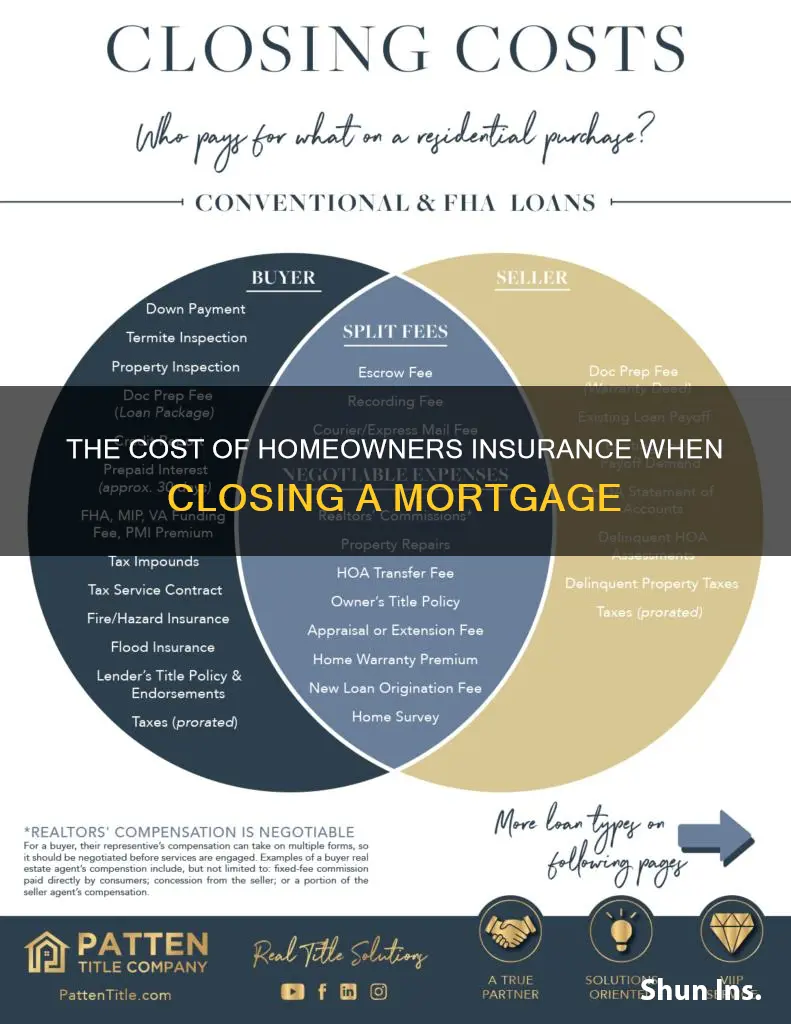

When it comes to closing on a new home, there are a multitude of costs to consider, including homeowners insurance. This insurance is an essential requirement for nearly all mortgage lenders before closing on a home, as it helps to protect both the lender and the buyer. The cost of insurance will depend on a variety of factors, including the value of the home, the location, and the coverage type. While the cost of homeowners insurance can vary, it is typically paid annually and upfront at closing, with the option to pay monthly thereafter. This upfront payment ensures that the investment is protected from any unforeseen events from the moment the buyer becomes a homeowner.

| Characteristics | Values |

|---|---|

| When is homeowners insurance paid? | Homeowners insurance is typically paid annually and upfront at closing. |

| What is the purpose of paying in advance? | Paying in advance ensures that when the bill is due, the money is already there. |

| What is the role of escrow accounts? | Escrow accounts are used by the lender to pay insurance and taxes on the buyer's behalf. They also help the buyer stay on top of their house payments. |

| What is the minimum requirement for homeowners insurance? | At a minimum, homeowners insurance should cover the cost of rebuilding the home in case of total loss or the loan balance, whichever is less. |

| What factors determine the insurance premium? | Insurers consider the property value, location, credit score, claims history, and coverage type and amount to determine the premium. |

| Can the insurance provider be changed after closing? | Yes, the insurance provider can be changed after closing, but the lender must be informed, and there should be no lapse in coverage. |

| What happens if insurance is not obtained before closing? | Lacking homeowners insurance at closing can delay or even cancel the transaction. |

| How can the insurance premium be calculated? | A mortgage calculator with PMI, taxes, insurance, and closing costs can help estimate the premium. |

Explore related products

What You'll Learn

![]()

Homeowners insurance is a requirement for mortgage lenders

The amount you pay for homeowners insurance depends on various factors, including the value of the home and its location. Insurers will consider the susceptibility of the home to natural disasters, as well as your credit score and claims history. A higher credit score and a clean claims history may help to reduce costs. The more comprehensive the coverage you need, the higher the premium costs will be.

