The cost of health insurance is a significant expense for many people, and it can be challenging to determine how much to budget for it. The amount you pay for health insurance depends on various factors, including your age, location, income, health status, and the type of plan you choose. Understanding these factors is crucial for making informed decisions about your healthcare coverage. In addition, the availability of subsidies and tax credits can significantly impact the affordability of health insurance plans.

| Characteristics | Values |

|---|---|

| Average annual health insurance cost | $7,080 for ACA marketplace plans |

| Average monthly health insurance cost | $445 for a single 21-year-old, $467 for a single 27-year-old, $505 for a single 30-year-old, $618 for a 30-year-old, and $1,478 for a 60-year-old |

| Premium for ACA health insurance plan | $590 per month |

| Average Bronze plan cost | $495 per month |

| Average Silver plan cost | $618 per month |

| Average Gold plan cost | $655 per month |

| Average Platinum plan cost | $1,166 per month |

| Average annual health insurance premiums in 2024 | $8,951 for single coverage and $25,572 for family coverage |

| Average annual premiums for covered workers in HDHP/SOs | $8,275 for single coverage and $24,196 for family coverage |

| Average premiums for covered workers in PPOs | $9,383 for single coverage and $26,678 for family coverage |

| Average premium for covered workers with both single and family coverage | Relatively higher in the Northeast and relatively lower in the South |

| Average premiums for covered workers at firms with a large share of older workers | $9,171 for single coverage |

| Average premiums for covered workers at firms with a smaller share of older workers | $8,738 for single coverage |

| Average premiums for covered workers at private for-profit firms | Lower |

| Average premiums for covered workers at private not-for-profit firms | Higher |

| Factors influencing health insurance costs | Age, location, income, and plan type |

| Health Insurance Marketplace Calculator | Provides estimates of health insurance premiums and subsidies for people purchasing insurance on their own |

Explore related products

![]()

Income-based subsidies

The first type of financial assistance offered by the ACA is the premium tax credit, which reduces monthly payments for insurance coverage. This credit limits an individual's contribution towards the premium of the "benchmark" plan, typically the second-lowest-cost silver plan in their Marketplace. The required individual contribution is set on a sliding income scale. For instance, in 2025, individuals with income up to 150% of the Federal Poverty Level (FPL) have a zero-required contribution, while those at 400% FPL or above contribute 8.5% of their household income.

The second type of financial assistance is the cost-sharing reduction (CSR), which decreases out-of-pocket expenses such as deductibles when individuals seek medical services. These subsidies are essential in making health insurance more accessible and affordable for people from diverse economic backgrounds.

Eligibility for income-based subsidies depends on several factors, including income, family size, age, and access to employer-sponsored coverage or Medicaid. In most states, individuals with income not exceeding 138% of the poverty level are eligible for Medicaid. Additionally, recent immigrants with income below the poverty level may also qualify for premium subsidies, even if they have been in the country for less than five years and do not qualify for Medicaid.

To determine eligibility and estimate potential subsidies, individuals can use tools like the Health Insurance Marketplace Calculator. This calculator considers factors such as income, age, and family size to provide an estimate of eligibility and potential costs for health insurance. However, it is important to note that eligibility requirements may vary by state, and individuals should refer to their state's specific guidelines and resources for more accurate information.

Disability and Insurance: Keeping Medical Cover Short-Term

You may want to see also

Explore related products

![]()

Age-based premiums

Age is a significant factor in determining health insurance premiums. While age-based premiums are not considered when setting rates for employer-sponsored health insurance, insurers in the ACA marketplace use age to set health plan premiums. Federal rules allow insurers to charge older adults (typically those in their sixties) up to three times the premium charged to younger adults (usually those in their early twenties). This federal limit on age rating ensures that people aged 64 and above do not pay more than three times the base rate. Once an individual turns 65, they typically transition from private health insurance to Medicare coverage.

