Several factors determine the cost of car insurance, including age, gender, driving history, vehicle type, location, and credit score. Typically, car insurance rates decrease over time, assuming a clean driving record. Age is one of the most crucial factors, as younger drivers are generally more likely to have accidents or take risks on the road due to their lack of experience. As a result, insurance rates are usually the lowest for middle-aged drivers and begin to climb again for older drivers due to increased accident risks. For males, rates drop significantly in their mid-20s, while females experience a similar decrease around the same age. Maintaining a clean driving record and improving one's credit score can also contribute to lower insurance rates over time.

| Characteristics | Values |

|---|---|

| Years of driving experience | Rates decrease over time, assuming a clean driving record. |

| Age | Rates are highest for teens and early 20s, dropping significantly in the mid-20s and climbing again in the driver's later years. |

| Gender | Male drivers' rates are higher than female drivers' in their teens and early 20s, but rates for all genders decrease as they approach 25. |

| Driving record | Accidents and violations will increase rates, but rates will decrease again 3-5 years after a violation if the driver keeps a clean record. |

| Credit score | An improved credit score may lower insurance rates. |

| Vehicle type | Cars with high safety ratings, low theft rates, and inexpensive parts have lower insurance rates. |

| Marital status | Getting married can lower insurance rates, especially for younger drivers. |

Explore related products

![]()

Age and gender

Insurance rates are typically the lowest for middle-aged drivers, but costs for seniors may increase due to a higher risk of accidents caused by physical, cognitive, or visual impairments. However, it's important to note that not all states permit age as a rating factor. Hawaii and Massachusetts ban its use, and Michigan only factors in years of driving experience. As a result, younger drivers in these states may still face higher premiums on average.

The difference in car insurance rates between men and women is more pronounced before the age of 25. For example, 18-year-old males cost 8% less to insure than their female counterparts, while 16-year-old males pay $423 more than females on average. At age 25, insurance rates for men have decreased significantly, dropping by an average of 18% from ages 20 to 21. Rates for women also decrease at 25, with an average drop of 8%.

While age and gender are crucial factors in determining insurance rates, other considerations, such as marital status and driving experience, also come into play. Married drivers, for instance, pay an average of $160 less per year than single, unmarried drivers. Additionally, drivers who frequent rural areas may receive discounts due to less congested roads and lower property crime rates.

PTA and D&O Insurance: California's Coverage

You may want to see also

Explore related products

![]()

Driving record

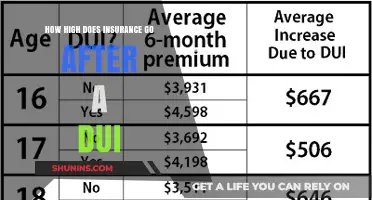

A driver's record, or driving history, can have a significant impact on their insurance rates. At-fault accidents, speeding tickets, and DUIs are among the factors that can influence the cost of insurance coverage.

In general, accidents or violations remain on a driver's record for three to five years, with more serious violations, such as alcohol-related offences, staying on record for much longer. For example, in the state of Florida, alcohol-related violations are tracked for 75 years.

The length of time that an accident or violation impacts insurance rates may differ from the duration of its presence on a driver's record. Typically, insurance rates are affected for three to five years following an incident. However, the exact duration depends on the state, the insurance company, and the nature of the incident. For instance, in Massachusetts, at-fault accidents can influence premiums for only six years.

It is important to note that insurance companies consider not only the most recent accident but also the entire driving history when calculating rates. As a result, multiple accidents, even if they are not at-fault, can lead to higher premiums. Additionally, factors such as fault, severity, driving profile, and the insurance company's policies also play a role in determining the impact on insurance rates.

Some insurance companies offer accident forgiveness, which prevents rates from increasing after the first at-fault accident, provided the driver has maintained a claims-free record for a certain number of years. This benefit may be included in the policy or offered as an add-on for an extra premium.

