Homeowners' insurance is an important consideration for anyone looking to buy a property. While it is not a legal requirement, most mortgage lenders will insist on it. The cost of insurance varies depending on location, the value of the property, and the level of coverage desired. The average cost of homeowners' insurance in the U.S. is $2,110 per year, but this can be much higher or lower depending on individual circumstances. For example, the average cost of a $1 million policy with excellent credit is $6,228, which jumps to $24,282 with poor credit. There are several types of homeowners' insurance, with varying levels of protection, and it is important to understand the extent of the coverage provided by each policy.

Explore related products

What You'll Learn

![]()

Average insurance costs

The average cost of homeowners insurance in the United States is $1,411 per year, according to the Insurance Information Institute. However, the cost of insurance can vary widely depending on several factors. The location of your home is a significant factor, with insurance being more expensive in areas with high real estate values. The age and square footage of your home, the cost of building materials, and the type of home will also impact the price of insurance. For example, older homes may need to install smoke alarms and carbon monoxide detectors, which can save up to 10% or more in annual premiums.

The coverage you choose will also affect the overall cost of insurance. Most homeowners insurance policies provide a minimum of $100,000 worth of liability insurance, but higher amounts are available, with some recommending a minimum of $300,000 to $500,000 worth of coverage. You can also choose to insure your possessions for actual cash value, which pays less for older items, or for replacement cost, which is about 10% more but covers the cost of replacing items without accounting for depreciation.

Additionally, the presence of security features such as burglar alarms, sprinkler systems, and dead-bolt locks can help lower annual premiums. Homeowners who own their residences outright may also see lower premiums, as insurance companies assume that a fully-owned home will be better cared for.

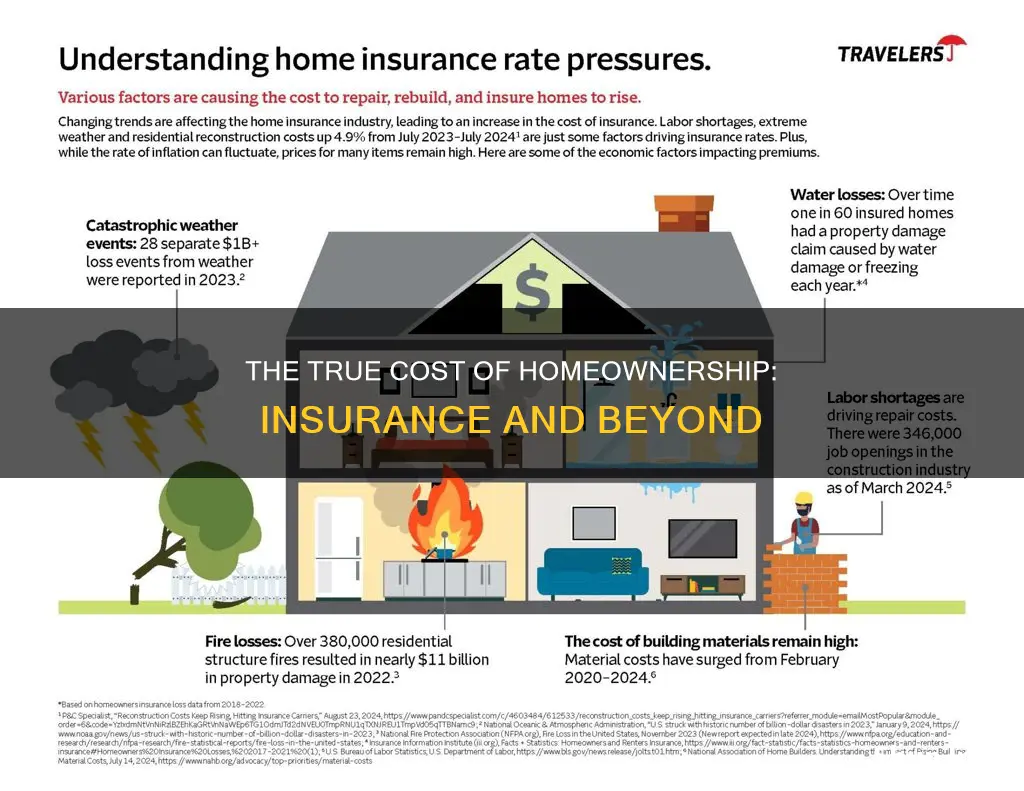

It is important to note that insurance rates can fluctuate frequently, and the cost of home insurance has been increasing due to inflation, the elevated cost of building materials, and the likelihood of future extreme weather-related losses.

