Homeowners insurance is a necessity, protecting your home and possessions against damage or theft. It also covers liability for accidents that injure other people or damage their property. The cost of basic homeowners insurance varies depending on several factors, including the location, size of the house, and the coverage amount required. The average cost of homeowners insurance in the US is $2,110 per year, but this can range from $1,090 to $3,353 per year. The price also depends on the age and construction materials of the house, as well as the coverage limits and deductibles selected. It's important to assess the value of your possessions and the level of risk to determine how much coverage you need.

Explore related products

$14.99 $14.99

What You'll Learn

- Homeowners insurance costs vary by location, property characteristics, and coverage

- The average annual cost is $2,110, but it can range from $1,090 to $3,353

- Policies cover damage, theft, liability, and additional living expenses

- The cost of rebuilding/replacement is covered, but contents coverage may be extra

- Credit history, claims history, and property features like pools can affect rates

![]()

Homeowners insurance costs vary by location, property characteristics, and coverage

Homeowners insurance costs vary depending on several factors, including location, property characteristics, and desired coverage. On average, homeowners insurance costs $2,110 per year or $176 per month, according to NerdWallet's analysis. However, the cost can range from as low as $610 per year in Hawaii to as high as $6,210 per year in Oklahoma.

Location plays a significant role in determining the cost of homeowners insurance. Insurance companies consider the risks associated with the area, such as weather-related risks like flood zones or areas prone to earthquakes, and location-related risks like property crime. For example, homes in neighbourhoods with high crime rates or frequent vandalism and break-ins may be considered high risk, leading to higher insurance rates. Additionally, insurance companies may offer discounts to homeowners who install additional safety features, such as deadbolts and security systems, which can help offset the higher premiums in these areas.

Property characteristics also influence insurance costs. The size of the house, the age of the property, and the presence of safety features are all taken into account. Older homes tend to be more expensive to insure than newer ones due to the lack of modern safety features and the potentially higher cost of repairs. The construction and materials used in the home can impact the cost as well. If your house is large or has high-end features, it will likely cost more to rebuild, resulting in higher insurance premiums.

The desired level of coverage is another critical factor in determining homeowners insurance costs. Dwelling coverage, which pays for the rebuilding or repair of the structure of your home in case of damage or destruction, is a significant component of the overall cost. Standard homeowners insurance policies typically cover disasters such as fire, lightning, hail, and explosions. However, additional coverage may be needed for areas prone to flooding or earthquakes. Liability coverage is another important consideration, as it protects you financially if someone is injured on your property. Most homeowners insurance policies provide a minimum of $100,000 in liability coverage, but higher amounts are recommended, with some suggesting $300,000 to $500,000 worth of coverage.

