Shopping for health insurance can be a daunting task, but understanding your needs and options is crucial to finding the right plan. Start by assessing your current health status, anticipated medical expenses, and budget to determine the level of coverage you require. Familiarize yourself with key terms like premiums, deductibles, copayments, and out-of-pocket maximums, as these will impact your overall costs. Compare plans from different providers, considering factors such as network coverage, prescription drug benefits, and additional services like mental health or maternity care. Utilize online tools, insurance marketplaces, or consult with a licensed broker to explore available options and ensure you’re getting the best value for your money. Finally, read the fine print carefully to avoid surprises and choose a plan that aligns with your health and financial goals.

Explore related products

What You'll Learn

- Assess Your Needs: Evaluate health, family, and financial situation to determine coverage requirements

- Understand Plan Types: Compare HMOs, PPOs, EPOs, and HDHPs for best fit

- Check Network Coverage: Ensure preferred doctors, hospitals, and specialists are in-network

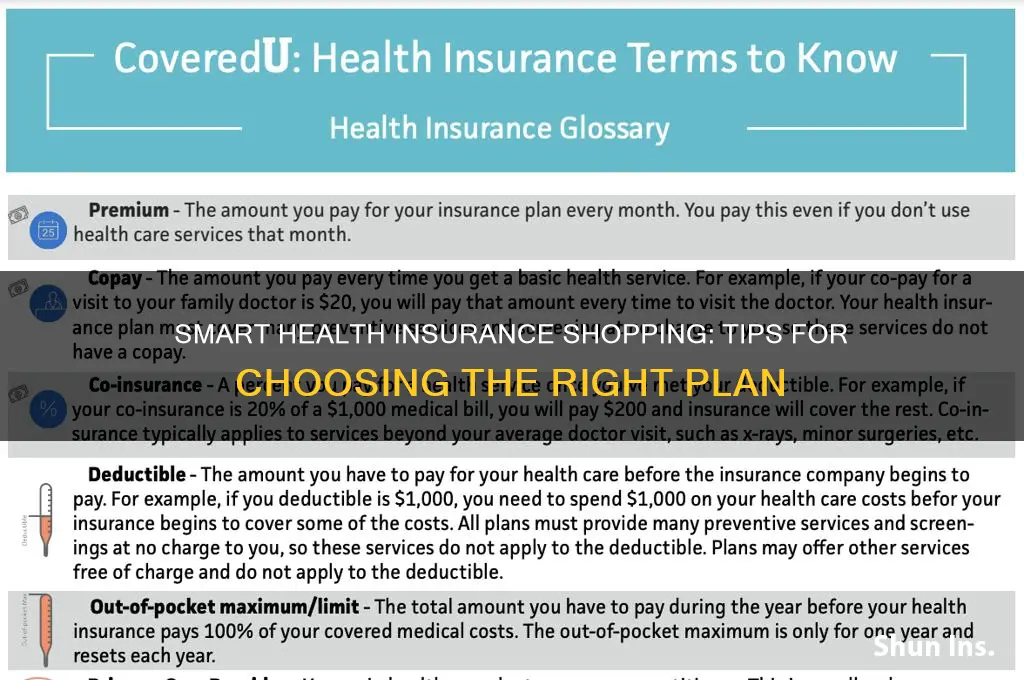

- Review Costs: Analyze premiums, deductibles, copays, and out-of-pocket maximums

- Verify Prescription Coverage: Confirm medications are covered under the plan’s formulary

![]()

Assess Your Needs: Evaluate health, family, and financial situation to determine coverage requirements

Before diving into the maze of health insurance plans, pause and take stock of your life. Your health, family dynamics, and financial landscape are the compass points that will guide you to the right coverage. Think of this as a personal audit, where every detail matters—from your age and medical history to your dependents and budget. Skipping this step is like navigating a forest without a map; you might find a path, but it’s unlikely to be the one tailored to your needs.

Start with your health. Are you in your 20s with no chronic conditions, or are you managing diabetes in your 50s? A young, healthy individual might prioritize low premiums and high deductibles, while someone with ongoing medical needs may require a plan with lower out-of-pocket costs and comprehensive prescription coverage. For instance, if you take a daily medication like metformin, ensure the plan covers it under Tier 1 or 2 to avoid paying full price. Don’t forget preventive care—if you’re due for screenings like mammograms or colonoscopies, confirm the plan covers these at 100%.

