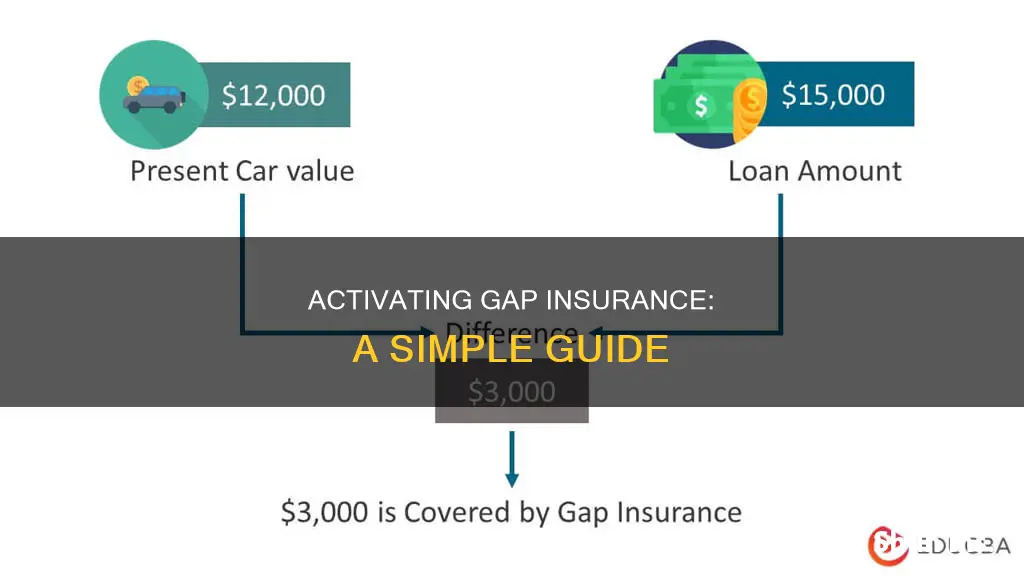

Gap insurance, or guaranteed asset protection, is an optional form of auto insurance that covers the difference between the depreciated value of a car and the loan amount owed if the car is involved in an accident, stolen, or deemed a total loss. This type of insurance is particularly useful for those who have made a small down payment (less than 20%) on a new car, are paying off the car loan over a longer period (60 months or more), or have rolled over negative equity from an old car loan. When purchasing gap insurance, it is recommended to buy it through your auto insurer rather than a dealership to avoid paying interest on the insurance.

| Characteristics | Values |

|---|---|

| What is it? | Guaranteed auto protection (GAP) insurance |

| When to get it | When you buy or lease a new car or truck |

| Who offers it | Your car dealer or auto insurance company |

| When to activate it | When your loan amount is more than your vehicle is worth |

| When to cancel it | When your vehicle is worth more than your remaining balance |

| Cost | Around $20 a year, or a flat fee of $500 to $700 |

Explore related products

What You'll Learn

![]()

When to buy gap insurance

- New Vehicle Purchase: Gap insurance is typically considered when buying a new vehicle, as it covers the "gap" between the vehicle's value and the loan or lease amount if the car is stolen or totaled. This gap is most significant in the early years of a loan when the vehicle's value depreciates faster than the loan balance decreases.

- Low Down Payment: If you make a small down payment on your vehicle purchase, you may want to consider gap insurance. A low down payment results in a larger gap between the vehicle's value and the loan amount, increasing your potential financial risk.

- Long-Term Loan: If you have a long-term loan, such as a loan term of 60 months or longer, gap insurance may be worth considering. The longer the loan term, the higher the chances of owing more than the vehicle's value.

- Quick Depreciation: Some vehicles depreciate faster than others. If you purchase a vehicle that depreciates quickly, such as certain luxury cars or electric vehicles, gap insurance can be beneficial.

- Negative Equity: If you have rolled over negative equity from a previous car loan into your new loan, gap insurance can help protect you. This situation often creates a larger gap between the vehicle's value and the loan amount.

- Lender or Lessor Requirements: In some cases, lenders or lessors may require you to have gap insurance as a condition of the loan or lease. It is important to check their requirements before making a decision.

- Financial Situation: Assess your financial ability to cover the gap between the vehicle's value and the loan amount if it is stolen or totaled. If you cannot afford to pay the difference, gap insurance can provide valuable protection.

- Cost-Benefit Analysis: Compare the cost of gap insurance with the potential financial risk you are facing. If the cost of gap insurance is significantly lower than the potential gap, it may be a worthwhile investment.

Remember that gap insurance is not required by state law, but it can provide valuable protection in certain situations. Evaluate your specific circumstances, including the vehicle's value, the loan or lease amount, and your financial ability to cover any potential gap, to make an informed decision about when to buy gap insurance.

Newer Cars: Cheaper Insurance?

You may want to see also

Explore related products

![]()

Where to buy gap insurance

When you buy or lease a new car, the dealer will likely offer you gap insurance. However, it is recommended that you also check with your insurance agent to see if their company has a better deal. Buying gap insurance from a dealer can be more expensive if the cost of the coverage is bundled into your loan amount, which means you would be paying interest on your gap coverage.

