The cost of family medical insurance is an important consideration for any household. With rising healthcare costs, advances in medical technology, and the increasing price of medical services, insurance premiums have consistently risen over the years. The cost of insurance can vary depending on the region, with local costs of living, specific state health regulations, and the level of competition among insurers all playing a part. Other factors that influence the price of insurance include the number of family members, age, medical history, and the type of plan. It is therefore important to understand the different types of health insurance plans available and select one that suits your family's needs and budget.

| Characteristics | Values |

|---|---|

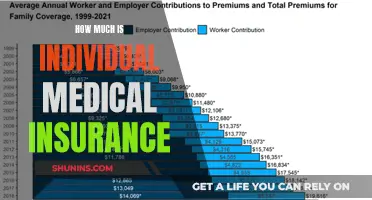

| Average Annual Premium for a Family of Four in 2020 | $21,342 |

| Average Annual Premium Increase Over Five Years | 22% |

| Average Monthly Premium for a Silver Plan for a Family of Five | $307 |

| Average Yearly Premium for a Silver Plan for a Family of Five | $3,682 |

| Types of Plans | Affordable Care Act (ACA), Medicare, Medicaid, Dental, Vision, Supplemental, Accident, Critical Illness, Short-term, and ACA plans |

| Costs to Consider | Premium, Deductible, Copays, and Coinsurance |

| Coverage | Day care expenses, in-hospitalization expenses, ambulance charges, pre & post-hospitalization expenses, maternity expenses, non-medical expenses, and preventive health check-ups |

| Other Factors Affecting Cost | State or region, local cost of living, specific state health regulations, and level of competition among insurers |

| Cost of Family Health Insurance in India for a Family of Four | ₹7,000 to ₹50,000 |

Explore related products

What You'll Learn

- Premium costs: Monthly fees vary by state, family size, and medical history

- Deductibles: Out-of-pocket expenses before insurance coverage kicks in

- Copays and coinsurance: Fixed fees vs. percentage costs for each service

- Coverage: Consider day-to-day, hospital, ambulance, and prescription needs

- Plan types: HMO, ACA, Medicare, and Medicaid plans have different benefits

![]()

Premium costs: Monthly fees vary by state, family size, and medical history

The premium costs of a good family medical insurance plan can vary based on several factors, including state, family size, and medical history. Firstly, let's talk about the impact of location and competition among insurers. The cost of living, specific health regulations, and competition among insurers in your state can influence the premium prices you'll encounter. For example, a state with high medical costs and limited insurance providers may have higher premiums than a state with more options and competitive pricing.

Additionally, family size plays a role in determining premium costs. Adding more members to a health insurance policy typically leads to higher total premiums due to the increased likelihood of medical claims. However, some insurance policies are designed with a reduced incremental cost for each additional family member, making it more financially feasible for larger families to obtain coverage under a single plan. It's also worth noting that children can be covered under the Children's Health Insurance Program (CHIP) if your income falls below a certain level.

Now, let's discuss the influence of medical history on premium costs. Insurance companies generally conduct a thorough assessment of your health profile, including your past medical records and pre-existing conditions, to determine the premium charges. If you have a history of illnesses or chronic conditions, you may face higher premiums and out-of-pocket expenses due to the expected increased usage of healthcare services. On the other hand, if you have had a relatively healthy life, your premiums are likely to be lower.

Other factors that can impact your premiums include age, tobacco use, and plan type. Older individuals tend to pay higher premiums because they are at a higher risk of developing illnesses. Tobacco use can also significantly affect premiums, with some states allowing up to a 50% higher premium for smokers compared to non-smokers. Finally, the type of plan you choose, such as individual, family, or employer-sponsored, will also influence the premium costs.

Legal Guardians and Medical Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

Deductibles: Out-of-pocket expenses before insurance coverage kicks in

The cost of family medical insurance can vary depending on several factors, including the type of plan, the number of family members covered, and the level of coverage required. When considering the cost of family medical insurance, it is essential to understand the concept of deductibles, which are out-of-pocket expenses that must be paid before insurance coverage kicks in.