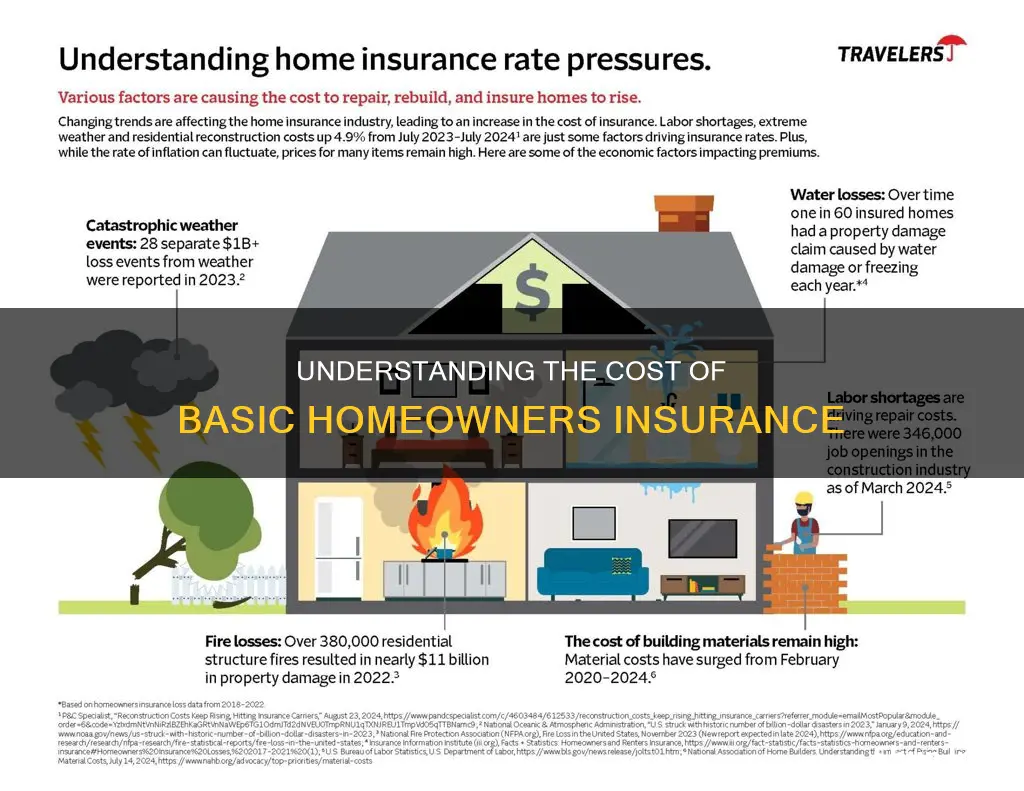

It is worth noting that insurance costs can fluctuate over time due to various factors, such as post-pandemic inflation, supply chain disruptions, and the increasing frequency of natural disasters. As a result, homeowners need to stay proactive about their coverage and regularly review their policies to ensure they have adequate protection.

Davis Vision Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

The average annual cost is $2,110, but it can range from $1,090 to $3,353

The cost of basic homeowners insurance can vary depending on several factors. The average annual cost is $2,110, but it can range from $1,090 to $3,353. This variation in pricing is influenced by a combination of factors, including location, claims history, coverage limits, and the characteristics of the home.

Location plays a significant role in determining insurance rates. Homes in coastal regions may be riskier to insure due to a higher likelihood of natural disasters. Crime rates in the area, proximity to wildfire-prone areas, and access to fire hydrants and fire departments are also considered when setting rates. Additionally, the age and construction materials of your home are important factors. Older homes may be more expensive to insure, especially if they require updates to meet modern safety and building codes or if they were built with hard-to-source materials. Homes constructed with materials that are less susceptible to fire and wind damage, such as concrete blocks, may benefit from lower insurance costs.

The amount of coverage you need is another critical aspect influencing insurance rates. Most homeowners insurance policies provide a minimum of $100,000 in liability insurance, but experts recommend considering higher coverage amounts, ranging from $300,000 to $500,000. It's important to ensure that your policy limits are sufficient to cover the cost of rebuilding your home in the event of a disaster, as construction costs can rise suddenly due to increasing demand for building materials and labour after a catastrophe.

Furthermore, your claims history can impact your insurance rates. Multiple previous claims may result in a higher rate, as insurers consider you more likely to file future claims. The presence of attractive nuisances, such as swimming pools or trampolines, can also increase your liability and, consequently, your insurance rate.

Basic homeowners insurance typically combines property and casualty coverages, protecting your home and possessions against damage or theft. It also provides liability coverage for accidents that injure others or damage their property. When considering the cost of basic homeowners insurance, it's essential to review the specific coverages included in the policy to ensure they meet your individual needs and provide adequate protection.

Home Insurance: Overgrown Tree Damage Covered?

You may want to see also

Explore related products

![]()

Policies cover damage, theft, liability, and additional living expenses

Basic homeowners insurance covers damage, theft, liability, and additional living expenses. The cost of insurance depends on your location, the size of your house, and how much coverage you need. On average, home insurance costs $2,110 per year. However, this can vary significantly depending on the state, with Oklahoma, Texas, and Nebraska being the most expensive, and Hawaii, Vermont, and Delaware being the least expensive.

Damage coverage includes protection against disasters such as fire, lightning, hail, and explosions. It also covers other types of water damage, such as rain coming through a hole in the roof caused by strong winds. However, it is important to note that flood and earthquake damage are typically not covered by basic homeowners insurance policies. To ensure coverage for these perils, separate policies or endorsements may be required.

Theft coverage is also a standard component of homeowners insurance. It covers the loss or theft of personal possessions, including expensive items like jewelry or artwork, up to a certain limit. Additional coverage can be purchased for valuable or irreplaceable items. Creating a detailed home inventory is highly recommended, as it helps streamline the claims process and ensures accurate valuation and replacement of your belongings.

Liability coverage is another crucial aspect of homeowners insurance. Most policies provide a minimum of $100,000 in liability insurance, but higher amounts are available and often recommended. Liability coverage protects you financially if someone is injured or their property is damaged while on your premises. It covers legal expenses and provides compensation for the injured party. If your assets exceed the liability limits of your policy, consider purchasing an umbrella policy, which offers broader coverage and higher limits.