Homeowners Insurance: Does It Cover Flood Damage?

You may want to see also

Explore related products

![]()

Rebuilding costs

The rebuild cost of a house is the amount it would cost to completely rebuild it if it were destroyed beyond repair. This includes the price of labour and materials. The rebuild cost is usually lower than the sale price or market value of a house. However, if your home is made of non-standard materials or has specialist architectural features, the rebuild cost may be higher than its market value. In this case, it is important to insure your home against the higher rebuild cost to avoid insurance shortfalls.

There are several ways to calculate the rebuild cost of your home. One way is to use a house rebuilding cost calculator, such as the one provided by the Building Cost Information Service. Another way is to hire an independent property appraiser to inspect your house and estimate the rebuild cost. This will provide an accurate estimate, but you will have to pay for their services. A quick way to estimate the rebuild cost is to multiply the total square footage of your home by local, per-square-foot building costs. You can find out construction costs in your community by contacting your local real estate agent, builders association, or insurance agent.

It is important to review the rebuild cost of your home each time you renew your insurance. If you renovate your home or build an extension, you should recalculate the rebuild cost and speak to your insurer to ensure you are fully covered. Changes in the cost of construction materials, labour, and inflation can all affect the rebuild cost of your home. To offset your financial risk, homeowners insurance companies typically offer replacement cost policies and extended dwelling coverage.

The replacement cost of a home is the amount of money it would take to rebuild it from the ground up with construction materials similar to those from the original build. This does not include the value of the land, as land is not factored into rebuilding estimates. The replacement cost value factors in the costs of labour, building materials, and other expenses relevant to the rebuilding process. Many insurers require homeowners to insure their homes for at least 80% of the replacement cost, and some may require 100%.

There are different types of replacement cost coverage offered by homeowners insurance companies. The standard replacement cost is the most basic financial protection, offering to repair or rebuild your home without any depreciation factored in. The extended replacement cost increases your home's dwelling coverage policy limit, helping to guard against inflation and increasing repair and construction costs. The guaranteed replacement cost, often the most expensive option, ensures reimbursement for the full amount required to replace or rebuild your home, regardless of the current building expenses.

How to Insure Someone Else's Home

You may want to see also

Explore related products

![]()

Personal property coverage

The amount of personal property coverage provided by your homeowners insurance policy can vary. Some policies offer a percentage of your dwelling coverage, such as 50%, as personal property coverage. For example, if your dwelling limit is $200,000, you may have $100,000 in personal property insurance coverage. Your policy may allow you to increase or decrease this limit to suit your needs.

It is important to note that personal property coverage typically has sub-limits for certain high-value items. For example, jewellery coverage may be limited to under $2,000. If you have expensive personal items, you may need to schedule them separately or add an insurance rider to your policy. This will ensure that your items are covered for their full value, but it may increase your premium.

There are two types of loss settlements for personal property: replacement cost and actual cash value. Replacement cost covers the item as new at the time of the claim, without deducting depreciation. Actual cash value, on the other hand, pays you the replacement cost minus depreciation, taking into account the item's age and wear and tear. Flood insurance for belongings is only available on an actual cash value basis.

To ensure adequate coverage, it is recommended to regularly appraise your personal property and review your policy limits. Additionally, consider implementing safety measures such as installing a burglar alarm, smoke alarms, carbon monoxide detectors, deadbolt locks, and sprinkler systems, as these can help lower your annual premiums.

HOA Rules: Homeowners Insurance — What You Need to Know

You may want to see also

Explore related products

![]()

Credit score impact

While it is challenging to determine exactly how much a credit score affects homeowners' insurance, it is clear that credit scores do have an impact on the rates offered by insurance companies. This impact varies depending on the state and the company.

In most states, insurance companies use credit-based insurance scores to evaluate credit history and calculate premiums. These scores are based on soft credit pulls, which do not impact an individual's credit score. However, these soft pulls allow insurance companies to assess the risk of offering an individual a policy. If an individual is deemed more likely to file a claim, they will likely pay more for their policy. Conversely, if they are seen as lower risk, they will probably pay less.