Next, consider your family. Are you single, married, or have children? A family plan often makes sense if you have dependents, but compare it to individual plans for each member. Sometimes, separate policies can be more cost-effective, especially if one person has significant health needs. For example, a spouse with a pre-existing condition might benefit from a plan with robust specialist coverage, while a healthy child could be on a lower-cost HMO. Also, factor in life stage changes—are you planning to expand your family? Maternity care and pediatric services become critical in such cases.

Finally, align your financial situation with your coverage choices. Health insurance isn’t just about monthly premiums; it’s about managing risk. If you have a high-deductible plan, can you afford to pay $5,000 out of pocket in an emergency? If not, consider a plan with higher premiums but lower deductibles. Use tools like Health Savings Accounts (HSAs) if you choose a high-deductible plan—they offer tax advantages and can help you save for medical expenses. Conversely, if you rarely visit the doctor, a catastrophic plan might suffice, but ensure it meets the minimum essential coverage requirements to avoid tax penalties.

The takeaway? Your health insurance shouldn’t be a one-size-fits-all solution. By meticulously evaluating your health, family, and finances, you can pinpoint the coverage that balances protection and affordability. It’s not just about finding a plan—it’s about finding *your* plan.

Why Insurance Covers Chiropractic Care: Benefits and Reasons Explained

You may want to see also

Explore related products

![]()

Understand Plan Types: Compare HMOs, PPOs, EPOs, and HDHPs for best fit

Choosing the right health insurance plan requires understanding the distinct structures of HMOs, PPOs, EPOs, and HDHPs. Each type offers a unique balance of cost, flexibility, and provider access, making the decision highly personal. HMOs (Health Maintenance Organizations) typically require you to select a primary care physician who coordinates all your care, including referrals to specialists. This model emphasizes preventive care and cost control but limits your ability to see out-of-network providers without significant out-of-pocket costs. If you value a streamlined, cost-effective approach and don’t mind staying within a network, an HMO might be your best fit.

PPOs (Preferred Provider Organizations) offer more flexibility by allowing you to see any provider, in-network or out, without a referral. While this freedom is convenient, it comes at a higher premium and often requires higher out-of-pocket costs for out-of-network care. PPOs are ideal for those who prioritize choice and are willing to pay more for it. For instance, if you frequently travel or prefer specific specialists outside a typical network, a PPO could save you from unexpected expenses down the line.

EPOs (Exclusive Provider Organizations) combine elements of HMOs and PPOs but with a critical limitation: they do not cover out-of-network care except in emergencies. Like HMOs, EPOs require you to use in-network providers, but they often don’t require referrals to see specialists. This plan suits individuals who want lower premiums than a PPO but are comfortable staying within a specific network. For example, if you live in an area with a robust network of providers, an EPO can offer significant savings without sacrificing quality care.

HDHPs (High Deductible Health Plans) pair with Health Savings Accounts (HSAs) and are designed for those who want to pay lower monthly premiums in exchange for higher out-of-pocket costs before coverage kicks in. These plans are ideal for healthy individuals or families who rarely need medical care beyond preventive services, which are typically covered at no cost. For instance, a 30-year-old with no chronic conditions might save hundreds annually by choosing an HDHP and contributing to an HSA for tax advantages. However, if you require frequent medical attention, the high deductible could negate the savings.

When comparing these plans, consider your health needs, budget, and provider preferences. For example, a family with young children might prefer a PPO for its flexibility, while a healthy single professional could benefit from an HDHP’s lower premiums. Always review the plan’s Summary of Benefits and Coverage (SBC) to understand copays, deductibles, and out-of-pocket maximums. By aligning your choice with your lifestyle and medical history, you can ensure your health insurance plan provides the best value and protection.

Medical Insurance Tax Deductions: What Canadians Need to Know

You may want to see also

Explore related products

$31.1 $245.95

$80.93 $92.95

![]()

Check Network Coverage: Ensure preferred doctors, hospitals, and specialists are in-network

Choosing a health insurance plan without verifying network coverage is like buying a car without checking if it fits your garage. In-network providers—doctors, hospitals, and specialists—have pre-negotiated rates with your insurer, slashing out-of-pocket costs dramatically. Out-of-network care, on the other hand, can trigger higher deductibles, coinsurance, or even full payment responsibility. For example, a routine MRI might cost $500 in-network but soar to $2,000 out-of-network. Before enrolling, cross-reference your insurer’s provider directory with your preferred healthcare professionals. If your trusted cardiologist isn’t listed, ask if they plan to join the network soon or if exceptions can be made for continuity of care.

