The rising cost of insurance has become a significant financial burden for many individuals and families, making it increasingly difficult to secure adequate coverage without breaking the bank. However, there are several strategies and initiatives aimed at making insurance more affordable, such as leveraging technology to streamline processes, promoting competition among providers, and offering tailored policies that meet specific needs without unnecessary add-ons. Additionally, government subsidies, tax incentives, and community-based programs are playing a crucial role in reducing premiums for low-income households. By exploring these options and staying informed about industry trends, consumers can find cost-effective solutions that provide the protection they need without compromising their financial stability.

Explore related products

What You'll Learn

- Government Subsidies: Explore policies offering financial aid to reduce insurance premiums for low-income individuals

- Group Plans: Leverage collective bargaining through employers or associations for discounted rates

- High Deductibles: Opt for higher out-of-pocket costs to lower monthly insurance premiums

- Preventive Care Focus: Reduce long-term costs by emphasizing regular health check-ups and wellness programs

- Comparative Shopping: Use online tools to compare policies and find the most cost-effective options

![]()

Government Subsidies: Explore policies offering financial aid to reduce insurance premiums for low-income individuals

Government subsidies can significantly lower insurance premiums for low-income individuals, making essential coverage more accessible. Programs like the Affordable Care Act’s (ACA) premium tax credits in the U.S. directly reduce monthly costs based on income and household size. For example, a family of four earning up to $106,000 annually in 2023 may qualify for subsidies, with savings averaging $500 to $800 per month. These credits are applied directly to premiums, ensuring immediate financial relief. Similar models exist globally, such as Australia’s Medicare Levy Surcharge, which subsidizes private health insurance for lower-income earners. By tying subsidies to income thresholds, governments ensure that financial aid reaches those who need it most, bridging the affordability gap in insurance markets.

Implementing effective subsidy policies requires careful design to avoid unintended consequences. For instance, means-testing ensures that aid is targeted to low-income individuals, but overly complex eligibility criteria can deter applicants. A streamlined application process, such as integrating subsidy applications into existing tax or social welfare systems, can improve uptake. Additionally, subsidies should be indexed to inflation and cost-of-living adjustments to maintain their effectiveness over time. Policymakers must also guard against market distortions, such as insurers raising base premiums in response to subsidies. Regular audits and transparency measures can mitigate these risks, ensuring subsidies fulfill their intended purpose of making insurance affordable without inflating overall costs.

Critics often argue that government subsidies create dependency or strain public budgets, but evidence suggests otherwise. Subsidies for health insurance, for example, reduce uncompensated care costs by encouraging preventive care and early treatment, ultimately lowering healthcare expenditures. In the U.S., Medicaid expansion under the ACA demonstrated that subsidizing insurance for low-income individuals improves health outcomes and reduces hospital debt. Similarly, auto insurance subsidies in states like California have lowered uninsured rates, reducing financial risks for all drivers. When designed thoughtfully, subsidies are an investment in public health and economic stability, not a drain on resources.

To maximize the impact of insurance subsidies, governments should adopt a multi-pronged approach. First, raise awareness through targeted outreach campaigns, particularly in underserved communities. Second, simplify enrollment processes by integrating subsidy applications into existing platforms, such as tax filing systems. Third, collaborate with insurers to offer standardized, subsidized plans that are easy to compare. Finally, monitor program effectiveness through data analysis, adjusting subsidy levels and eligibility criteria as needed. By combining financial aid with accessibility and transparency, governments can ensure that insurance remains affordable for low-income individuals without compromising market efficiency.

Accessing Your Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Group Plans: Leverage collective bargaining through employers or associations for discounted rates

One of the most effective ways to secure more affordable insurance is by tapping into the power of group plans. By pooling together through employers, professional associations, or alumni networks, individuals can access discounted rates that would be unattainable on their own. This collective bargaining model leverages the principle of economies of scale: insurers offer lower premiums to groups because the risk is spread across a larger number of policyholders, reducing administrative costs and ensuring a steady stream of revenue. For example, a small business with 10 employees can often negotiate health insurance rates 10-20% lower than individual plans, even with comparable coverage.

To maximize the benefits of group plans, it’s essential to understand the mechanics of enrollment and eligibility. Employers typically offer group insurance as part of their benefits package, but associations and organizations often have similar programs available to members. When evaluating these options, pay attention to the specifics of the plan, such as deductibles, copays, and coverage limits. For instance, a group health plan might offer a $1,000 deductible compared to $2,500 for an individual plan, significantly reducing out-of-pocket costs. Additionally, some group plans include perks like wellness programs or discounted gym memberships, adding further value.

