The Affordable Care Act (ACA) has been the subject of much debate since its implementation in 2014, with many claiming that it has caused insurance premiums to increase substantially. While there is evidence to suggest that premiums have indeed increased, the rate of growth has been relatively low compared to pre-ACA years, and the ACA has made healthcare available to a larger number of people. This article will explore the ways in which the ACA has slowed insurance rate increases and examine the impact of the Act on the insurance market.

| Characteristics | Values |

|---|---|

| Median proposed premium increase for 2025 | 7% |

| Range of premium changes across 324 ACA Marketplace insurers nationally | -14% to 51% |

| Number of insurers proposing decreasing premiums | 50 |

| Number of insurers requesting premium increases greater than 10% | 85 |

| Median proposed rate increase in 2024 | 6% |

| Average increase in benchmark silver premiums in 2024 | 5% |

| Total average family plan cost increase from 2008 to 2016 | 43% |

| Total average family plan cost increase from 2000 to 2008 | 97% |

| Estimated increase in employer premiums in 2011 due to ACA | 1% to 3% |

| Uninsured rate in 2023 | <8% |

| Uninsured rate in 2013 | 14.4% |

| Uninsured rate in 2016 | 9% |

| Average individual market medical costs increase between 2013 and 2015 | 69% |

Explore related products

$36.33 $54.99

What You'll Learn

![]()

ACA improves health insurance coverage rates

The Affordable Care Act (ACA) has been instrumental in improving health insurance coverage rates, as evidenced by a significant drop in the national uninsured rate. This decrease is especially notable when compared to the period before the ACA's implementation, where rising healthcare costs made coverage increasingly unaffordable.

One of the key provisions of the ACA that has enhanced coverage rates is the expansion of Medicaid eligibility. This expansion has been particularly beneficial for low-income adults without children, a group that previously faced stringent Medicaid eligibility rules and limited coverage options. As a result, millions of people who were previously uninsured have gained access to affordable and comprehensive healthcare coverage.

The ACA has also introduced tax credits for private coverage purchased through newly established marketplaces. These tax credits play a crucial role in narrowing inequities and improving coverage rates. By providing upfront financial assistance, individuals and families can more easily afford the health insurance plans offered through the ACA marketplaces. This has resulted in a substantial increase in marketplace enrollment, with millions more people enrolled in ACA plans each year.

Furthermore, the ACA has helped reduce coverage inequities among different demographic groups. This includes narrowing disparities in coverage rates between racial and ethnic groups, individuals living in rural and urban areas, and those with varying sexual orientations and gender identities.

While there have been some fluctuations in premium costs and insurer participation, the overall impact of the ACA has been positive in terms of improving health insurance coverage rates. The ACA's provisions have ensured that a larger portion of the population has access to affordable and comprehensive healthcare, which is essential for promoting better health outcomes and financial security.

Auto Insurance: Lost Keys Covered?

You may want to see also

Explore related products

![]()