Homeowners insurance premiums are generally paid annually. At closing, you will typically be required to pay the first year's premium upfront. If you have an escrow account, your lender will pay your first year's premium through this account. If you don't have an escrow account, you'll need to show proof that you've paid your first year's insurance premium at closing.

It's important to note that you'll need to meet the minimum coverage requirements set by your lender. This typically includes coverage for fire, wind, and theft, as well as 100% of the replacement cost value of the home. If you're underinsured, your lender will require you to increase your coverage before closing. Additionally, if you buy a home in a flood zone, you may need to purchase additional flood insurance.

While homeowners insurance is not required by law, it is a necessary step to secure a home loan from a mortgage lender. By understanding the role of homeowners insurance in the home-buying process, you can be prepared to handle this expense at closing and ensure a smooth transaction.

HOA Members: Must You Get Earthquake Insurance?

You may want to see also

Explore related products

![]()

You can change your insurance provider after closing

When buying a home, there are several costs to consider, including the closing costs. Closing costs are associated with securing a mortgage loan, and they include prepaid costs like homeowners insurance and taxes. These prepaid costs are typically required by the lender to protect their investment. While the exact amount can vary, it is generally recommended to have at least 12 months' worth of homeowners insurance premiums prepaid at closing. This is usually done through an escrow account, where the lender pays the insurance premiums on your behalf.

Now, let's address the question: "Can you change your insurance provider after closing?" The answer is yes! You are not locked into your insurance provider forever just because you chose them at closing. You can change your home insurance provider at any time, but there are a few things to keep in mind. Firstly, check if your claim is still "open" or unresolved. If it is, you may need to wait until it's closed before switching providers. Additionally, switching providers before your policy's renewal date may incur a cancellation fee from your current insurer. It's also important to ensure that your new policy meets your mortgage lender's requirements.

When considering switching insurance providers, it's essential to shop around for quotes and compare coverages, limits, and deductibles. Affordability is crucial, but it's also important to evaluate how well the insurance company handles claims and whether they offer additional features like a mobile app. You may also want to look for discounts, such as bundling home and auto insurance, which can provide significant savings. Remember, it's your choice to switch insurance providers, and you can do so whenever you find a better deal or if you're unhappy with your current provider's service.

Once you've decided to switch insurance providers, there are a few steps to take. First, purchase your new policy and schedule its start date. Then, contact your former insurer to cancel your old policy. You may be eligible for a refund for any unused portion of your policy, minus any cancellation fees. Your new insurance company can provide proof of insurance to your old company if needed, but they typically cannot cancel the previous policy on your behalf. It's also a good idea to review your policy regularly, at least once a year, to ensure you're getting the best value for your budget.

In conclusion, while closing costs may include prepaid homeowners insurance premiums, you are not tied to that insurance provider for the long term. You have the flexibility to change providers whenever you like, although there may be some fees and considerations depending on the timing. By regularly reviewing your policy and exploring alternative options, you can ensure that you're getting the best value and service to protect your valuable investment—your home.

Reporting Insurance Fraud in Ohio: What You Need to Know

You may want to see also

Explore related products

![]()

Closing costs include insurance and taxes

Closing costs are the fees you pay when you officially become the owner of a house. They are typically associated with securing a mortgage loan. Closing costs include insurance and taxes, which are prepaid costs that you would have to pay with or without a loan.

Homeowners insurance is an essential requirement for nearly all mortgage lenders before closing on a home. Lenders require proof of insurance to protect their investment. The insurance helps to protect both the lender and the buyer in the event of unforeseen circumstances. The cost of insurance is determined by factors such as the value and location of the home, credit score, and claims history.

If you have a mortgage, you will likely be required to pay your first year's homeowners insurance premium before or at closing. This is done to protect the lender's investment, as they will not recoup their money without insurance if the home is destroyed. You can pay this upfront cost with or without an escrow account. An escrow account is used by the lender to pay your insurance and taxes on your behalf, and it can make tracking payments easier.

In addition to the first year's premium, you may also need to pay a few months' worth of insurance into your escrow account, depending on the closing date. This is because the first payment to the mortgage company is usually not due until at least one month after closing, so additional insurance is paid upfront to ensure coverage until the first payment date.

