The cost of homeowners insurance depends on a variety of factors, including the location, size, and age of the house, as well as the coverage amount and deductible selected. The national average cost of homeowners insurance is $2,466 per year for a policy with a $300,000 dwelling limit, but rates can vary significantly from state to state and even city to city. For example, the average annual rate in Houston is $6,370, while in San Jose, California, it is $1,090. Older homes tend to be more expensive to insure due to the lack of modern safety features, and homes in coastal regions may also be pricier due to the increased risk of natural disasters. Additionally, the construction materials used, such as roofing and siding, can impact the cost of insurance, with more flammable or damage-prone materials raising the price.

| Characteristics | Values |

|---|---|

| Average cost of homeowners insurance | $2,466 per year for a policy with a $300,000 dwelling limit |

| Average cost of homeowners insurance with $350,000 in dwelling coverage | $1,678 per year |

| Average cost of homeowners insurance with $300,000 in dwelling coverage | $2,601 per year |

| Cheapest insurer | Progressive, with an average annual rate of $729 |

| Most expensive insurer | American Family, with an average annual rate of $2,745 |

| Cheapest state for homeowners insurance | Hawaii, Vermont, and Delaware |

| Most expensive state for homeowners insurance | Oklahoma, Texas, and Nebraska |

| Cheapest ZIP code for home insurance | 96813 in Honolulu, with an average annual rate of $610 |

| Most expensive ZIP code for home insurance | 28480 in North Carolina, with an average annual rate of $29,684 |

| Factors influencing insurance rates | Location, claims history, coverage limits, home characteristics, credit score, and deductible |

Explore related products

What You'll Learn

![]()

Home insurance costs vary by location

Home insurance costs vary depending on location, with some states being more expensive than others. For instance, in 2025, Oklahoma, Texas, and Nebraska were the most expensive states for home insurance, with average annual rates of $6,210, $4,585, and $4,505, respectively. In contrast, Hawaii, Vermont, and Delaware were the least expensive states, with average annual rates of $610, $950, and $1,025, respectively. The national average cost of home insurance in the US is $2,466 per year for a policy with a $300,000 dwelling limit, or $1,678 per year for a policy with $350,000 in dwelling coverage.

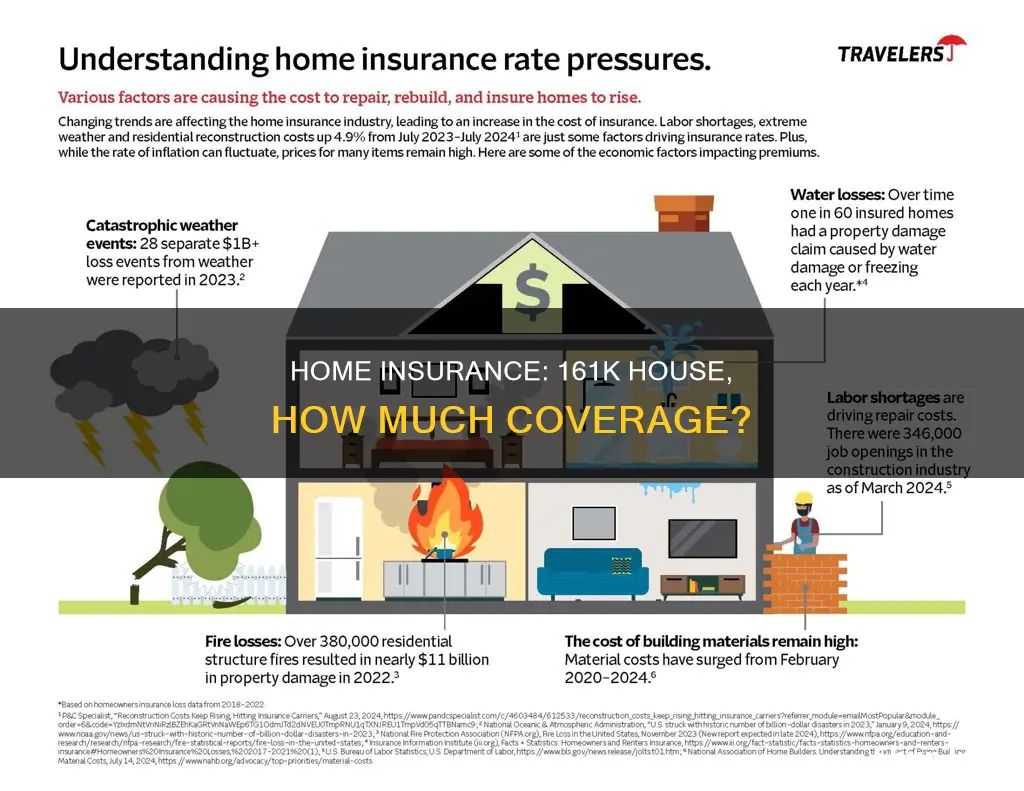

Location is one of the most significant factors influencing the cost of home insurance. Insurers perceive homes in areas prone to extreme weather, flooding, wildfires, or crime as riskier and, therefore, more expensive to insure. For example, coastal homes may be riskier to insure due to a higher likelihood of natural disasters. Additionally, areas with lower construction costs often have more favourable insurance rates.