The impact of credit scores on insurance rates is particularly notable for individuals with poor credit. On average, individuals with poor credit pay 82% more for home insurance than those with excellent credit. This is because individuals with poor credit are considered higher-risk by insurance companies and are therefore offered higher rates. However, it is important to note that insurance companies use their own scoring metrics to determine credit-based insurance scores, so the impact of credit scores on rates can vary.

While credit scores can influence insurance rates, they are not the sole factor in determining rates. Other factors, such as location, the home's size and age, and the installation of safety and security equipment, also play a role in rate-setting. Additionally, insurance companies may deny coverage or renewal based on factors other than credit scores.

It is worth noting that individuals with poor credit may find more affordable insurance rates by checking rates from multiple companies, as some insurers may offer lower rates for those with poor credit. Improving credit scores over time can also help individuals with poor credit save money on homeowners' insurance in the long run.

Home Insurance: Annual Renewal and Why It's Necessary

You may want to see also

Explore related products

![]()

Optional coverages

- Extended Replacement Cost Coverage: This coverage provides additional funds beyond the amount specified in your original policy. It typically ranges from 20% to 25% of your dwelling value and serves as a buffer if rebuilding costs exceed expectations. To obtain this coverage, you may need to meet specific underwriting rules and conditions set by your insurance company.

- Guaranteed Replacement Cost Coverage: This coverage ensures that your insurance company will pay the full cost of repairing or replacing your home, even if it exceeds your policy limits. This is especially useful if construction costs in your area have increased since you purchased your policy. Not all insurance companies offer this level of coverage, so be sure to check with your provider.

- Personal Articles Floater: This coverage is designed for valuable possessions that may exceed the coverage limits in your regular policy. Items typically covered include jewellery, furs, stamps, coins, guns, computers, antiques, silverware, fine arts, and other collectibles. A personal articles floater lists each insured item, provides a description, and specifies any excluded perils. It often offers broader coverage than a standard home insurance policy, and there is usually no deductible applied.

- Increased Limits on Money and Securities: This endorsement increases the coverage for money, bank notes, securities, and deeds. This can be particularly useful if you keep a significant amount of cash or valuable securities in your home.

- Secondary Premises and Liability Coverage: If you own a secondary residence, such as a summer home, this endorsement extends your homeowners insurance coverage to that property. It provides peace of mind and ensures that your secondary residence is protected against disasters and liabilities.

- Water Backup Coverage: This coverage protects you from damage caused by water that backs up, overflows, or discharges from sewers, drains, sump pumps, or related equipment. It covers damage to your belongings and the cost of water removal and sewage removal. This coverage is particularly relevant if you have a sump pump in your basement or crawl space.

- Musical Instrument Coverage: Musical instruments often require separate coverage due to their unique nature and value. This coverage ensures that your musical instruments are protected in the event of damage or loss.

- Sewer Line Coverage: Sewer line coverage protects against issues with the sewer line, such as blockages or damage. This coverage is worth considering, especially if you live in an area with ageing infrastructure or if your neighbours have experienced sewer line problems.

- Wind and Flood Coverage: Depending on your location, you may want to consider optional coverages for wind-driven rain and flooding. These perils are not always included in standard homeowners insurance policies, but they can cause significant damage, especially in high-risk areas.

- Earthquake Coverage: If you live in an area prone to seismic activity, consider adding earthquake coverage to your policy. Keep in mind that earthquake coverage often comes with a separate, higher deductible.

Remember, these are just a few examples of optional coverages available. The specific optional coverages offered by insurance providers may vary, and it's always best to speak with an agent to determine which coverages are most suitable for your individual needs.

House Insurance: A Necessary Evil?

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in the US is $2,110 per year, but rates vary depending on location, coverage amount, and credit score.

The cost of homeowners insurance can be influenced by factors such as location, credit score, coverage amount, and the presence of security features like burglar alarms, smoke alarms, and carbon monoxide detectors.

Homeowners insurance typically covers repairs or rebuilding costs for damage to the structure of the home and detached structures like garages and sheds due to fire, lightning, hail, and explosions. It also covers personal belongings, additional living expenses if the home is uninhabitable, and liability protection for bodily injury or property damage to others.

The amount of coverage needed depends on the cost of rebuilding your home, replacing your belongings, and the level of liability protection desired. Experts recommend purchasing higher liability limits and ensuring coverage is sufficient to rebuild your home.

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)