ACA reduces coverage inequities

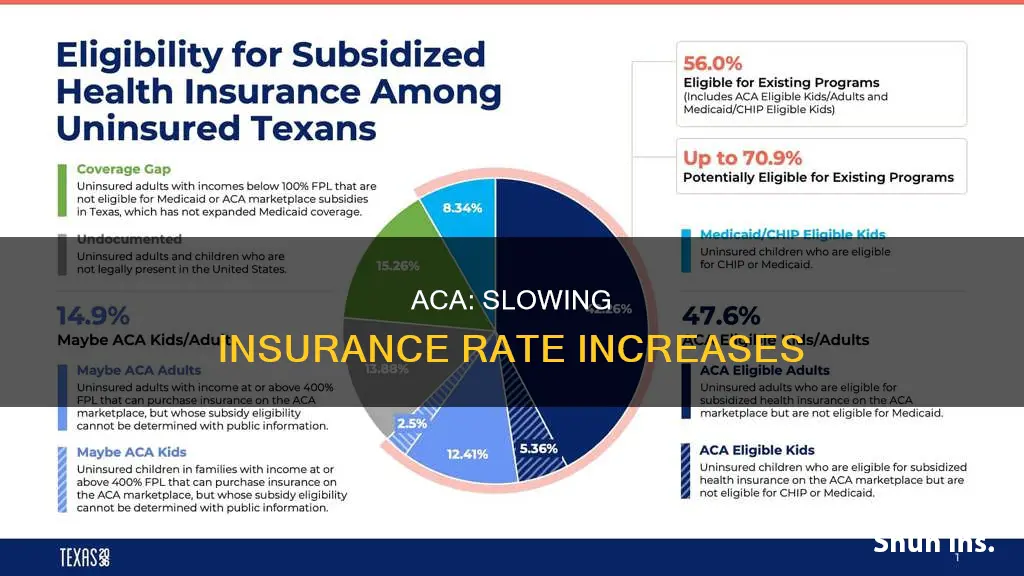

The Affordable Care Act (ACA) has been instrumental in reducing coverage inequities and improving health insurance coverage rates. According to a report by the Department of Health and Human Services' Assistant Secretary for Planning and Evaluation (ASPE), the ACA has dramatically boosted both coverage and affordability. This is particularly evident in the significant drop in the uninsured rate, which fell to below 8% in 2023, less than half the rate before the ACA.

One of the key ways the ACA achieves this is through the expansion of Medicaid eligibility. Previously, stringent Medicaid eligibility rules left non-disabled, low-income adults without children with limited coverage options. However, with the ACA, Medicaid eligibility was expanded, providing coverage for people with incomes below 138% of the federal poverty level. This expansion has resulted in millions of people transitioning from Medicaid to ACA Marketplace coverage, improving their access to affordable and comprehensive healthcare.

The ACA also addresses coverage inequities related to race, ethnicity, geographical location, sexual orientation, and gender identity. For instance, in states that expanded Medicaid, larger gains in coverage were observed, with improvements particularly evident for people with incomes under 200% of the federal poverty level.

Additionally, the ACA provides tax credits for private coverage purchased through its marketplaces. These tax credits play a crucial role in narrowing inequities and enhancing coverage rates by offering upfront financial assistance to individuals seeking health insurance plans in their state. This assistance is especially beneficial for families with incomes between 100% and 200% of the federal poverty level, who receive the largest tax credits.

While the ACA has been effective in slowing insurance rate increases and improving coverage, it's important to note that not all insurers will increase their rates at the same pace. Some individuals may be impacted by specific factors, trends, and developments in their state or regional markets. As a result, it is recommended to review your current plan and compare options to make an informed decision.

Mazda6 Insurance Costs: What You Need to Know

You may want to see also

Explore related products

![]()

ACA provides tax credits for private coverage

The Affordable Care Act (ACA) provides tax credits for private coverage, also known as premium tax credits (PTC). These tax credits are refundable, helping eligible individuals and families cover the premiums for their health insurance purchased through the Health Insurance Marketplace.

To be eligible for the premium tax credit, certain requirements must be met, and a tax return must be filed with Form 8962, Premium Tax Credit (PTC). For tax years 2021 and 2022, the American Rescue Plan Act of 2021 (ARPA) temporarily removed the rule that taxpayers with a household income above 400% of the federal poverty line cannot qualify for a premium tax credit.

When applying for Marketplace coverage, the Marketplace estimates the amount of the Premium Tax Credit that can be claimed for the tax year. This estimate is based on information provided about family composition, projected household income, and other factors such as whether those being enrolled are eligible for non-Marketplace coverage. Based on this estimate, individuals can choose to have all, some, or none of the estimated credit paid in advance directly to their insurance company to lower their monthly premiums.

The premium tax credit can be used to purchase four different types of plans offered through the marketplace: bronze, silver, gold, and platinum. All plans sold in the marketplace must meet standards to ensure adequate coverage, with bronze plans providing the least comprehensive coverage and platinum plans providing the most comprehensive.