Geico Insurance: Permit Impact on Premiums

You may want to see also

Explore related products

![]()

Credit score

The time it takes to raise your credit score depends on the reasons behind your low score. If your score is low because you don't have a credit history, it may take a few months to get your first credit score. However, it will take longer to attain a good or excellent score. According to FICO, it takes at least six months to generate a credit score, and longer to earn a good or excellent score. VantageScore takes even less time, and you might qualify for a score within a month or two of opening an account.

If your score is low due to missed payments or bankruptcy, it will take longer to rebuild your credit. It can take years to rebuild your credit in such cases. Negative information on your credit report, such as missed payments, can have a significant impact on your credit score. It takes seven years for many types of negative information to be removed from your credit report.

To raise your credit score, you should make all your payments on time, keep your credit utilisation low, and maintain a healthy credit mix. It is also important to monitor your credit report regularly for any errors. While building a solid credit history takes time, you can establish a fair credit score (600-699) within a year or two by consistently making timely payments, maintaining low credit utilisation, and avoiding unnecessary credit applications.

HIP Insurance: College Students and Their Coverage

You may want to see also

Explore related products

![]()

Type of vehicle

The type of vehicle you drive is a factor in how much you pay for car insurance. This includes the make and model of the car, its age, and its safety features.

Firstly, the make and model of your car can affect your insurance rate based on how often that make is involved in insurance claims, how much it costs to repair or replace, and the safety features it has. For example, certain makes and models are known to cause more damage than other vehicles, and are therefore more expensive to insure. Cars with low safety ratings and high repair or replacement costs are also more expensive to insure.

Secondly, the age of your vehicle can impact insurance costs. Newer cars tend to be more expensive to insure because they are more costly to replace. They may also have more complex features or electrical components, which can drive up repair costs. However, older cars can also be expensive to fix, especially if they are premium or luxury models.

Thirdly, the size of your vehicle can make a difference in road accidents. Larger vehicles, such as SUVs, tend to result in lower repair costs compared to compact cars, which can lead to lower insurance rates. However, if a vehicle is likely to cause more damage to other vehicles in an accident, this may increase insurance rates.

Finally, certain types of cars, such as sports cars, are linked to riskier driving behavior and are therefore more expensive to insure.

Other factors that can impact insurance rates include the driver's age, location, gender, driving history, credit history, and occupation.

Insurance Rates: A Quick Spike Explained

You may want to see also

![]()

Insurance company

Insurance companies consider several factors when determining car insurance rates, and these factors can cause rates to fluctuate over time. While age is a significant consideration, with younger drivers generally considered higher-risk and facing higher rates, other elements come into play.

Firstly, a driver's record is crucial. Accidents, violations, and claims can result in higher premiums, with rates typically decreasing 3 to 5 years after a violation if the driver maintains a clean record. Additionally, insurance companies may offer discounts to long-term customers with clean records at every renewal.

Secondly, personal factors like improved credit scores, marital status, and vehicle type can impact rates. A higher credit score can lead to lower premiums, and insurance companies often view married drivers as more responsible, resulting in reduced rates. Furthermore, vehicles with high safety ratings, low theft rates, and inexpensive parts typically have lower insurance costs.

Lastly, external factors beyond an individual's control can influence rates. Inflation, rising repair costs, and more frequent claims due to extreme weather events have contributed to upward trends in average rates in recent years.

While insurance rates generally decrease over time as drivers gain experience and a clean record, it is important to note that this decrease is not automatic and can vary among insurance providers and individual circumstances. Regularly reviewing one's policy, comparing rates, and discussing specific factors with insurance companies can help identify opportunities for savings.

Defective Tail Lights: Insurance Impact and Costly Repairs

You may want to see also

Frequently asked questions

Insurance rates for young drivers decrease a little bit every year, with the most significant drops occurring between the ages of 18 and 25. The average cost of car insurance decreases by 7% each year for drivers between 16 and 25.

Insurance rates can be lowered by improving your credit score, maintaining a clean driving record, and taking a defensive driving course.

Having no accidents within the past three to five years can result in a car insurance discount of 26%, on average.

Insurance rates are influenced by various factors, including age, gender, driving history, vehicle type, location, and credit score. Rates generally decrease with age, as older drivers are considered less risky and more experienced.