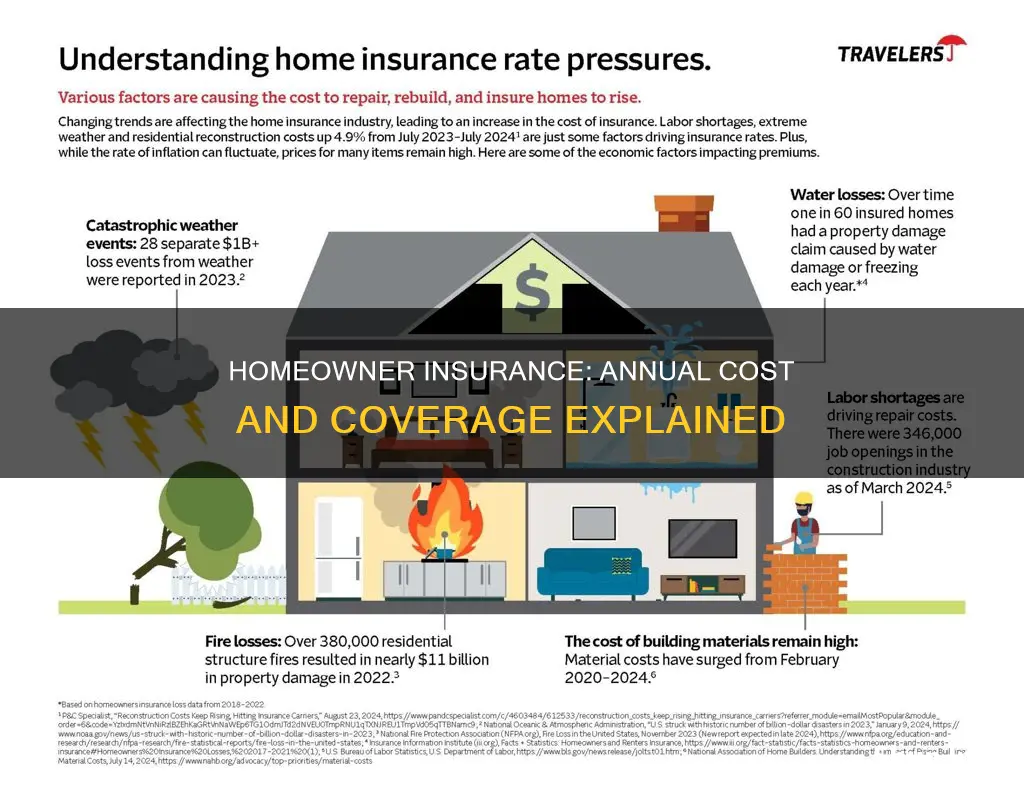

The cost of annual homeowner insurance varies depending on a multitude of factors, including the location of the home, the size of the home, and the type of construction materials used. For instance, the average annual premium in Oklahoma City is $5,431, while in Portland, Oregon, it is $1,029. Additionally, homes in areas prone to wildfires, flooding, or extreme weather may face higher insurance costs or even difficulty obtaining coverage. Home insurance rates are also influenced by the amount of dwelling coverage, with larger homes requiring more coverage. Other factors that can impact the cost of homeowner insurance include the claims history of the homeowner and the presence of additional hazards such as a swimming pool or a dog.

| Characteristics | Values |

|---|---|

| Average Annual Home Insurance Cost in the US | $1,411 |

| Average Annual Home Insurance Cost in the US (2024) | $2,377 |

| Average Annual Home Insurance Cost in the US (Progressive's Network) | $1,090.08 - $3,353.74 |

| Average Annual Home Insurance Cost in Oklahoma City | $5,431 |

| Average Annual Home Insurance Cost in Portland, Oregon | $1,029 |

| Average Annual Home Insurance Cost in Vermont, Alaska, and Delaware | $<1,000 |

| Average Annual Home Insurance Cost in Nebraska and Louisiana | >$5,000 |

| Average Annual Home Insurance Cost in Florida | $2,437 |

| Average Annual Home Insurance Cost in Oregon | $793 |

| Average Annual Home Insurance Cost for USAA Homeowners Insurance | $1,535 |

| Average Annual Home Insurance Cost for a Condo | $200 |

| Average Annual Home Insurance Cost for a Single-Family Detached Structure on a Beachfront | $5,000 |

| Factors Affecting Home Insurance Cost | Location, claims history, coverage limits, home characteristics, dwelling coverage, construction materials, coverage selections, prior claims, deductible, home size, building materials, siding type, flooring materials, heating type, roof type, shape, and location-based factors |

Explore related products

What You'll Learn

![]()

Home insurance rates vary by state and city

Home insurance rates vary significantly by state and city, and several factors influence these fluctuations. Firstly, the cost of dwelling coverage, which is the part of your policy that covers the rebuilding of your home's structure in case of damage or destruction, plays a pivotal role in determining rates. If your house is larger or boasts high-end features, the cost of dwelling coverage will be higher, leading to more expensive insurance.