A deductible is an out-of-pocket expense that you, the policyholder, are responsible for paying towards an insured loss. In the context of family medical insurance, a deductible refers to the amount you must pay for covered healthcare services before your insurance plan starts paying. For example, if you have a $500 deductible and incur a covered medical expense of $1000, you will need to pay the first $500 out of your pocket, after which your insurance plan will cover the remaining $500.

Deductibles are an integral part of insurance contracts, allowing for risk-sharing between the policyholder and the insurer. They can be a specific dollar amount, as in the example above, or a percentage of the total insured amount. For instance, if you have a 2% deductible on a $100,000 home insurance policy, a $2000 deductible will be applied to any claim payment. Thus, if you have a covered loss of $10,000, you will receive a claim check for $8000 after the deductible is deducted.

It's important to note that deductibles may vary based on state regulations and the specific terms of your insurance policy. Additionally, certain types of insurance, such as auto insurance or homeowners policies, may have deductibles that apply each time you file a claim, while others, like hurricane deductibles in some states, are applied once per season.

When choosing a family medical insurance plan, understanding how deductibles work is crucial. High-deductible health plans (HDHPs) typically come with lower monthly premiums, but you will pay more out-of-pocket before the insurance coverage kicks in. On the other hand, low-deductible plans have higher monthly premiums but provide earlier insurance payments, making them suitable for families with frequent doctor visits or anticipated medical needs.

Understanding Medical Insurance Coverage After Job Loss

You may want to see also

Explore related products

![]()

Copays and coinsurance: Fixed fees vs. percentage costs for each service

When it comes to health insurance, there are several costs to consider when comparing family health insurance plans. The cost of health insurance can be a significant part of a family budget. While the exact costs will depend on your specific plan and the services you require, here is a detailed look at copays and coinsurance, and how they differ in terms of fixed fees versus percentage costs for each service.

Copays

Copays, or copayments, are flat fees or fixed amounts that you pay each time you receive a covered service. This means that the amount is predetermined and does not change based on the final bill. Copays are typically paid upfront, directly at the doctor's office or when filling a prescription. The amount can vary depending on the provider, service, and your specific health plan. For example, a copay for a doctor's visit might be $15, $20, or another amount, while a copay for medication could be $10 or $40. Copays are usually separate from your monthly premium and deductible. Not all plans use copays, and some may use both copays and deductibles/coinsurance, depending on the covered service.

Coinsurance

Coinsurance, on the other hand, is a percentage of the cost of a covered service that you pay after meeting your deductible. For instance, if your doctor's visit costs $100 and your coinsurance is 20%, you would pay $20 out of pocket, and your insurance plan would cover the remaining $80. Coinsurance typically ranges from 20% to 40%, but the exact percentage depends on your plan. Like copays, coinsurance is often separate from your monthly premium, and it may not apply to preventive services.

Choosing a Plan

When choosing a family health insurance plan, it is essential to understand the different types of plans available and how the costs are structured. HMO plans, for example, typically offer coverage from select in-network doctors and hospitals, while PPO plans may provide more flexibility in choosing healthcare providers. Additionally, consider your family's specific needs and budget. If you require frequent care, a plan with lower copays and coinsurance might be more suitable, whereas if you only need infrequent care, a plan with higher copays and coinsurance could be an option.

Cost Considerations

In addition to copays and coinsurance, there are other costs associated with family health insurance plans. These include the monthly premium, which is the amount you pay to keep your insurance active, and the deductible, which is the amount you must pay for eligible services before your insurance coverage begins. The Children's Health Insurance Program (CHIP) is a state resource that provides low-cost or free health insurance for families with children who meet certain qualifications. You can also explore high-deductible health plans, traditional health plans, and health insurance subsidies to reduce or remove premium costs.

Choosing the Right Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Coverage: Consider day-to-day, hospital, ambulance, and prescription needs

When considering a family medical insurance plan, it is important to think about the day-to-day, hospital, ambulance, and prescription needs of your family.

Day-to-day coverage includes annual health check-ups and daycare procedures such as cataract treatment and dialysis. Family plans can also cover tests, doctor's fees, and post-treatment hospital visits. This can include pre-hospitalisation coverage of up to 60 days and post-hospitalisation coverage of up to 180 days.

