In the United States, millions of individuals are responsible for selecting their own health insurance, a task that can be both daunting and complex. This includes self-employed workers, freelancers, and those whose employers do not offer group health plans, as well as individuals who purchase coverage through the Health Insurance Marketplace established by the Affordable Care Act. Additionally, with the rise of gig economy jobs and changing employment landscapes, more people are finding themselves in situations where they must navigate the intricacies of health insurance independently. Understanding the number of people in this position highlights the importance of accessible information, transparent pricing, and user-friendly tools to help individuals make informed decisions about their healthcare coverage.

| Characteristics | Values |

|---|---|

| Total U.S. Population (2023) | ~333.3 million |

| Percentage with Health Insurance (2022) | 91.7% |

| Number of People with Health Insurance (2022) | ~305.7 million |

| Percentage with Private Health Insurance (2022) | 65.6% |

| Number of People with Private Health Insurance (2022) | ~215.5 million |

| Percentage with Employer-Sponsored Insurance (ESI) (2022) | 54.4% |

| Number of People with ESI (2022) | ~166.3 million |

| Percentage with Non-Group (Individual) Private Insurance (2022) | 9.6% |

| Number of People with Individual Private Insurance (2022) | ~31.3 million |

| Percentage with Medicaid (2022) | 18.9% |

| Number of People with Medicaid (2022) | ~62.7 million |

| Percentage with Medicare (2022) | 18.4% |

| Number of People with Medicare (2022) | ~61.2 million |

| Uninsured Rate (2022) | 8.3% |

| Number of Uninsured People (2022) | ~27.6 million |

| Note: | People with individual private insurance are more likely to have chosen their own health insurance plans, either through the Affordable Care Act (ACA) marketplaces or directly from insurers. |

Explore related products

What You'll Learn

![]()

Factors influencing individual health insurance choices

In the United States, approximately 14% of the population, or around 46 million people, purchase their own health insurance, often through the individual market or health insurance exchanges. This figure highlights the significant number of individuals who must navigate the complex landscape of health insurance choices independently. The decision-making process is influenced by a myriad of factors, each playing a critical role in determining the most suitable coverage. Understanding these factors can empower individuals to make informed choices that align with their health needs and financial circumstances.

Cost and Affordability: The Primary Determinant

The single most influential factor in individual health insurance choices is cost. Premiums, deductibles, copayments, and out-of-pocket maximums vary widely across plans, and individuals must balance these expenses against their budget. For example, a Bronze plan may have lower monthly premiums but higher deductibles, making it suitable for healthy individuals who rarely visit the doctor. Conversely, a Gold plan with higher premiums but lower out-of-pocket costs may be preferable for those with chronic conditions or frequent medical needs. Practical tip: Use online calculators to estimate annual healthcare expenses under different plans, factoring in expected medical usage and prescription drug costs.

Coverage Needs: Tailoring Plans to Health Status

Health status and anticipated medical needs significantly shape insurance choices. Young, healthy adults may prioritize catastrophic coverage plans, which offer minimal benefits but protect against major medical expenses. In contrast, older adults or those with pre-existing conditions often seek comprehensive plans that include specialist visits, prescription drug coverage, and preventive care. For instance, a 55-year-old with diabetes would benefit from a plan that covers insulin and regular endocrinologist visits. Caution: Avoid underestimating future health needs; unexpected illnesses or accidents can lead to financial strain without adequate coverage.

Provider Networks: Access to Preferred Care

The availability of preferred doctors, hospitals, and specialists within a plan’s network is another critical factor. Health Maintenance Organizations (HMOs) typically require in-network care and referrals for specialists, while Preferred Provider Organizations (PPOs) offer more flexibility but at a higher cost. For individuals with established relationships with specific healthcare providers, verifying network inclusion is essential. Example: A patient with a rare condition may need a plan that includes access to a specialized treatment center, even if it means paying higher premiums.

Plan Type and Flexibility: Balancing Structure and Choice

The type of insurance plan—HMO, PPO, EPO, or POS—impacts both cost and flexibility. HMOs are generally more affordable but restrictive, while PPOs offer greater freedom to see out-of-network providers at an additional cost. Exclusive Provider Organizations (EPOs) combine elements of HMOs and PPOs, often excluding out-of-network coverage altogether. Step-by-step advice: List your preferred providers and compare their inclusion across different plan types. Weigh the importance of flexibility against potential cost savings to determine the best fit.

