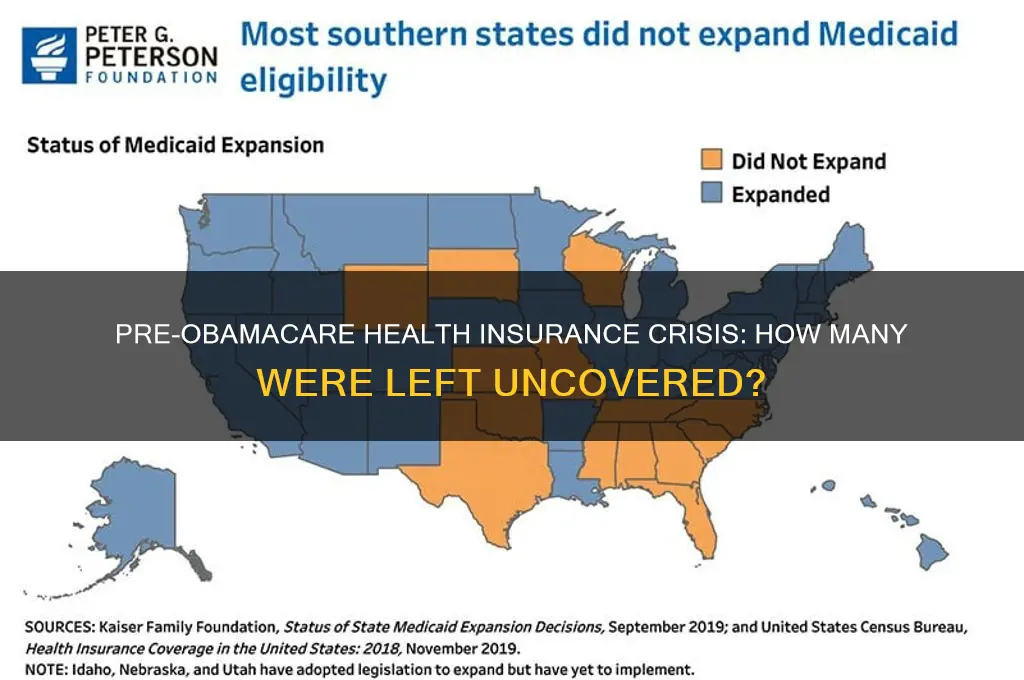

Uninsured rates by state: Southern and Western states had higher uninsured populations pre-ACA due to policy differences

Before the Affordable Care Act (ACA), commonly known as Obamacare, was implemented, the United States faced significant disparities in health insurance coverage, with Southern and Western states consistently reporting higher uninsured rates compared to their Northern and Eastern counterparts. This geographical divide was not merely coincidental but deeply rooted in policy differences that shaped access to healthcare. For instance, in 2010, Texas had an uninsured rate of 24.6%, while Massachusetts, which had already implemented state-level reforms, stood at 4.4%. These numbers highlight the stark contrast in policy approaches and their outcomes.

One key factor contributing to higher uninsured rates in Southern and Western states was their reluctance to expand Medicaid programs prior to the ACA. States like Texas, Florida, and Georgia, which later opted out of Medicaid expansion under the ACA, historically maintained stricter eligibility criteria, leaving millions of low-income residents without coverage. In contrast, states like New York and Vermont had more expansive Medicaid programs, ensuring broader access to healthcare for their populations. This policy divergence created a clear divide in uninsured rates, with Southern and Western states bearing the brunt of the crisis.

Another critical aspect was the ideological stance of state governments toward healthcare regulation. Southern and Western states, often characterized by conservative leadership, tended to favor limited government intervention in healthcare. This approach resulted in fewer state-funded health programs and less aggressive outreach to enroll eligible individuals in existing programs. For example, in 2013, Mississippi had an uninsured rate of 18.7%, while Vermont’s was 7.6%. The disparity reflects not just economic differences but also the political priorities that shaped healthcare policies in these regions.

The impact of these policy differences was particularly severe for specific demographics. In Southern and Western states, young adults, racial minorities, and part-time workers were disproportionately uninsured. For instance, in 2010, 32% of Hispanics in Texas lacked health insurance, compared to 14% of non-Hispanic whites. These disparities underscore how state-level policies exacerbated inequities in access to healthcare. The ACA’s implementation aimed to address these gaps, but the pre-existing policy landscape in these regions created a steep uphill battle.

To address these disparities, stakeholders must recognize the role of state-level policies in shaping uninsured rates. Advocates for healthcare reform can use pre-ACA data to highlight the success of progressive policies in states like Massachusetts and Vermont, urging Southern and Western states to adopt similar measures. Additionally, targeted outreach programs can help bridge the gap by educating underserved populations about available resources. While the ACA has made significant strides, understanding the historical policy differences provides a roadmap for further reducing uninsured rates in these regions.

Understanding Lifetime Caps on Health Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Impact on minorities: Racial and ethnic minorities faced higher uninsured rates due to systemic disparities pre-Obamacare

Before the Affordable Care Act (ACA), commonly known as Obamacare, racial and ethnic minorities in the United States faced disproportionately higher uninsured rates, a stark reflection of systemic disparities deeply embedded in the healthcare system. Data from the Kaiser Family Foundation reveals that in 2010, approximately 33% of Hispanics, 21% of African Americans, and 20% of Native Americans were uninsured, compared to 11% of non-Hispanic whites. These disparities were not merely coincidental but rooted in structural inequalities that limited access to affordable healthcare, stable employment with benefits, and geographic availability of healthcare services.