Location is another critical factor in the variability of home insurance rates. Different areas of the country face varying levels of risk, with some regions being more susceptible to natural disasters like tornadoes, hurricanes, and wildfires. States with a higher likelihood of these events tend to have pricier insurance rates as the frequency of claims is higher. For instance, Nebraska, Louisiana, Florida, Oklahoma, and Kansas are among the most expensive states for home insurance due to the elevated risk of tornadoes and hurricanes. Conversely, states with a lower risk of natural disasters, such as Hawaii, Vermont, Delaware, Alaska, and Maine, tend to have cheaper insurance rates.

Additionally, the characteristics of your home can also impact insurance rates. The construction materials used, roof type, and home features like siding and flooring can influence the overall value of your property, thereby affecting insurance costs. For example, concrete block homes may be cheaper to insure than wood frame houses due to their higher resistance to fires and strong winds.

Crime rates in your ZIP code, proximity to emergency services, and access to water sources for firefighting are further location-based factors that insurers consider when setting rates. These variables collectively contribute to the diverse home insurance rates observed across different states and cities in the United States.

Erie Homeowners Insurance: Does It Cover Mine Subsidence?

You may want to see also

Explore related products

![]()

The size of your deductible affects your premium

The cost of annual homeowners insurance varies widely, with location being a significant factor. For example, the average annual premium in Oklahoma City is $5,431, while in Portland, Oregon, it's $1,029. Other factors that influence the cost of homeowners insurance include the characteristics of your home, such as construction materials and roofing type, as well as the likelihood of natural disasters in your area.

When purchasing homeowners insurance, you will have the option to select a deductible, which is the amount you pay out of pocket when you file a claim. The deductible is separate from your insurance premium, which you pay annually to your insurance carrier. The higher the deductible, the lower your premium, and vice versa. This means that if you choose a higher deductible, you will pay less in premiums upfront but will need to pay more out of pocket if you need to file a claim.

For example, let's say a fire causes $50,000 worth of damage to your home, and you have a $1,000 policy deductible. Your insurance company will reimburse you for the damage minus the deductible, so you will receive $49,000 ($50,000 minus $1,000). You will then pay the $1,000 deductible directly to the contractor repairing your home.

When choosing a deductible, it's important to consider your financial situation. If you can comfortably afford higher out-of-pocket costs, you may opt for a higher deductible to secure a lower annual premium. On the other hand, if you don't have much saved for unexpected expenses, you may prefer a lower deductible, even if it means paying a higher premium.

It's worth noting that deductibles can vary depending on the type of storm or damage to your home. For example, in Florida and some coastal counties, special hurricane deductibles may apply to named storm or hurricane damage claims. Additionally, some companies offer percentage-based deductibles, where you pay a percentage of your home's insured value, typically between 1% and 10%.

The Captive Conundrum: Exploring the Nature of Farmers Insurance Relationship

You may want to see also

Explore related products

![]()

The type of home you have impacts the cost

Location is a significant factor in determining the cost of homeowner's insurance. Homes in coastal regions or areas prone to wildfires, tornadoes, hurricanes, earthquakes, or floods may be at a higher risk of damage and therefore have higher insurance rates. Crime rates in your ZIP code can also impact your insurance rates, as insurers may consider the likelihood of theft claims. Additionally, your proximity to a fire station and the distance from your home to the nearest woods or brush can affect your insurance costs.

The construction materials and features of your home can also impact the cost of insurance. For example, concrete block homes may cost less to insure than wood frame houses as they are less susceptible to fires and strong winds. The type of roof you have, such as asphalt shingles or a hip roof, can also influence your insurance rates, with less flammable and wind-resistant options often resulting in lower costs. The siding type, flooring materials, and heating system of your home are other factors that insurers consider when assessing the risk and determining the cost of insurance.

The age of your home is another factor that can impact the cost of insurance. Older homes may cost more to insure than newer ones due to the lack of modern safety features and the potentially higher cost of repairs. The presence of certain features, such as swimming pools or trampolines, may also be considered "attractive nuisances" by insurance companies, leading to higher insurance rates due to the potential for injury.

The amount of dwelling coverage you need is another critical factor in determining the cost of homeowner's insurance. Dwelling coverage pays to rebuild or repair the structure of your home if it is damaged or destroyed. A larger home or one with high-end features will typically require more dwelling coverage and result in higher insurance costs.

Home Business: Am I Covered by Homeowners Insurance?