The ACA also extends tax credits to people with annual incomes equivalent to 400% of the federal poverty level, eliminating the "subsidy cliff", which rendered people with incomes just above 400% of poverty ineligible for financial assistance.

The Race for Rates: Letting Auto Insurances Compete

You may want to see also

Explore related products

![]()

ACA increases federal spending on subsidies

The Affordable Care Act (ACA), also known as Obamacare, has reshaped the healthcare landscape in the United States. The federal government subsidizes health insurance for over 150 million Americans through various programs and tax benefits. In 2023, these subsidies amounted to $1.6 trillion, with $91 billion going towards subsidies for health insurance purchased through ACA marketplaces.

The ACA provides premium tax credits to subsidize the cost of healthcare for enrollees with incomes between 100-400% of the federal poverty line (FPL). The higher the beneficiary's income, the more the tax credit amount is reduced. The ACA limited subsidies to those below 400% of the FPL, but the American Rescue Plan in 2021 temporarily lifted this cap and increased the credit amount.

The availability of these subsidies has contributed to a decline in the uninsured population. If the enhanced subsidies expire, monthly premium payments are expected to increase sharply, and the Congressional Budget Office (CBO) projects an average of 3.8 million more uninsured people annually.

While premium increases generally result in higher federal spending on subsidies, the impact of the ACA on healthcare costs is relatively small. The growth in Medicare spending, tax breaks for employer-provided insurance, and the Medicaid program contribute significantly more to federal health program spending. Obamacare programs for those under 65, including Medicaid expansion and new health insurance subsidies, account for about 8% of the federal government's cost for major health programs.

Overall, the ACA has played a significant role in expanding healthcare access, and its impact on federal spending is primarily through the provision of subsidies to make health insurance more affordable for millions of Americans.

Auto Insurance and Child Support: Who Pays for What?

You may want to see also

Explore related products

![]()

ACA slows growth of employer premiums

The Affordable Care Act (ACA) has been associated with slower growth in employer premiums, with experts attributing the low growth rates to factors other than the ACA. The slow rate of growth in employer-sponsored premiums has been touted as positive, as it helps keep the cost of healthcare more manageable.

While the ACA has had some impact on premiums for employer-sponsored plans, the growth rates have been historically low. Experts estimate that there was a 1% to 3% increase in employer premiums in 2011 due to insurance requirements under the ACA, such as preventive care without copays and coverage for young adults up to age 26. However, the overall effect of the ACA on employer plan premiums has been minimal, and the slow growth in premiums cannot be solely attributed to the healthcare law.

The total average family plan cost increased by 43% from 2008 to 2016, a much slower rate compared to the 97% increase from 2000 to 2008. This slow rate of growth is good news for premiums, as it helps control the cost of healthcare. The ACA has also been credited with improving insurance coverage rates and affordability, particularly through the expansion of Medicaid eligibility and tax credits for private coverage.

While the ACA may have contributed to some increase in premiums, the overall impact has been mixed. Some factors, such as the economy and trends in medical claims costs, have also influenced premium growth rates. Additionally, the ACA's impact on premiums may vary depending on specific state or regional market factors, trends, and developments.

In conclusion, while the ACA has had some effect on employer premiums, the growth has been slow and may be influenced by various other factors. The ACA's improvements in coverage rates and affordability, along with the slow growth in employer premiums, have been positive outcomes that contribute to more accessible and affordable healthcare.

Best Auto Insurance in Texas: What to Choose?

You may want to see also

Frequently asked questions

ACA stands for the Affordable Care Act, also known as Obamacare.

The ACA slows insurance rate increases by providing tax credits for private coverage purchased through newly established marketplaces and expanding Medicaid eligibility. The ACA also reduced coverage inequities between different groups of people.

The ACA has dramatically improved health insurance coverage rates, with the national uninsured rate falling below 8% as of 2023, a record low that is less than half the rate before the ACA. However, there is some debate about the effect of the ACA on insurance rates, with some sources claiming that it has caused premiums to increase substantially, while others argue that the impact has been minimal.