The age of a home is another factor that affects insurance costs. Older homes often lack modern safety features, and repairs can be costly, leading to higher insurance rates. The construction materials used can also impact rates, with homes featuring materials that are less susceptible to fires and strong winds generally costing less to insure.

The size of a home is another consideration, as larger homes have higher insurance rates due to increased surface area that can be damaged or destroyed, resulting in higher repair and rebuilding costs.

Home insurance rates can also vary by city. For example, in 2025, Houston had the most expensive average rate at $6,370 per year, while San Jose, California, was the cheapest at $1,090 per year.

Additionally, factors such as an individual's credit history, claims history, and chosen deductible can influence the cost of home insurance. Shopping around and comparing quotes from multiple companies can help homeowners find the most affordable policy for their needs.

Homeowners vs Renters Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

The age of the house matters

The age of a house can also impact the rebuild value, which is a crucial factor in determining insurance rates. If the replacement cost of an older home exceeds its market value, specialised coverage or an HO-8 policy may be required. These policies are designed for older homes and may have lower dwelling coverage limits, but they can also be more affordable. Additionally, older homes built with rare or handmade materials can significantly increase the cost of rebuilding, leading to higher insurance rates.

The age of a house also influences the likelihood of certain risks, such as damage from wind, hail, or wildfires. Houses in areas prone to these environmental hazards will generally have higher insurance premiums. Similarly, the crime rate of a neighbourhood can affect insurance rates, with higher crime areas considered riskier and, therefore, more expensive to insure.

While the age of the house is a significant factor, it's important to note that location often plays a more prominent role in determining insurance rates. The cost of living in a particular area, the likelihood of natural disasters, and the distance from emergency services can all impact insurance premiums. Additionally, the size of the house and the amount of dwelling coverage needed will also affect the overall cost of homeowners insurance.

It's worth noting that insurance rates for older homes can be mitigated by making updates and remodelling to address safety concerns and modernise components. This can help reduce the risk of filing a claim and may result in lower insurance premiums over time.

How to Deduct Homeowners Insurance on Schedule 3

You may want to see also

Explore related products

![]()

The size of the house impacts the cost

The size of the house is a significant factor in determining the cost of homeowners insurance. Larger homes typically have higher insurance rates than smaller homes. This is because a bigger house means more surface area that can be damaged or destroyed during a covered event, resulting in higher repair and rebuilding costs.

The square footage of a house is a critical factor in calculating the cost of rebuilding or repairing it in the event of damage. A larger home will require more building materials and labour, driving up the overall cost. This is especially true if the house has high-end features, as the cost of replacing or repairing these features can be substantial.

The size of the house also affects the dwelling coverage needed. Dwelling coverage is the part of the insurance policy that pays for the rebuilding or repairing of the house's structure if it is damaged or destroyed. A larger house will require a higher dwelling coverage limit, which will increase the cost of the insurance policy.

Additionally, the size of the house can impact the likelihood of certain risks, such as injuries or accidents. For example, a larger house may have more rooms, stairs, or spaces where someone could trip and fall, increasing the potential liability for the homeowner.

It's important to note that the cost of homeowners insurance is influenced by various factors, including location, age of the house, credit score, and the deductible chosen. These factors, along with the size of the house, all contribute to the final insurance premium. Therefore, when considering the cost of homeowners insurance, it is essential to look at all these factors collectively to get an accurate estimate.

Home Insurance: Pools and Other Structures Coverage

You may want to see also

Explore related products

![]()

The type of roof affects the price

Roof Shape

The shape of a roof can affect its durability and resistance to wind and water damage. For example, roofs that slope on all four sides, such as hip roofs, are adept at withstanding high winds and storms, potentially resulting in lower insurance rates. Gable roofs, with two sloping sides forming a triangle, are cost-effective for areas less affected by high winds. Saltbox roofs can also resist wind and offer effective water shedding, potentially lowering insurance rates.