Government Subsidies and Marketplaces: Leveraging Financial Assistance

For many individuals, government subsidies through the Affordable Care Act (ACA) marketplaces significantly influence insurance choices. Premium tax credits and cost-sharing reductions can make higher-tier plans more affordable for eligible individuals and families. For example, a family of four earning up to $106,000 annually may qualify for subsidies in 2023. Practical tip: Use the marketplace’s subsidy calculator to estimate eligibility and apply these savings when comparing plans.

In conclusion, choosing individual health insurance is a multifaceted decision shaped by cost, health needs, provider access, plan structure, and available subsidies. By carefully evaluating these factors and leveraging available tools, individuals can select coverage that provides both financial protection and access to necessary care.

Why Companies Delay Insurance Claims: Uncovering the Wait Time Mystery

You may want to see also

Explore related products

![]()

Cost considerations in selecting health insurance plans

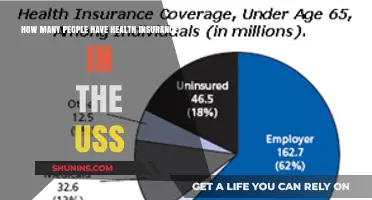

In the United States, approximately 158 million people rely on employer-sponsored health insurance, leaving about 55 million individuals to navigate the complex task of choosing their own plans. This group includes self-employed workers, freelancers, early retirees, and those without access to employer coverage. For these individuals, cost considerations are paramount, as they must balance premiums, deductibles, copays, and out-of-pocket maximums without the subsidy of an employer. Understanding these financial components is critical to selecting a plan that provides adequate coverage without breaking the bank.

Consider the premium—the monthly fee for maintaining coverage—as the foundation of your cost analysis. While lower premiums may seem attractive, they often come with higher deductibles, which is the amount you pay out of pocket before insurance kicks in. For example, a plan with a $200 monthly premium and a $6,000 deductible may save you money if you’re healthy but could lead to financial strain if you require unexpected medical care. Conversely, a plan with a $500 monthly premium and a $1,000 deductible offers more predictable costs for frequent healthcare users. Evaluate your health history and anticipated needs to determine the optimal balance.

Beyond premiums and deductibles, examine copays and coinsurance, which dictate your share of costs for specific services. A plan with a $30 copay for doctor visits and 20% coinsurance for hospital stays might be suitable for someone with manageable health conditions. However, if you have chronic illnesses requiring frequent specialist visits or prescriptions, look for plans with lower copays or capped specialty drug costs. For instance, some plans offer $0 copays for generic medications, which can save hundreds of dollars annually for individuals on long-term therapies.

Out-of-pocket maximums are another critical factor, as they cap your total annual expenses for covered services. Plans with lower out-of-pocket maximums, such as $5,000, provide financial protection but typically come with higher premiums. For a 30-year-old with no dependents, a plan with a $7,000 out-of-pocket maximum might be a reasonable trade-off for lower monthly costs. However, families or individuals with higher health risks may prioritize plans with $4,000 or lower caps to mitigate catastrophic expenses.

Finally, leverage available tools and resources to simplify your decision-making process. Use online calculators to estimate annual costs based on your expected healthcare usage. Compare plans side by side on marketplaces like Healthcare.gov, paying attention to provider networks and prescription drug coverage. If you’re eligible, consider Health Savings Accounts (HSAs) paired with high-deductible plans, which offer tax advantages and flexibility for long-term savings. By meticulously weighing these cost considerations, you can select a health insurance plan that aligns with your financial and medical needs.

Medical Residents: Understanding Their Health Insurance Options

You may want to see also

Explore related products

![]()

Understanding health insurance policy coverage options

In the United States, approximately 158 million people rely on employer-sponsored health insurance, leaving about 55 million individuals to navigate the complex task of choosing their own coverage. This group includes self-employed workers, freelancers, early retirees, and those who don’t qualify for employer plans. For these individuals, understanding health insurance policy coverage options isn’t just a choice—it’s a necessity. The marketplace offers a dizzying array of plans, each with unique benefits, costs, and limitations. Without a clear grasp of these options, one risks overpaying, underinsuring, or missing critical coverage altogether.

Consider the core types of health insurance plans: HMOs, PPOs, EPOs, and HDHPs. Each operates differently, from provider networks to out-of-pocket costs. For instance, an HMO (Health Maintenance Organization) typically requires selecting a primary care physician and obtaining referrals for specialists, making it ideal for those who prioritize lower premiums and don’t mind restricted flexibility. In contrast, a PPO (Preferred Provider Organization) offers more freedom to see out-of-network providers but at a higher cost. EPOs (Exclusive Provider Organizations) combine elements of both but exclude out-of-network coverage entirely. HDHPs (High Deductible Health Plans), often paired with HSAs (Health Savings Accounts), cater to those willing to pay lower premiums in exchange for higher deductibles, a strategy that works best for individuals with minimal healthcare needs.