Consider this scenario: A family in Texas discovered their pediatrician wasn’t in-network after their child needed urgent care. The $300 visit became a $700 bill, plus a denied claim. To avoid such pitfalls, use the insurer’s online tools or call their customer service to confirm coverage. Pay attention to tiers within networks—some plans label providers as "preferred" or "participating," which can affect costs even within the network. If you’re switching insurers, don’t assume your current providers will carry over. Proactively update your list of preferred doctors and verify their status before open enrollment ends.

For those with chronic conditions or specialized care needs, network coverage isn’t just a detail—it’s a lifeline. A patient with diabetes, for instance, relies on endocrinologists, dietitians, and labs. If any of these specialists fall outside the network, managing the condition becomes financially unsustainable. Some insurers offer narrow networks with lower premiums but limited provider choices, while others provide broader networks at higher costs. Weigh your health needs against your budget: If you rarely see specialists, a narrow network might suffice. But if you require frequent, specific care, prioritize plans with robust in-network options.

Here’s a practical tip: If you’re torn between plans, create a spreadsheet listing your current providers and their network status under each option. Include columns for premiums, deductibles, and estimated annual costs based on your typical healthcare usage. This visual comparison highlights trade-offs between cost and access. Additionally, don’t overlook "network adequacy" laws in your state, which require insurers to maintain a minimum number of providers within a reasonable distance. If you live in a rural area, this is especially critical—a "broad" network might still leave you hours away from the nearest in-network specialist.

Finally, remember that networks aren’t static. Providers join or leave networks annually, so recheck coverage during each open enrollment period. Some insurers allow appeals for out-of-network providers under specific circumstances, such as lack of in-network specialists for your condition. Document these conversations and keep records of any promises made by customer service representatives. By treating network coverage as a non-negotiable priority, you’ll avoid unexpected costs and ensure seamless access to the care you need.

Top UK Insurance Giants: Leading Companies Dominating the Market

You may want to see also

Explore related products

![]()

Review Costs: Analyze premiums, deductibles, copays, and out-of-pocket maximums

Understanding the financial structure of health insurance plans is crucial, as costs can vary widely and impact your budget significantly. Premiums, deductibles, copays, and out-of-pocket maximums are the four pillars of health insurance expenses, each playing a distinct role in how much you’ll pay for coverage and care. Start by comparing premiums—the monthly or annual fee for your plan—but don’t stop there. A lower premium might seem appealing, but it often comes with higher out-of-pocket costs when you need care. Conversely, a higher premium plan may offer lower deductibles and copays, making it more cost-effective if you anticipate frequent medical visits.

Next, dissect deductibles, the amount you pay out of pocket before insurance kicks in. Plans with high deductibles, often $1,000 or more for individuals and $2,000+ for families, can be risky if you have limited savings. For example, a 30-year-old with no chronic conditions might opt for a high-deductible plan to save on premiums, but a sudden injury could lead to unexpected financial strain. On the other hand, low-deductible plans may be better for those with ongoing health needs, like a 50-year-old managing diabetes, who requires regular doctor visits and prescriptions.

Copays, fixed fees for specific services like doctor visits or prescriptions, are another critical factor. While a $20 copay for a primary care visit may seem minor, specialty visits or urgent care copays can be significantly higher, ranging from $50 to $100 or more. Analyze your typical healthcare usage: if you visit the doctor once a year, a higher copay might be acceptable, but frequent users should prioritize plans with lower copays. Prescription copays, often tiered by drug type, can also add up quickly, especially for brand-name medications.

Finally, out-of-pocket maximums cap your total annual expenses for covered services, typically ranging from $2,000 to $8,000. This is your financial safety net—once reached, the insurance covers 100% of costs. For instance, a family with a $6,000 out-of-pocket maximum knows their worst-case scenario for medical expenses in a year. When comparing plans, consider your health history and risk tolerance: a lower out-of-pocket maximum provides more protection but often comes with higher premiums.