A common misconception is that group plans are only available through full-time employment. In reality, part-time workers, freelancers, and even retirees can access group insurance through professional associations or alumni groups. For example, the Freelancers Union offers health insurance plans to its members, while many universities provide alumni with access to group life or health insurance policies. These options are particularly valuable for individuals who don’t qualify for employer-sponsored plans but still want to avoid the higher costs of individual coverage.

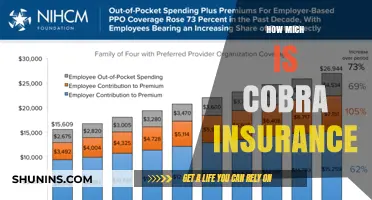

While group plans offer significant savings, they aren’t without limitations. The coverage is often tied to membership or employment, meaning a change in status could result in loss of benefits. For instance, leaving a job might require transitioning to COBRA coverage, which can be more expensive. To mitigate this risk, consider pairing group insurance with supplemental policies, such as short-term health insurance or critical illness coverage, to ensure continuous protection. Additionally, always review the plan’s network of providers to ensure your preferred doctors and hospitals are included.

In conclusion, group plans are a powerful tool for making insurance more affordable, but they require proactive research and strategic planning. Whether through an employer, association, or organization, leveraging collective bargaining can lead to substantial savings and enhanced benefits. By understanding eligibility, comparing plan details, and preparing for potential changes, individuals can maximize the value of group insurance and secure financial peace of mind.

Primary vs Secondary Insurance: Understanding Your Coverage

You may want to see also

Explore related products

![]()

High Deductibles: Opt for higher out-of-pocket costs to lower monthly insurance premiums

Choosing a high-deductible health plan (HDHP) can significantly reduce your monthly insurance premiums, but it’s a trade-off that requires careful consideration. For example, a 35-year-old individual might pay $200 monthly for a low-deductible plan with a $1,000 deductible, compared to $120 monthly for an HDHP with a $4,000 deductible. The immediate savings of $80 per month ($960 annually) can be appealing, especially if you’re generally healthy and rarely visit the doctor. However, this strategy hinges on your ability to cover the higher out-of-pocket costs if a medical need arises.

To make this approach work, start by assessing your health history and financial stability. If you’re in your 20s or 30s with no chronic conditions and a solid emergency fund (ideally $5,000 or more), an HDHP could align with your lifestyle. Pairing it with a Health Savings Account (HSA) amplifies the benefits: contributions are tax-deductible, grow tax-free, and can be used for qualified medical expenses. For instance, contributing $2,000 annually to an HSA not only offsets potential out-of-pocket costs but also builds a long-term health financial cushion.

However, this strategy isn’t foolproof. Unexpected accidents or illnesses can lead to financial strain if you’re unprepared. For families or individuals with recurring medical needs, the higher deductible might negate premium savings. A 45-year-old with diabetes, for example, would likely face frequent out-of-pocket expenses that outweigh the reduced premiums. Always compare total annual costs (premiums + deductible + copays) between plans to ensure the HDHP truly saves you money.

Practical tips can maximize the value of an HDHP. First, negotiate medical bills—providers often offer discounts for upfront payments. Second, use preventive care services, which are typically covered at no cost under HDHPs, to avoid larger issues later. Finally, shop around for prescriptions using tools like GoodRx to find lower prices. By combining these strategies, you can leverage the lower premiums of an HDHP while minimizing financial risk.

In conclusion, high deductibles are a viable path to affordable insurance for those with good health and financial discipline. It’s not a one-size-fits-all solution, but for the right individual, it offers both immediate savings and long-term financial benefits. Assess your situation, plan for contingencies, and use available tools to make the most of this approach.

Becoming a Life Insurance Agent in Maryland: A Guide

You may want to see also

Explore related products

![]()

Preventive Care Focus: Reduce long-term costs by emphasizing regular health check-ups and wellness programs

Regular health check-ups and wellness programs aren’t just about catching illnesses early—they’re a strategic investment in lowering insurance costs over time. Consider this: a 2020 study by the *Journal of Occupational and Environmental Medicine* found that companies with robust wellness programs saw a $3.27 return for every dollar spent, primarily through reduced healthcare claims and absenteeism. For individuals, this translates to fewer catastrophic health events, which are the primary drivers of high insurance payouts. For instance, annual blood pressure screenings for adults over 40 can detect hypertension early, allowing for lifestyle changes or medication that prevent costly heart attacks or strokes later.