Beyond plan types, coverage specifics matter. Prescription drug coverage, for example, varies widely. Some plans cover only generic medications, while others include brand-name drugs but with tiered copays. A 25-year-old with no chronic conditions might opt for a plan with limited drug coverage to save on premiums, whereas a 50-year-old managing hypertension would prioritize comprehensive coverage. Similarly, maternity care, mental health services, and preventive screenings aren’t always standard. Reviewing the Summary of Benefits and Coverage (SBC) document is essential to avoid surprises. For instance, a plan might cover annual checkups at 100% but require a 30% coinsurance for specialist visits.

Cost-sharing mechanisms—deductibles, copays, and coinsurance—further complicate the decision-making process. A plan with a $1,500 deductible and 20% coinsurance might seem affordable until a $10,000 medical bill arrives, leaving the insured responsible for $3,000 post-deductible. To mitigate this, some individuals pair high-deductible plans with an HSA, which allows tax-free contributions to cover medical expenses. However, HSAs require careful budgeting; contributions are irreversible, and penalties apply for non-qualified withdrawals.

Finally, timing and enrollment periods are critical. Open Enrollment for individual plans typically runs from November 1 to January 15, though qualifying life events (e.g., marriage, job loss) trigger Special Enrollment Periods. Missing these windows can leave one uninsured for months. Pro tip: Use the Healthcare.gov subsidy calculator to estimate premium tax credits, which can significantly reduce costs for those earning up to 400% of the federal poverty level. For example, a single individual earning $54,360 annually might qualify for a subsidy, lowering monthly premiums by hundreds of dollars.

In summary, choosing health insurance independently demands a meticulous approach. By dissecting plan types, scrutinizing coverage details, understanding cost-sharing, and leveraging enrollment tools, individuals can secure a policy that aligns with their health needs and financial situation. The process is daunting but not insurmountable—informed decisions today prevent financial strain tomorrow.

Understanding Medical Insurance Coverage for Support Animals

You may want to see also

Explore related products

![]()

Impact of employment status on insurance decisions

Employment status significantly shapes how individuals approach health insurance decisions, often dictating the level of choice, cost, and coverage they face. For the roughly 150 million Americans with employer-sponsored insurance, the decision-making process is streamlined: employers typically offer 2-3 plan options, with the company covering an average of 83% of premiums for single coverage. This arrangement minimizes personal financial burden and simplifies choices, though it limits customization. In contrast, the self-employed and unemployed must navigate the individual market, where premiums average $456 monthly for single coverage, with no employer subsidy. This stark disparity highlights how employment status directly influences both the feasibility and complexity of insurance decisions.

Consider the self-employed, who comprise about 10% of the U.S. workforce. Without access to group plans, they face higher premiums and fewer subsidies, often turning to Health Savings Accounts (HSAs) or high-deductible plans to manage costs. For instance, a 40-year-old freelancer might opt for a Bronze plan with a $7,000 deductible, paired with an HSA contribution of $3,850 annually, to balance affordability with tax advantages. Meanwhile, part-time workers, who often lack employer-sponsored benefits, may qualify for Medicaid or Affordable Care Act (ACA) subsidies if their income falls below 400% of the federal poverty level ($54,360 for an individual in 2023). These examples illustrate how employment status dictates not only the cost of insurance but also the strategic financial planning required to secure coverage.

The unemployed face perhaps the most challenging decisions, particularly during gaps in employment. COBRA allows them to continue their employer’s plan for up to 18 months, but at full cost plus a 2% administrative fee—a prohibitive expense for many. Alternatively, they can turn to the ACA marketplace, where 87% of enrollees qualify for premium tax credits, reducing average monthly costs to $116. However, this requires proactive enrollment during specific windows, such as the annual Open Enrollment Period (November 1 to January 15) or a Special Enrollment Period triggered by job loss. Failure to act within 60 days of losing coverage can result in a coverage gap, underscoring the urgency employment status imposes on insurance decisions.

A comparative analysis reveals that employment status not only determines access to insurance but also influences long-term health outcomes. Studies show that individuals with employer-sponsored insurance are 30% more likely to receive preventive care than those on individual plans, due to lower out-of-pocket costs and greater plan stability. Conversely, the self-employed and unemployed often delay care, with 40% reporting they skipped treatment due to cost concerns. This disparity underscores the need for policy interventions, such as expanding Medicaid eligibility or enhancing ACA subsidies, to mitigate the impact of employment status on health equity.