To make an informed decision, create a cost scenario based on your expected healthcare needs. For example, if you anticipate two doctor visits, one specialist visit, and generic prescriptions annually, calculate the total costs under different plans. Factor in potential emergencies or unexpected illnesses to ensure you’re not blindsided by expenses. Tools like healthcare.gov’s plan comparison feature or insurance broker calculators can simplify this analysis. Ultimately, balancing premiums, deductibles, copays, and out-of-pocket maximums requires aligning your financial priorities with your health needs, ensuring you’re neither overpaying nor underinsured.

Medical Insurance Abroad: Cigna's Global Coverage Explained

You may want to see also

Explore related products

![Consumers shopping guide for automobile insurance / [State of New York, Insurance Department] 1976 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Verify Prescription Coverage: Confirm medications are covered under the plan’s formulary

Prescription medications can be a significant expense, often representing a critical component of healthcare costs. When shopping for health insurance, it’s essential to verify that your current or anticipated medications are covered under the plan’s formulary—the list of drugs the insurer agrees to pay for. Failing to do this can lead to unexpected out-of-pocket costs, especially for specialty drugs or brand-name medications. For example, a 30-day supply of a common cholesterol-lowering statin might cost $10 under one plan but $50 under another if it’s not on the formulary. Start by compiling a list of all medications you or your dependents take, including dosage and frequency, and cross-reference this with the plan’s formulary document, typically available on the insurer’s website.

Analyzing the formulary requires attention to detail. Plans often categorize drugs into tiers (e.g., Tier 1 for generics, Tier 4 for specialty drugs), with higher tiers costing more. A medication like insulin, for instance, might be in Tier 2 under one plan but Tier 3 under another, doubling your copay. Additionally, some plans require prior authorization or step therapy, where you must try a lower-cost drug first before the insurer covers a more expensive option. For older adults or those with chronic conditions, this can delay necessary treatment. Use the plan’s drug cost estimator tool, if available, to compare costs across different insurers. If a medication isn’t covered, ask if exceptions can be made or if there’s a therapeutically equivalent alternative on the formulary.

Persuasively, verifying prescription coverage isn’t just about cost—it’s about continuity of care. Switching medications due to insurance limitations can disrupt treatment, especially for conditions like epilepsy or depression, where consistency is critical. For families with children, ensure vaccines and age-specific medications (e.g., ADHD treatments) are covered. If you’re considering a high-deductible plan, note that prescriptions may not be covered until the deductible is met, which could mean paying full price for drugs like asthma inhalers ($200–$300 per month) until then. Prioritize plans that cover your medications in lower tiers or offer deductible exemptions for maintenance drugs.

Comparatively, employer-sponsored plans often have more comprehensive formularies than individual market plans, but this isn’t always the case. If you’re self-employed or shopping on the marketplace, look for plans labeled as “gold” or “platinum,” which typically have broader prescription coverage but higher premiums. Conversely, “bronze” plans may exclude expensive medications altogether. For those on Medicare, Part D prescription drug plans vary widely—use the Medicare Plan Finder to compare formularies and costs. Don’t assume all plans cover the same drugs; even within the same insurer, different plans can have distinct formularies.

Practically, keep a record of your formulary checks and any exclusions you discover. If a plan doesn’t cover a critical medication, contact the insurer to ask about appeals or exceptions. Some states have laws requiring coverage for specific conditions, like diabetes or mental health, so research your state’s regulations. Finally, consider using a pharmacist as a resource—they can often suggest generic alternatives or help navigate prior authorization requirements. Prescription coverage is a non-negotiable aspect of health insurance, and thorough verification ensures you’re not left paying more than you should.

Short-Term Health Insurance: Can It Help You Avoid ACA Penalties?

You may want to see also

Frequently asked questions

Assess your healthcare needs, budget, and preferred providers. HMOs are cost-effective but require in-network care, while PPOs offer more flexibility at a higher cost. High-deductible plans with HSAs are ideal for those with low medical expenses.

Look beyond the monthly premium. Consider deductibles, copays, coinsurance, out-of-pocket maximums, and whether your preferred doctors and medications are covered.

Extremely important. Ensure your preferred doctors, hospitals, and specialists are in-network to avoid higher out-of-network costs or denied coverage.

It depends on your health needs and budget. Lower premiums often mean higher deductibles, suitable for those rarely needing care. Lower deductibles are better if you anticipate frequent medical visits.

These plans differ in premium and out-of-pocket costs. Bronze has the lowest premiums but highest out-of-pocket costs, while Platinum has the highest premiums but lowest out-of-pocket costs. Choose based on your expected healthcare usage and financial situation.