Hospital coverage can include emergency services, hospitalisation expenses, and other medical costs. For example, Fatima Khan, a 32-year-old, opted for a family floater plan covering herself, her spouse, and two dependent children with a health plan of ₹10 lacs. A few months after the policy purchase, Fatima underwent kidney stone removal surgery and was hospitalised for 5 days. Her medical bills reached ₹3 lakh, which were paid by the insurance company.

Ambulance coverage can vary depending on your insurance plan. For example, Medicare Part B covers ground ambulance transportation when travelling in any other vehicle could endanger your health. It may also cover emergency transportation in an airplane or helicopter if ground transportation cannot provide immediate and rapid transport. Non-emergency ambulance transportation may also be covered if you have a written order from your doctor stating that it is medically necessary.

Prescription coverage can include prescription drugs, although it is important to check your policy carefully to understand any exclusions or limitations.

Life Insurance and Medicaid: Burial Application Impact

You may want to see also

Explore related products

![]()

Plan types: HMO, ACA, Medicare, and Medicaid plans have different benefits

The cost of family medical insurance can vary depending on the specific plan and the needs of the family. When considering a plan, it is essential to understand the different types of health insurance available and the benefits they offer. Here is an overview of the key differences between HMO, ACA, Medicare, and Medicaid plans:

HMO (Health Maintenance Organization) Plans

HMO plans are a type of Medicare Advantage Plan (Part C) offered by private insurance companies. With an HMO plan, you generally need to receive care from doctors, healthcare providers, and hospitals within the plan's network. However, some HMOs are Point-of-Service (HMOPOS) plans, which allow for out-of-network services at a higher cost. HMO plans often include additional benefits, such as prescription drug coverage, vision and hearing exams, and preventive dental coverage. They usually have lower monthly premiums and an out-of-pocket maximum that limits annual medical expenses.

ACA (Affordable Care Act) Plans

ACA plans, also known as Marketplace, Exchange plans, or Obamacare, are designed to be affordable and accessible. They are available through state marketplaces and may offer subsidies to reduce premium costs for those without employer-provided insurance, Medicare, or Medicaid coverage. ACA plans can vary in terms of coverage, cost, and access to doctors and specialists.

Medicare Plans

Medicare is a federal health insurance program primarily for individuals 65 and older, but it may also cover those under 65 with certain disabilities or special conditions. Original Medicare has deductibles and does not have an out-of-pocket spending limit. To supplement this, many people enrol in Medicare Advantage plans (Part C), which offer additional benefits, including prescription drug coverage and vision and dental care. Medicare Advantage plans can have provider restrictions, and enrollees typically choose a primary care physician (PCP) to oversee their care and referrals.

Medicaid Plans

Medicaid plans are state-run and provide low-cost or free health insurance for individuals and families with limited financial resources. These plans often have income and eligibility requirements and may offer comprehensive coverage, including dental and vision care.

When choosing a family medical insurance plan, it is essential to consider your family's specific needs, budget, and eligibility for different programs. Understanding the benefits and restrictions of each plan type will help you make an informed decision.

Oral Surgery: Dental or Medical Insurance, Which is Best?

You may want to see also

Frequently asked questions

A good family medical insurance plan is one that appropriately covers your family's health needs within your budget. It is important to check the coverage offered under the plan and select one that balances your family's coverage needs with your budget.

The cost of family medical insurance varies depending on several factors, including the number of family members, location, age, and medical history of the family members. For example, the average monthly premium for a Silver plan for a family of five is $307 ($3,682 yearly). The cost of insurance is also influenced by local cost of living, specific state health regulations, and the level of competition among insurers.

When choosing a family medical insurance plan, it is important to consider the different types of plans available, such as Affordable Care Act (ACA) plans, Medicare, and Medicaid plans. You should also understand the costs associated with the plan, including premiums, deductibles, copays, and coinsurance. Additionally, consider the coverage offered, such as day care expenses, hospitalization expenses, ambulance charges, maternity expenses, and preventive health check-ups.