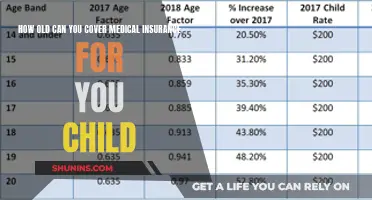

The cost of health insurance varies with age, with rates increasing as individuals advance in years. For instance, the average monthly health insurance cost for a single 21-year-old is $445, while it increases to $467 for a 27-year-old and $505 for a 30-year-old. The average cost at age 24 is $486 per month, and by age 26, it averages $498 per month. The cost of health insurance for a 40-year-old is approximately $621 per month, representing a 27.8% increase compared to the base rate.

The expense of health insurance starts to surge significantly in the fifties, with rates more than 75% higher than the base rate. At age 50, the average monthly cost is $868, surpassing $1,000 per month by age 54. The average monthly cost at age 55 is $1,084, and it continues to rise with age, reaching $1,319 at age 60, $1,396 at age 62, and $1,458 at age 64. The cost at age 65 averages $1,458 per month, similar to the previous year.

It is worth noting that the cost of health insurance for children is generally lower. The average cost of health insurance for children aged 14 and younger is $372 per month, which is 23.5% cheaper than the base rate. However, rates start to increase from age 15 onwards. Additionally, it is important to remember that age-based premiums are not the sole factor influencing health insurance costs. Other factors, such as location, family size, tobacco use, and plan category, also play a role in determining the final premium amount.

Vehicle Insurance: Medical Expense Coverage Explained

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Plan types

HMO (Health Maintenance Organization)

An HMO is a health plan that provides prepaid comprehensive medical care. HMOs both insure and deliver health services, and patients must typically receive non-emergency services within the HMO's network of healthcare providers and facilities. An open-access HMO will cover non-emergency care outside of this network for an extra cost.

PPO (Preferred Provider Organization)

A PPO is a health plan that contracts with medical providers to create a network. Patients pay less if they use providers within this network but can use out-of-network providers for a higher cost.

EPO (Exclusive Provider Organization)

An EPO is a health plan that comprises a group of hospitals and doctors that contract to provide comprehensive medical services. Patients receive coverage only from these providers, except in emergencies.

POS (Point-of-Service Plan)

A POS plan typically has several reimbursement levels depending on where enrollees receive services. Patients pay less if they use providers within the plan's network.

FSA (Flexible Spending Account)

An FSA is a type of savings account that allows you to set aside pre-tax dollars to pay for qualified medical expenses.

Fee-for-Service

A fee-for-service plan gives participants the same reimbursement regardless of the hospital or care provider they choose.

In addition to these types, there are also bronze, silver, gold, and platinum plans, with bronze offering the least coverage and platinum the most. If you are under 30, you may be eligible for a high-deductible, catastrophic plan. These plans have lower monthly premiums but higher out-of-pocket costs.

It is also worth noting that short-term health plans are available, which fall outside of ACA rules and generally do not cover pre-existing conditions.

When choosing a plan, it is important to consider your healthcare needs and whether you may need to use out-of-network services.

Understanding the End Date of Your Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Location

The cost of health insurance is dependent on a variety of factors, one of which is location. In the United States, the average national monthly health insurance cost for one person on an Affordable Care Act (ACA) plan without premium tax credits in 2024 is $477. This figure is an average, and the cost of health insurance varies by state.

The cost of health insurance in the ACA marketplace at HealthCare.gov differs based on where you live, the insurance company, the plan and metal tier you choose, how many people are covered, your age, and whether you smoke. For example, the average monthly health insurance cost is $445 for a single 21-year-old, $467 for a single 27-year-old, and $505 for a single 30-year-old. As people age, the cost of health insurance typically increases, with rates rising faster when individuals reach their 50s and 60s.

The impact of location on health insurance costs is influenced by the level of competition in a particular area. Additionally, the cost of living in a specific location can affect health insurance prices, as higher costs of living may result in higher insurance premiums.

It is worth noting that some states, such as New York and Vermont, do not consider age when determining health insurance premiums. However, age is a significant factor in most states, with the base age of 21 being used to adjust premium costs upwards for older individuals.