Finally, additional living expenses (ALE) coverage is included in most homeowners insurance policies. ALE reimburses you for extra costs incurred if your home becomes uninhabitable due to a covered loss. This includes expenses such as temporary housing, food, transportation, and even pet boarding costs. It is important to keep detailed records and receipts to substantiate your ALE claim and ensure prompt reimbursement from your insurance provider.

Tow Truck Insurance: Is It a Worthy Investment?

You may want to see also

Explore related products

$5.97 $10.99

![]()

The cost of rebuilding/replacement is covered, but contents coverage may be extra

The cost of rebuilding or replacement is typically covered by homeowners insurance, but contents coverage may be extra. This is an important distinction to understand when considering a policy.

Homeowners insurance provides a range of coverage, depending on the policy type. Most policies cover the physical dwelling and other structures on the property, such as a garage, fence, driveway, or shed. However, the rebuilding cost coverage may not be enough in the event of a catastrophe, such as a hurricane, tornado, or wildfire, which can cause construction costs to rise suddenly due to increased demand for building materials and labour. To protect against this, some insurance companies offer extended replacement cost coverage, which can pay an extra 5 to 25 percent above the limits, or a guaranteed replacement cost policy, which will pay whatever it costs to rebuild your home as it was before the disaster.

Contents coverage, also known as personal property coverage, is typically included in homeowners insurance policies but at a percentage of the dwelling coverage, usually around 50 to 70 percent. This coverage helps protect the contents of your home, including personal items such as furniture, clothing, electronics, and kitchenware, in the event that they are destroyed, damaged, or stolen due to a covered loss or peril. To ensure adequate coverage, it is advisable to conduct a home inventory and assess the value of your belongings. If the value of your belongings exceeds the coverage limit, you may need to add an insurance rider to your policy for specific items, which will likely raise your premium.

The cost of rebuilding/replacement coverage and contents coverage can vary depending on various factors, including location, the size of the house, and the coverage limits. It is important to review your policy carefully to understand what is and is not covered and to make any necessary adjustments to ensure adequate protection.

Income Continuation Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

$8.99 $14.99

![]()

Credit history, claims history, and property features like pools can affect rates

Basic homeowners insurance provides coverage for disasters such as damage due to fire, lightning, hail, and explosions. The standard amount of coverage may not be enough, and it is recommended that homeowners consider purchasing at least $300,000 to $500,000 worth of liability coverage.

Credit history, claims history, and property features like pools can affect the rates of basic homeowners insurance. Firstly, credit history can influence the rates charged for basic homeowners insurance. While requesting a quote should not negatively impact your credit score, insurance companies in most states can consider your credit history to determine rates. They use your credit history to generate a credit-based insurance score, which measures how likely you are to file an insurance claim. Policyholders with higher credit-based insurance scores may be viewed as more likely to pay on time and maintain their homes, resulting in lower premiums. However, only a few states have banned the use of credit as a rating factor, and the impact of credit history on rates varies across different insurance companies.

Secondly, claims history can also affect insurance rates. Homeowners with an extensive claims history may be considered high-risk and charged higher rates. The likelihood of future claims is influenced by factors such as claim size, type of claim, and state regulations. Multiple claims over a short period, regardless of the amount, can raise red flags for insurers. Certain types of claims, such as dog bites, water damage, and theft, are more likely to recur and may result in higher rates.

Lastly, property features like pools can impact insurance rates. Pools are considered an "attractive nuisance," and homeowners insurance must cover liability and the pool itself. The cost of insurance for homes with pools can vary depending on factors such as the value of the home, the presence of a fence, and whether the pool is considered part of the home or an external structure. In-ground pools may result in a premium increase, while above-ground pools may be considered personal property, impacting the personal property limit of the policy. Overall, the presence of a pool can lead to higher insurance rates due to the associated risks and liabilities.

Insured but Not Covered: Closing Fails

You may want to see also

Frequently asked questions

The cost of basic homeowners insurance is influenced by the location, size of the house, and how much coverage is needed. Other factors include the age of the home, the construction materials used, and the presence of attractive nuisances such as swimming pools or trampolines.

It is recommended that homeowners have enough insurance to cover the cost of rebuilding their home and replacing their belongings in the event of a disaster. A home inventory can help determine how much coverage is needed for belongings, and most policies provide a minimum of $100,000 worth of liability insurance.

Basic homeowners insurance typically includes property and casualty coverage, as well as liability coverage for injuries or damage that occurs on the property. It also covers additional living expenses if the home is damaged and the residents cannot live in it.