Roof Material

The material of a roof impacts its durability, resistance to damage, and maintenance requirements. Metal roofs are highly durable, fire-resistant, and can sustain high winds, making them a favorite among insurance providers. Slate roofs are resistant to fire, rot, insects, and require little maintenance. Tile roofs provide quality insulation and are resistant to rot and fire but can be more expensive and prone to breaking upon impact. Impact-resistant shingles, such as Class 4 asphalt shingles, can withstand hail and high winds, potentially reducing insurance costs. On the other hand, wood roofs are not fire-resistant and may require a fire retardant to be insurable, with some companies refusing to cover them.

Roof Age and Condition

Older roofs are more prone to damage and may require costly repairs or replacements, leading to higher insurance premiums. Insurance providers may inspect the roof's condition, looking for signs of deterioration, wear and tear, or water damage, which can increase the need for replacement. A well-maintained roof is likely to be viewed more favorably by insurance companies.

Geographical Location

The geographical location of a property influences the risk factors it faces, such as severe weather events like hurricanes, tornadoes, or hailstorms. Insurance companies consider the local climate and specific risks in an area to assess the likelihood of claims and set appropriate rates. For example, areas prone to severe weather may have higher insurance rates to account for potential roof damage.

While the type of roof is a significant factor in determining insurance rates, other factors also play a role, such as the coverage limits chosen, the home's location, age, size, and the cost of building materials. It is essential to consider all these factors when evaluating homeowners insurance costs.

Home Insurance: Does It Cover Broken Glass Doors?

You may want to see also

Explore related products

![]()

Crime rates in the area are a factor

Additionally, the proximity of your home to police stations, fire departments, and emergency services can impact your insurance expenses. Living farther away from emergency services may result in higher insurance premiums as the risk of severe damage in case of a fire or other incidents is greater.

The level of security and protective measures in your home can also influence insurance costs. Homes with security systems, smoke detectors, and fire alarms are considered safer, reducing the risks of theft and fire. Many insurance companies offer discounts to homeowners who invest in these safety features, resulting in lower premiums.

Your personal history of filing insurance claims is another factor that insurance companies consider. If you routinely file claims, your provider may view you as a higher risk and increase your premiums. The type of claims filed also matters; theft, water damage, and dog bite claims can significantly impact your policy rates.

Furthermore, the location of your home in relation to areas with high crime rates can affect insurance costs. If your home is situated in an area notorious for crime, theft, or natural disasters, your insurance costs may be higher due to the increased likelihood of filing a claim.

While crime rates are a factor, it's important to remember that insurance companies consider various other factors when determining your home insurance rate, such as the size and features of your home, the cost of rebuilding or repairing, and your personal credit history.

Florida's Home Insurance Crisis: What You Need to Know

You may want to see also

Frequently asked questions

The cost of homeowners insurance depends on various factors, including location, claims history, coverage limits, and the characteristics of your home. The national average cost of homeowners insurance is $2,466 per year for a policy with a $300,000 dwelling limit. To estimate the cost of insuring your $161k house, you can use online home insurance calculators. These tools will consider factors such as your location, the age and size of your home, and the coverage options you choose.

Many factors influence the cost of homeowners insurance. Here are some key considerations:

- Location: The location of your property plays a significant role in determining the cost of insurance. Factors such as crime rates, proximity to the coast, and the risk of natural disasters in your area can impact your insurance rates.

- Home characteristics: The construction materials, siding type, roofing type, and flooring materials of your home can affect its insurance cost. For example, homes with asphalt shingle roofs may have lower insurance costs due to their lower flammability risk.

- Coverage limits and deductibles: The amount of coverage you choose and your deductible level will impact your insurance rates. Higher coverage limits and lower deductibles typically result in higher insurance costs.

- Credit score: Homeowners with poor credit histories often pay more for home insurance than those with excellent credit.

- Safety features and age of the home: Older homes may cost more to insure if they lack modern safety features, as repairs can be more expensive.

You can use online home insurance calculators to get an estimate. These tools will ask you a series of questions about your property, location, and desired coverage options to provide you with an estimated insurance cost.

Dwelling coverage is a fundamental aspect of home insurance. It is the part of your policy that pays for the repair or rebuilding of your home if it is damaged or destroyed by a covered event, such as a fire or tornado. The amount of dwelling coverage you need will depend on the estimated cost of rebuilding your home. The higher the rebuilding cost, the higher your insurance rates are likely to be.

To get the best rate, it is recommended to shop around and compare quotes from multiple insurance companies. Bundling your home and auto insurance policies with the same company can often result in significant discounts. Additionally, consider the following:

- Raise your deductible: Increasing your deductible can lower your insurance premiums. However, weigh this option carefully, as a higher deductible means you'll pay more out of pocket if you need to make a claim.

- Review your coverage options: Evaluate the coverage options carefully and choose those that are most relevant to your needs. You may not need all the available coverages, and eliminating unnecessary ones can reduce your overall cost.