To implement this approach effectively, start by understanding what preventive services your insurance covers at no out-of-pocket cost under the Affordable Care Act (ACA). These include vaccinations, cancer screenings, and chronic disease monitoring. For example, a 50-year-old man should prioritize colonoscopies every 10 years, while a 30-year-old woman should focus on HPV testing every 5 years. Pair these screenings with wellness programs like gym reimbursements, smoking cessation classes, or mental health apps. Many insurers offer discounts or rewards for completing such programs, directly reducing premiums or deductibles.

However, preventive care isn’t a one-size-fits-all solution. Over-screening can lead to unnecessary procedures and stress, so tailor your approach based on age, gender, and family history. For instance, someone with a family history of diabetes should monitor blood sugar levels annually starting at age 35, while others might wait until 45. Similarly, wellness programs should align with personal health goals—a sedentary office worker might benefit from a step-tracking challenge, while someone with high stress could prioritize mindfulness workshops.

The key takeaway is that preventive care shifts the focus from reactive treatment to proactive management. By investing time and effort upfront, individuals can avoid the financial and health burdens of chronic conditions. For insurers, this means fewer high-cost claims, which can stabilize premiums for everyone. It’s a win-win: healthier individuals and more sustainable insurance systems. Start small—schedule that overdue check-up, enroll in a wellness program, and watch how these steps compound into long-term savings.

Colorado Insurance Insights: Understanding Dam Coverage and Policies

You may want to see also

Explore related products

![]()

Comparative Shopping: Use online tools to compare policies and find the most cost-effective options

Online comparison tools have revolutionized the way consumers shop for insurance, transforming a once tedious process into a streamlined, data-driven task. These platforms aggregate quotes from multiple providers, allowing users to compare premiums, coverage limits, deductibles, and policy features side by side. For instance, tools like The Zebra, Policygenius, and NerdWallet’s insurance comparator pull real-time data from insurers, ensuring accuracy and relevance. This transparency empowers consumers to make informed decisions, often uncovering savings of 20–30% compared to traditional broker-assisted purchases. The key lies in the ability to filter results based on specific needs—whether it’s a high liability limit for auto insurance or a low deductible for health plans—ensuring the cheapest option isn’t just affordable but also adequate.

To maximize the effectiveness of these tools, start by gathering precise information about your coverage needs. For auto insurance, note your vehicle’s make, model, and annual mileage; for health insurance, consider your age, pre-existing conditions, and prescription needs. Input this data consistently across platforms to ensure apples-to-apples comparisons. Beware of default settings that may skew results—for example, some tools pre-select higher coverage levels than necessary. Additionally, pay attention to the fine print: a lower premium might come with higher out-of-pocket costs or exclusions. Pro tip: Use incognito mode when comparing quotes to avoid price increases based on browsing history, as some insurers adjust rates based on perceived demand.

While online tools are powerful, they aren’t infallible. Some insurers, particularly regional providers or specialty carriers, may not be included in comparison databases. For example, USAA, known for its competitive rates for military families, often requires direct inquiry. Similarly, certain policy types, like flood or earthquake insurance, might not be comprehensively covered by mainstream comparators. In such cases, supplement your research with direct insurer websites or industry reports. Another caution: avoid fixating solely on price. A $50 annual savings might not justify a policy with poor customer service or a high complaint ratio, which can be verified through the National Association of Insurance Commissioners (NAIC) database.

The ultimate takeaway is that comparative shopping isn’t just about finding the lowest price—it’s about optimizing value. For example, a 25-year-old driver might save $300 annually by choosing a policy with a $1,000 deductible over a $500 one, provided they have an emergency fund to cover the difference. Similarly, bundling home and auto insurance can yield discounts of 10–25%, but only if the combined policy offers comparable coverage. Use comparison tools as a starting point, then cross-reference findings with customer reviews and financial stability ratings from agencies like A.M. Best. By combining data-driven insights with practical considerations, you can secure insurance that’s both affordable and reliable.

ICICI Prudential Life Insurance: ULIP or Not?

You may want to see also

Frequently asked questions

Insurance affordability depends on factors like maintaining a good credit score, bundling policies (e.g., auto and home), choosing higher deductibles, and taking advantage of discounts for safe driving, loyalty, or safety features.

To lower car insurance premiums, drive safely to avoid accidents and claims, maintain a clean driving record, reduce coverage on older vehicles, and shop around for quotes from multiple providers to find the best rates.

Yes, some governments offer programs like Medicaid for health insurance or subsidized plans through healthcare marketplaces. Additionally, low-income individuals may qualify for discounted auto or home insurance through state-specific programs.