In navigating these decisions, practical tips can ease the burden. For the self-employed, comparing plans during Open Enrollment and leveraging tax deductions for premiums can maximize savings. The unemployed should act swiftly to explore COBRA, ACA options, or Medicaid, using tools like Healthcare.gov’s subsidy calculator to estimate costs. Part-time workers should verify eligibility for employer benefits or state-specific programs, as some companies offer prorated coverage. Ultimately, understanding how employment status intersects with insurance options empowers individuals to make informed, cost-effective choices in an often complex landscape.

Medically Needy: Is It Equivalent to Health Insurance?

You may want to see also

Explore related products

![]()

Role of government policies in individual insurance choices

Government policies significantly shape the landscape of individual health insurance choices, often determining who must navigate this complex terrain and how they do so. In the United States, for instance, the Affordable Care Act (ACA) expanded Medicaid eligibility and established health insurance marketplaces, reducing the number of uninsured individuals by millions. However, not everyone qualifies for Medicaid or employer-sponsored insurance, leaving a substantial portion of the population—estimated at around 15-20 million people—to select their own plans. This group includes self-employed workers, part-time employees, and those in the gig economy, who often lack access to group coverage. Policies like the ACA’s individual mandate, which requires most Americans to have health insurance or pay a penalty, further incentivize individuals to actively choose their plans.

Analyzing the impact of government policies reveals both opportunities and challenges. Subsidies and tax credits, such as those provided under the ACA, make individual plans more affordable for low- and middle-income earners. For example, individuals earning up to 400% of the federal poverty level ($54,360 for a single person in 2023) may qualify for premium tax credits. However, policy changes can introduce uncertainty. The repeal of the individual mandate penalty in 2019 led to concerns about reduced enrollment in individual plans, as healthy individuals might opt out, potentially destabilizing the risk pool. This underscores the delicate balance governments must strike between encouraging participation and ensuring affordability.

Instructively, individuals navigating their insurance choices should closely monitor policy updates, as they can directly affect plan availability and costs. For instance, the Inflation Reduction Act of 2022 extended enhanced subsidies through 2025, providing continued financial relief for marketplace enrollees. Practical tips include using government-run platforms like Healthcare.gov to compare plans, checking eligibility for cost-sharing reductions, and enrolling during open enrollment periods to avoid penalties. Additionally, understanding state-specific policies is crucial, as some states have expanded Medicaid or implemented their own mandates, further influencing individual choices.

Comparatively, countries with universal healthcare systems, such as Canada or the UK, demonstrate an alternative approach where government policies eliminate the need for individuals to choose their own insurance. In these systems, healthcare is publicly funded, and access is guaranteed, reducing the administrative burden on citizens. However, even in such systems, supplemental private insurance exists, offering additional benefits like private hospital rooms or faster access to specialists. This highlights that while government policies can minimize the need for individual choice, they often coexist with private options, creating a hybrid model.

Persuasively, the role of government policies in individual insurance choices cannot be overstated, as they directly influence accessibility, affordability, and equity. Policies that prioritize transparency, such as standardized plan designs and clear cost breakdowns, empower individuals to make informed decisions. Conversely, policies that reduce subsidies or narrow eligibility criteria can disproportionately affect vulnerable populations, exacerbating health disparities. Advocates for healthcare reform argue that governments should focus on expanding coverage options and simplifying enrollment processes to ensure that choosing health insurance is not a barrier to care. By doing so, policymakers can foster a system where individual choice is both meaningful and equitable.

Understanding HSAs: Medical Insurance Companion

You may want to see also

Frequently asked questions

Approximately 14-15 million people in the U.S. purchase health insurance individually through the Affordable Care Act (ACA) marketplaces or directly from insurers, requiring them to choose their own plans.

Most Americans with health insurance (about 158 million) receive it through employer-sponsored plans, where employers often offer a selection of plans for employees to choose from, though the employer typically subsidizes a portion of the cost.

Globally, the number varies widely by country. In nations with universal healthcare, like the UK or Canada, individuals do not choose private insurance. In contrast, in countries like the U.S. or parts of Europe with mixed systems, millions must select their own plans, though exact numbers are difficult to pinpoint due to differing healthcare models.

![New York Color Cover Stick, Light [781] 0.08 oz](https://m.media-amazon.com/images/I/81Cb2ipn4VL._AC_UL320_.jpg)