To understand the impact, consider the intersection of income, employment, and healthcare access. Racial and ethnic minorities are more likely to work in low-wage jobs that do not offer employer-sponsored health insurance, a primary source of coverage pre-ACA. For instance, in 2010, only 38% of Hispanic workers and 45% of Black workers had employer-based insurance, compared to 60% of white workers. This gap was further exacerbated by higher poverty rates among minorities, making private insurance unaffordable. Without the ACA’s expansions, such as Medicaid and subsidized marketplace plans, millions in these communities remained locked out of the healthcare system.

The consequences of these disparities were dire. Uninsured minorities faced delayed or forgone care, leading to poorer health outcomes and higher mortality rates for preventable conditions. For example, Black Americans were twice as likely to die from diabetes as their white counterparts, a disparity linked to lack of access to consistent care. Similarly, Hispanic women were less likely to receive mammograms, contributing to later-stage breast cancer diagnoses. These health inequities were not just individual tragedies but also economic burdens, as untreated conditions often led to costlier emergency care.

Addressing these disparities required more than just expanding coverage—it demanded targeted interventions. The ACA’s Medicaid expansion, for instance, disproportionately benefited minorities, reducing the uninsured rate among Hispanics by 15 percentage points and among Blacks by 10 percentage points between 2013 and 2016. However, states that opted out of Medicaid expansion saw significantly smaller gains, particularly in the South, where a large share of uninsured minorities resided. This highlights the importance of policy implementation in bridging systemic gaps.

In practical terms, advocates and policymakers must continue to address the root causes of these disparities. This includes enforcing anti-discrimination policies in healthcare, increasing cultural competency among providers, and expanding community health centers in underserved areas. For individuals, understanding eligibility for ACA subsidies or Medicaid can be a lifeline. Tools like the Healthcare.gov calculator can help determine affordability, while local health departments often provide enrollment assistance. The ACA was a step forward, but ensuring equitable access remains an ongoing battle.

Best Insurance Companies Offering Photographer Packages for Creative Professionals

You may want to see also

Explore related products

![]()

Uninsured with pre-existing conditions: Millions lacked coverage pre-ACA due to denials for pre-existing health conditions

Before the Affordable Care Act (ACA), millions of Americans faced a harsh reality: being denied health insurance simply because they had a pre-existing condition. This wasn't just a bureaucratic hurdle; it was a life-altering barrier. Imagine being told you couldn't get coverage because you had asthma, diabetes, or even a history of cancer. For these individuals, a pre-existing condition wasn't just a medical term – it was a scarlet letter, branding them as uninsurable.

Statistics paint a grim picture. A 2010 report by the Commonwealth Fund estimated that up to 52 million Americans under age 65 had pre-existing conditions that could make them ineligible for individual health insurance. This wasn't a small, niche problem; it affected roughly one in five non-elderly adults.

The consequences were devastating. People delayed necessary care, skipped medications, and faced crippling medical debt. A pre-existing condition could mean choosing between putting food on the table and getting a life-saving treatment. This wasn't just about numbers; it was about human lives being compromised due to a flawed system.

The ACA's prohibition on denying coverage based on pre-existing conditions was a game-changer. It wasn't just policy; it was a moral imperative, ensuring that health insurance wasn't a privilege reserved for the perfectly healthy.

Consider Sarah, a 35-year-old with Type 1 diabetes. Before the ACA, she was denied individual coverage repeatedly, forcing her to rely on a high-deductible plan through her employer. One hospitalization for diabetic ketoacidosis left her with $20,000 in debt. Post-ACA, Sarah finally secured comprehensive coverage, allowing her to manage her condition without the constant fear of financial ruin. Sarah's story isn't unique; it's a testament to the millions who gained access to care thanks to the ACA's protections.

Who Manages Process Serving in Insurance Companies: Key Roles Explained

You may want to see also

Frequently asked questions

Before the Affordable Care Act (ACA) was implemented in 2010, approximately 48 million non-elderly Americans were uninsured in 2010, according to the U.S. Census Bureau.

Prior to Obamacare, about 16.3% of the non-elderly U.S. population lacked health insurance in 2010, as reported by the Centers for Disease Control and Prevention (CDC).

Yes, the number of uninsured Americans varied significantly by state before the ACA. States like Texas and Florida had higher uninsured rates (around 25-30%), while states like Massachusetts had lower rates (around 5%) due to earlier state-level reforms.

Before Obamacare, low-income individuals were disproportionately affected by lack of insurance. Approximately 28% of people with incomes below the federal poverty level were uninsured in 2010, compared to 8% of those with incomes at or above 400% of the poverty level.

Yes, specific demographic groups were more likely to be uninsured before the ACA. These included young adults (ages 19-25), racial and ethnic minorities (e.g., Hispanics and Native Americans), and individuals working in low-wage jobs without employer-sponsored insurance.