It is important to shop around for insurance quotes and understand your coverage needs before closing on a home. Your lender can provide guidance on the required coverage amounts, and it is crucial to provide all necessary insurance documents ahead of time to avoid delays in the closing process.

Moving Truck Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Shop around for insurance quotes before closing

When buying a home, it is essential to consider the various costs involved, including homeowners insurance. While not legally required in any state, homeowners insurance is typically mandated by mortgage lenders to protect their investment. As such, it is crucial to factor this into your closing costs.

To ensure you get the best deal, it is recommended to shop around for insurance quotes before closing on your new home. Starting this process about a month before closing gives you ample time to compare different insurers and evaluate your coverage options. By using an online quoting tool, you can easily compare multiple policies at once. Additionally, filling out an online questionnaire through an insurance marketplace platform can streamline the process, as they will connect you with agents offering customised policies based on your needs and budget.

When gathering quotes, you will need to provide prospective insurers with specific information about the home, including its age, address, roof condition, and the number of occupants. It is also essential to ensure that the policy you choose meets your lender's requirements for scope and amount of coverage. Ask for clarification from your lender if you are unsure about their specific requirements.

Remember, even if you pay for homeowners insurance through an escrow account, you have the freedom to switch policies if you find a more suitable deal. Simply cancel your existing policy, inform your lender about the change, and they will redirect your escrow payments to your new insurance company. However, always ensure that you have proof of insurance before closing, as this is typically required by lenders several days to two weeks before the closing date.

By shopping around for insurance quotes and taking advantage of early bird discounts, you can make informed decisions and optimise your coverage while managing the financial aspects of closing on your new home effectively.

Navigating Pet Insurance: A Guide to Understanding Farmers' Quotes

You may want to see also

Explore related products

![]()

Your insurance premium is determined by property value and location

When it comes to purchasing a home, there are numerous costs to consider, including homeowners insurance. This type of insurance is mandatory for anyone financing a house and is highly recommended for all homeowners to protect their property and possessions. The premium, or cost, of homeowners insurance is influenced by various factors, with property value and location being two key determinants.

Property value is a crucial factor in determining homeowners insurance premiums. However, it is important to distinguish between market value and replacement cost. Market value, also known as actual cash value, refers to the current selling price of the property, taking into depreciation into account. On the other hand, replacement cost is the estimated expense of rebuilding the home from the ground up, encompassing construction and labour costs. While market value is generally unrelated to insurance premiums, replacement cost is a fundamental factor in calculating them. This is because the replacement cost reflects the amount of money an insurance company would need to pay out if the home were destroyed, ensuring that the homeowner can rebuild.

The location of the property also plays a significant role in determining homeowners insurance premiums. Certain locations may be more prone to specific risks, such as floods or earthquakes, which necessitate additional coverage. Furthermore, the cost of labour and materials can vary depending on the geographical area, impacting the overall rebuilding expense. Location can also influence the market value of a property, but this does not directly affect insurance premiums in the same way as replacement cost.

When calculating homeowners insurance premiums, insurance providers will consider the replacement cost of the property, including the cost of rebuilding the dwelling and any additional structures, as well as the value of personal belongings. They will also take into account the location-specific risks and the prevailing labour and material costs in that area. By combining these factors, insurance companies can establish appropriate coverage limits and premiums for homeowners.

It is worth noting that, in addition to property value and location, there are other factors that can influence homeowners insurance premiums. These may include the age, condition, size, and building materials of the home, as well as any improvements or upgrades made to the property. Furthermore, the type of coverage selected, such as liability coverage or additional endorsements, can also impact the premium. Homebuyers should consult with insurance agents and utilise online tools to obtain accurate estimates and ensure they have adequate coverage for their specific needs.

Homeowner's Insurance: What Happens When You Sell?

You may want to see also

Frequently asked questions

Yes, homeowners insurance is included in closing costs. It is a prepaid cost that you would have to pay with or without a loan.

At a minimum, your homeowner's insurance should cover the cost of rebuilding the home in case of total loss or the loan balance, whichever is less. Your insurance policy must cover 100% of the replacement cost value of the improvements.

If your insurance is escrowed, the annual premium is divided by twelve to get your monthly insurance payments. This is then added to your monthly mortgage payment.

Yes, you may change your insurance provider after closing. However, you must keep your lender informed and ensure there is no lapse in coverage.

Shop around for insurance quotes from multiple homeowners insurance providers to find the best rates and coverage options.