The cost of homeowners insurance is determined by a variety of factors, including the location, age, and square footage of the property, as well as the type of construction, materials used, and safety features. The national average cost of homeowners insurance is $1,678 per year, according to Forbes, while NerdWallet estimates the average to be $2,110 per year for $300,000 worth of dwelling coverage. To estimate the amount of insurance needed, one can multiply the total square footage of their home by the local per-square-foot building costs. This guide will explore the various factors influencing the cost of homeowners insurance and provide insights into calculating the necessary coverage.

Explore related products

What You'll Learn

![]()

Homeowners insurance costs vary by state

Homeowners insurance costs vary widely by state, and several factors influence these differences. The national average cost of homeowners insurance in the US is $2,110 per year for $300,000 worth of dwelling coverage, but rates can differ by thousands of dollars across states.

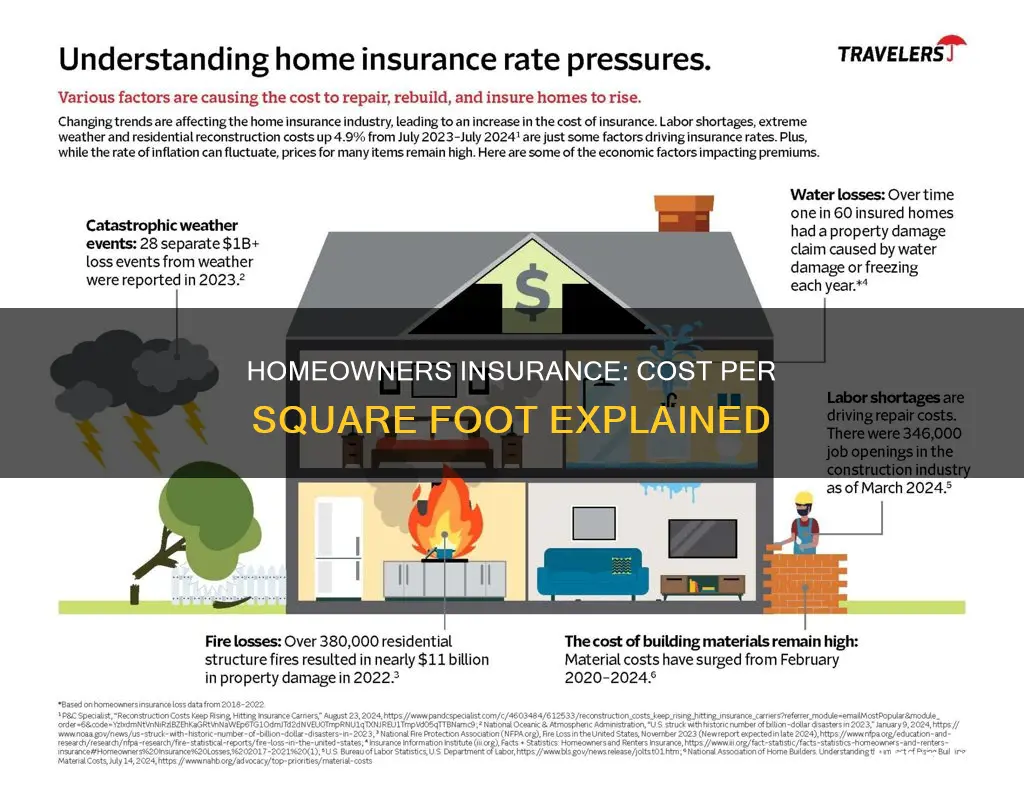

Location is a significant factor in determining insurance rates. States with a higher risk of natural disasters, such as tornadoes, windstorms, hurricanes, wildfires, hail storms, and flooding, tend to have higher insurance premiums. For example, states like Oklahoma, Texas, Nebraska, and Colorado have experienced rapidly increasing insurance costs due to recent severe weather events. Additionally, coastal homes often have higher insurance premiums than inland homes.

The cost of living in a particular state also impacts insurance rates. A higher cost of living can make it more expensive to rebuild after a claim, resulting in higher insurance rates. Conversely, states with a lower cost of living may have cheaper insurance rates.

Other factors that contribute to varying insurance costs across states include the frequency of property crimes, the age and square footage of homes, the cost of building materials, and individual credit history.

To estimate the amount of insurance coverage needed, homeowners can multiply the total square footage of their home by the local per-square-foot building costs. It is also recommended to consider adding an inflation guard clause to the policy, as construction costs can rise suddenly after a major catastrophe, pushing rebuilding costs above the policy limits.

Mortgage Insurance: Appraised Value Impact

You may want to see also

Explore related products

![]()

Square footage is a factor

To estimate the amount of insurance you need, multiply the total square footage of your home by the local, per-square-foot building costs. You can find out the construction costs in your community by contacting your local real estate agent, builders association, or insurance agent.

The type of construction and exterior materials used in your home can also affect the cost of insurance. For example, concrete block homes may cost less to insure than wood frame houses because they are less susceptible to fires and strong winds. Similarly, asphalt shingles for roofing may result in lower insurance costs than cedar or wood-shakes because they are less flammable.