Furthermore, employer-sponsored health insurance coverage may also be influenced by location. Organizations with employees in multiple locations may need to consider varying contribution strategies and minimum percentage requirements for each state or region.

Teachers' Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

$8.99 $14.99

$13.1 $19.99

![]()

Tax credits

The Premium Tax Credit is a refundable tax credit that helps eligible individuals and families with low or moderate incomes afford health insurance purchased through the Health Insurance Marketplace (also known as the Exchange). The size of the Premium Tax Credit is based on a sliding scale, meaning that those with lower incomes receive a larger credit to help cover the cost of their insurance. The credit is available immediately upon enrollment in an insurance plan, and people can choose to have payments go directly to insurers to cover a share of their monthly health insurance premiums.

To receive a premium tax credit, individuals must be U.S. citizens or lawfully present in the United States. They cannot receive the credit if they are eligible for other "minimum essential coverage," including Medicare, Medicaid, or employer-sponsored coverage. The credit is available to individuals and families with incomes at or above the federal poverty level who purchase coverage in the ACA marketplace in their state. For example, for 2025, an individual would need an income of at least $15,060, while a family of four would need an income of at least $31,200.

The amount of the Premium Tax Credit is generally equal to the premium for the second-lowest-cost silver plan available through the Marketplace, minus a certain percentage of the enrollee's household income. The credit cannot be more than the premiums for the Marketplace plan or plans in which the enrollee or their family enrolls. The enrollee's expected contribution is generally between 2% and 9.5% of their income. For example, an individual with an annual income of $30,120 (200% of the poverty line) would have an expected contribution of 2% of their income, or $602 per year.

When enrolling in Marketplace insurance, individuals can choose to have the Marketplace compute an estimated credit that is paid to their insurance company to lower their monthly premiums, or they can choose to get the full benefit of the credit when they file their tax return for the year. If an individual chooses to receive advance payments of the Premium Tax Credit, they will need to reconcile the amount paid in advance with the actual credit computed when they file their tax return for the year. This is done using IRS Form 8962, which compares the advance amount used to the amount the individual qualifies for based on their final income. If the individual used too much credit, they will repay it via taxes, and if they used too little, they can claim the difference as a credit.

Access Card Usage for Medical Insurance: What You Need to Know

You may want to see also

Frequently asked questions

The average annual health insurance cost is $7,080 for ACA marketplace plans. The average monthly cost is $445 for a single 21-year-old, $467 for a single 27-year-old, and $505 for a single 30-year-old. The cost of health insurance depends on factors such as age, location, income, and plan type.

The cost of health insurance is influenced by several factors, including age, location, income, and plan type. Older individuals tend to pay more for health insurance than younger people. The cost of health insurance also varies by location, with areas like New York or California typically having higher insurance costs. Income impacts eligibility for subsidies, with lower incomes qualifying for reduced premiums and out-of-pocket costs. Different plan types, such as HMOs, PPOs, and HDHPs, offer varying levels of coverage and flexibility, which affect the overall cost.

The Health Insurance Marketplace categorizes plans into four tiers: Bronze, Silver, Gold, and Platinum. Bronze plans typically have the lowest premiums but the highest out-of-pocket costs, making them suitable for individuals who rarely need medical care. Silver plans offer a balance between premiums and out-of-pocket expenses and are ideal for those with moderate healthcare needs. Gold plans have higher premiums but lower out-of-pocket costs, suitable for those requiring frequent medical care. Platinum plans have the highest premiums but provide the lowest out-of-pocket costs, catering to individuals with extensive medical needs.

The cost of health insurance can be calculated using tools such as the Health Insurance Marketplace Calculator. This calculator estimates health insurance premiums and subsidies based on factors such as income, age, and family size. It helps determine eligibility for subsidies and provides an estimate of how much an individual may spend on health insurance.

Coinsurance is a percentage of the covered amount that enrollees may be required to pay instead of a copay. It is typically around 20% of the covered amount. Plans with lower out-of-pocket maximums tend to have higher premiums, while plans with higher out-of-pocket maximums usually have lower premiums.