You may want to see also

Explore related products

![]()

The cost of building materials affects premiums

The cost of homeowners insurance varies widely across the United States. The average annual premium can range from $1,029 in Portland, Oregon, to $5,431 in Oklahoma City. Several factors influence the cost of homeowner insurance premiums, including the cost of building materials.

The building materials used in a home affect the cost of homeowner insurance premiums because they impact the reconstruction cost. Homes with more expensive building materials will cost more to rebuild, leading to higher insurance premiums. For example, an older home with materials like plaster walls, ornate moldings, stained-glass windows, and hardwood floors will be more costly to repair or replace. Similarly, homes with roofs made of cedar or wood shakes will likely have higher insurance costs than those with asphalt shingles, which are less flammable.

The type of building materials can also indicate the age of the home. Older homes may need to be brought up to code during the rebuilding process, increasing the overall cost. Newly constructed homes often receive an average discount of 36% compared to older homes. Additionally, older homes may lack modern safety features, and repairs can be more expensive.

The cost of building materials is not the only factor that influences insurance premiums. The location of the property also plays a significant role. Homes in coastal regions, near woods, or in areas prone to wildfires may have higher insurance costs due to the increased risk of natural disasters. Crime rates in the ZIP code can also impact premiums, as insurers consider the likelihood of theft claims.

To manage the cost of homeowner insurance, it is essential to review average home insurance rates in your state and compare rates from multiple companies. Renovating or upgrading your home can also impact your insurance costs. For example, upgrading your home's electrical system may make you eligible for cheaper premiums or more insurance options. However, finishing a basement or building a swimming pool will likely increase your insurance costs due to the higher replacement cost value of your home.

Homeowners Insurance: Non-Permitted Work and Its Risks

You may want to see also

Explore related products

![Takashi Utsunomiya Premium annual concert dinner show 2009 [DVD]](https://m.media-amazon.com/images/I/91xRGzaTV1L._AC_UL320_.jpg)

![]()

Home insurance rates fluctuate frequently

Location is a significant determinant of insurance rates. Homes in areas prone to natural disasters, such as hurricanes, wildfires, and floods, tend to have higher insurance costs. For example, states like Florida, California, and Louisiana experience more frequent natural disasters, resulting in higher average insurance premiums. Additionally, homes in coastal regions, near woods, or in areas with high crime rates may face higher insurance rates due to increased risks.

The type of home also influences insurance rates. Larger homes typically have higher insurance costs because more area is susceptible to damage or destruction. The construction materials and features of a home can also impact rates. For example, concrete block homes may be cheaper to insure than wood-frame houses due to their higher resistance to fires and strong winds. Roof type and shape are also considered, with hip roofs being more resistant to wind and potentially lowering insurance costs.

Other factors that contribute to fluctuating insurance rates include the size of the deductible, claims history, and coverage limits. A higher deductible generally leads to lower premiums, while multiple claims can result in higher rates. Running a business from home or owning a dog may also increase insurance costs due to higher liability risks.

It is important to note that insurance rates can change rapidly, especially with the increasing impact of climate-related events. Homeowners are advised to compare insurance rates annually and consider multiple quotes to ensure they obtain the best deal.

Evacuation Coverage: What Your Home Insurance Includes

You may want to see also

Frequently asked questions

The cost of annual homeowner insurance varies depending on a number of factors, including location, claims history, coverage limits, and home characteristics. The average cost of insurance for a 12-month policy ranges from $1,090.08 to $3,353.74.

The location of your home is one of the biggest factors in determining the cost of homeowner insurance. Homes in areas that are prone to natural disasters, such as hurricanes, wildfires, earthquakes, and floods, tend to have higher insurance costs. Additionally, homes in coastal regions, near woods, or with higher crime rates may be more expensive to insure due to an increased risk of theft, natural disasters, or damage.

The size of your home impacts the cost of insurance because larger homes have more surface area that can be damaged or destroyed, leading to higher repair and rebuilding costs. As a result, insurance companies may charge higher premiums for larger homes to cover the potential costs of repairs or rebuilding.

Yes, the type of building materials used in your home can affect the cost of insurance. Homes built with more expensive or flammable materials may have higher insurance rates because they are more costly to repair or replace in the event of damage. Additionally, certain roof types, such as asphalt shingles, may be less expensive to insure because they are less susceptible to fire or wind damage.

![HOME GROWN 131,200+ Pure Wildflower Seeds 𝗨𝗦𝗔 - Premium Texas Flower Seeds [3 Oz] Perennial Garden Seeds for Birds & Butterflies - Wild Flowers Bulk Perennial: 22 Varieties Flower Seed for Planting](https://m.media-amazon.com/images/I/817-zh2xH5L._AC_UL320_.jpg)