Other factors that can impact the cost of homeowners insurance include the location of the property, the age of the home, the number of bedrooms and bathrooms, whether there is a garage, the type of foundation, improvements or upgrades made to the home, and the number of people living in the home.

General Insurance's Fort Worth Location

You may want to see also

Explore related products

![]()

Inflation guard clauses

To estimate how much homeowners insurance you need, multiply the total square footage of your home by the local per-square-foot building costs. However, as costs rise, your homeowners coverage needs to keep pace. If it doesn't, you may find yourself underinsured, which can be a very costly situation. This is where an inflation guard clause comes in.

An inflation guard clause is an essential part of your homeowners policy, safeguarding your most valuable asset. It is a powerful solution to help keep your home insured against the unexpected. An inflation guard endorsement automatically adjusts the dwelling limit to reflect current construction costs in your area when you renew your insurance. This is because the cost of building materials and labour costs are subject to inflationary pressures. For example, construction wages are up nearly five percent following the pandemic and its resulting labour shortages.

After a major catastrophe such as a hurricane, tornado, or wildfire, construction costs may rise suddenly because of increased demand and a shortage of construction workers. This price bump may push rebuilding costs above your homeowners policy limits. An inflation guard endorsement can protect against this possibility by automatically adjusting the insured value of your home.

However, inflation guard coverage is not always automatic and may need to be selected as an option for your policy. It is important to review your current coverage and assess its adequacy. You should also ensure your policy's inflation guard aligns with local market realities.

Vacation Rental Damage Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Natural disasters and location

Natural disasters can have a significant impact on the cost of homeowners' insurance. The frequency and severity of natural disasters have increased due to climate change, leading to higher insurance payouts and uncertainty about future losses. As a result, reinsurance companies have increased their rates for insurance companies, who pass these costs on to policyholders. Homeowners in high-risk areas may pay more for insurance than those in lower-risk regions, even within the same state.

The main natural disasters that influence insurance costs include tropical cyclones, wildfires, tornadoes, flooding, earthquakes, and severe storms. Tropical cyclones, which are the most common and destructive of these disasters, generate strong winds and heavy rainfall. In contrast, droughts are becoming more frequent and prolonged due to rising temperatures, and they can also be detrimental to homes.

Standard homeowners' insurance policies typically exclude coverage for disasters such as earthquakes, floods, mudflows, landslides, and tsunamis. Separate policies or endorsements are often required for these perils. For instance, flood insurance can be obtained through the National Flood Insurance Program (NFIP) or private insurance companies, with NFIP offering up to $250,000 for dwelling coverage and $100,000 for personal contents protection. The average cost of flood insurance through NFIP is $1,153 per year.

Homeowners in coastal areas prone to hurricanes may need to purchase additional coverage for wind damage, as some home insurance companies exclude this peril. Furthermore, insurance companies in earthquake-prone states may set a minimum deductible for earthquake insurance, which can range from 2% to 20% of dwelling coverage.

To ensure adequate coverage, it is recommended to review your homeowners' insurance policy and understand the specific perils covered. In the event of a disaster, having sufficient coverage can provide financial protection and facilitate the rebuilding process.

Home Insurance Costs in the Outer Banks

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Crime rates and safety features

Safety features act as a risk-reducing mechanism, lowering insurance premiums. Installing a security system, improving lighting in the yard, and implementing motion sensors or security cameras can deter burglars and reduce the likelihood of theft. Modernizing heating, plumbing, and electrical systems can also decrease the chances of fire and water damage, which are favourable factors in the eyes of insurance providers. Additionally, consider installing water leak detection systems and devices that automatically shut off the water supply in the event of damage to pipes or plumbing. These measures not only protect your home but also reduce the frequency and cost of insurance claims.

The presence of a pool on your property can significantly impact your insurance rates due to the associated risks. However, you can mitigate these risks by installing safety features such as a fence around the pool, life-saving devices, first aid kits, and a portable pool lift. Insurance companies may offer discounts for these safety measures, reducing your overall premiums.

The age and condition of your roof are also important considerations. Older roofs or those in poor condition may incur higher premiums due to the increased risk of weather-related damage. Conversely, a newer roof or one constructed with fortified roofing materials may qualify for policy discounts.

It is worth noting that while installing safety features and making home upgrades can lower your insurance costs, the upfront cost of these improvements can be significant. Nevertheless, the long-term benefits of reduced risks and potential savings on insurance claims make these investments worthwhile.

Homeowner's Insurance: Does It Cover Basement Seepage?

You may want to see also

Frequently asked questions

To estimate the amount of insurance you need per square foot, multiply the total square footage of your home by the local, per-square-foot building costs. You can find out the construction costs in your community by contacting your local real estate agent, builders association or insurance agent.

The cost of homeowners insurance is determined by factors such as the location, age, and square footage of your home, the deductibles and policy limits, the cost of building materials, and the type of construction materials used.

The average cost of homeowners insurance in the US is about \$2,110 a year for \$300,000 worth of dwelling coverage, but rates vary by state. The national average cost is \$1,678 per year, according to Forbes, and \$2,466 per year according to Bankrate.

Many insurers offer online tools for estimating the cost of homeowners insurance. You can also use a home insurance calculator to get an estimate of your home insurance costs.