You can typically add gap coverage to an existing car insurance policy or a new policy, as long as your loan or lease has not been paid off. Buying gap insurance from an insurance company may be less expensive, and you won't pay interest on your coverage. If you already have car insurance, check with your current insurer to determine how much it would cost to add gap coverage to your existing policy. Note that you need comprehensive and collision coverage to be able to add gap coverage to a car insurance policy.

In the US, some insurance companies that offer gap insurance include:

- Progressive

- State Farm

- Allstate

- Travelers

- Nationwide

- American Modern Home Insurance Co.

- American National Property and Casualty Co.

- American Security Insurance Co.

- Balboa Insurance Co.

- Continental Casualty Co.

- Courtesy Insurance Co.

- Financial American Property and Casualty Insurance Co.

- First Colonial Insurance Co.

- Great American Insurance Co.

- Great American Insurance Company of New York

- Ironshore Indemnity Inc.

- Landcar Casualty Co.

- Lyndon Property Insurance Co.

- Markel Insurance Co.

- MIC Property and Casualty Insurance Corp.

- Old Republic Insurance Co.

- Old United Casualty Co.

- Securian Casualty Co.

- Sentruity Casualty Co.

- Service Lloyds Insurance Co.

- Spinnaker Insurance Co.

- State National Insurance Co.

- Transamerica Casualty Insurance Co.

- United Financial Casualty Co.

- Universal Underwriters Insurance Co.

- Work First Casualty Co.

Credit unions are also a good place to look for gap insurance. They often offer affordable gap insurance to their members and can shop around for you to find the best rate.

Dealerships: Test Drive Insurance

You may want to see also

Explore related products

![]()

How much does gap insurance cost?

The cost of gap insurance varies depending on where you purchase it. If you buy gap insurance from a dealership, it can cost hundreds of dollars a year. Dealerships and lenders charge higher prices for gap insurance than car insurance companies, with rates between $500 and $700. Plus, you will pay interest on the sum since it will be rolled into your loan.

If you add gap coverage to a car insurance policy that already includes collision and comprehensive insurance, it typically increases your premium by around $20 to $60 per year. Insurance companies, on the other hand, charge an average of $20 to $40 per year for gap insurance when buyers bundle it into an existing insurance policy.

If you want to buy a standalone gap insurance policy, you can expect to pay between $200 and $300.

Military Vehicles: Insured?

You may want to see also

Explore related products

![]()

When to cancel gap insurance

Gap insurance is not a legal requirement and can be cancelled at any time. However, there are certain instances when it makes sense to cancel your policy.

Firstly, if your loan balance is less than your vehicle's actual cash value, you may want to consider cancelling your gap insurance. This is because gap insurance is only valuable when you owe more than what the car is worth. So, if your car's value is greater than the remaining loan balance, you’re essentially paying for coverage that you will never use, even if your car is stolen or written off in an accident.

Secondly, if you have paid off your loan early, or sold or traded in your vehicle, you may want to cancel your gap insurance. This is because gap insurance is designed to cover the difference between the remaining loan balance and the car's value in the event of a total loss. If there is no loan to pay off, there is no need for gap insurance.

Thirdly, if you are looking to switch to a different gap insurance company, you may want to cancel your current policy. However, it is important to ensure that you have a new policy in place before cancelling your existing policy to avoid any lapse in coverage.

Finally, if you no longer feel that gap insurance is necessary for your vehicle, or if you need to lower your insurance premiums to save money, you may want to consider cancelling your policy.

It is important to note that if you cancel your gap insurance policy before the end of the term, you may be charged a cancellation fee. This fee can vary depending on the insurer and how long you have had the policy. Additionally, if you have already made a claim on your gap insurance policy, you may not be eligible for a refund.

Gap Insurance Claims: Report to NC Commissioner?

You may want to see also

Explore related products

![]()

Gap insurance alternatives

Gap insurance is not essential, and there are several alternatives to consider. Firstly, standard auto insurance policies cover the depreciated value of a car, so your insurer should pay out enough for a replacement car of a similar age and condition. If you are happy with this, you may not need gap insurance.

Secondly, many fully comprehensive car insurance policies offer 'new car replacement' for the first 12 or even 24 months for new cars. If your policy includes this, you won't need gap insurance during this period.

Thirdly, gap insurance is mostly associated with new cars, as they depreciate faster than used cars. If you have a used car, gap insurance may not be as useful, as the gap between what you paid and what the insurer will pay will be smaller.

Finally, if you are leasing a car, your leasing company may require you to purchase gap insurance. However, you can shop around for the best deal, as you don't have to buy from a car dealer. There are a number of specialist firms that can provide cover, and it may be cheaper to buy from an online provider.

Tracking Devices: Are They in Your Car?

You may want to see also

Frequently asked questions

You can get gap insurance from your car dealer or your auto insurance company.

You can get gap insurance when you buy or lease a new car. You can typically buy it at any time as long as the loan or lease isn't paid off.

Auto insurers typically charge a few dollars a month or around $20 a year. Lenders charge a flat fee of around $500 to $700.