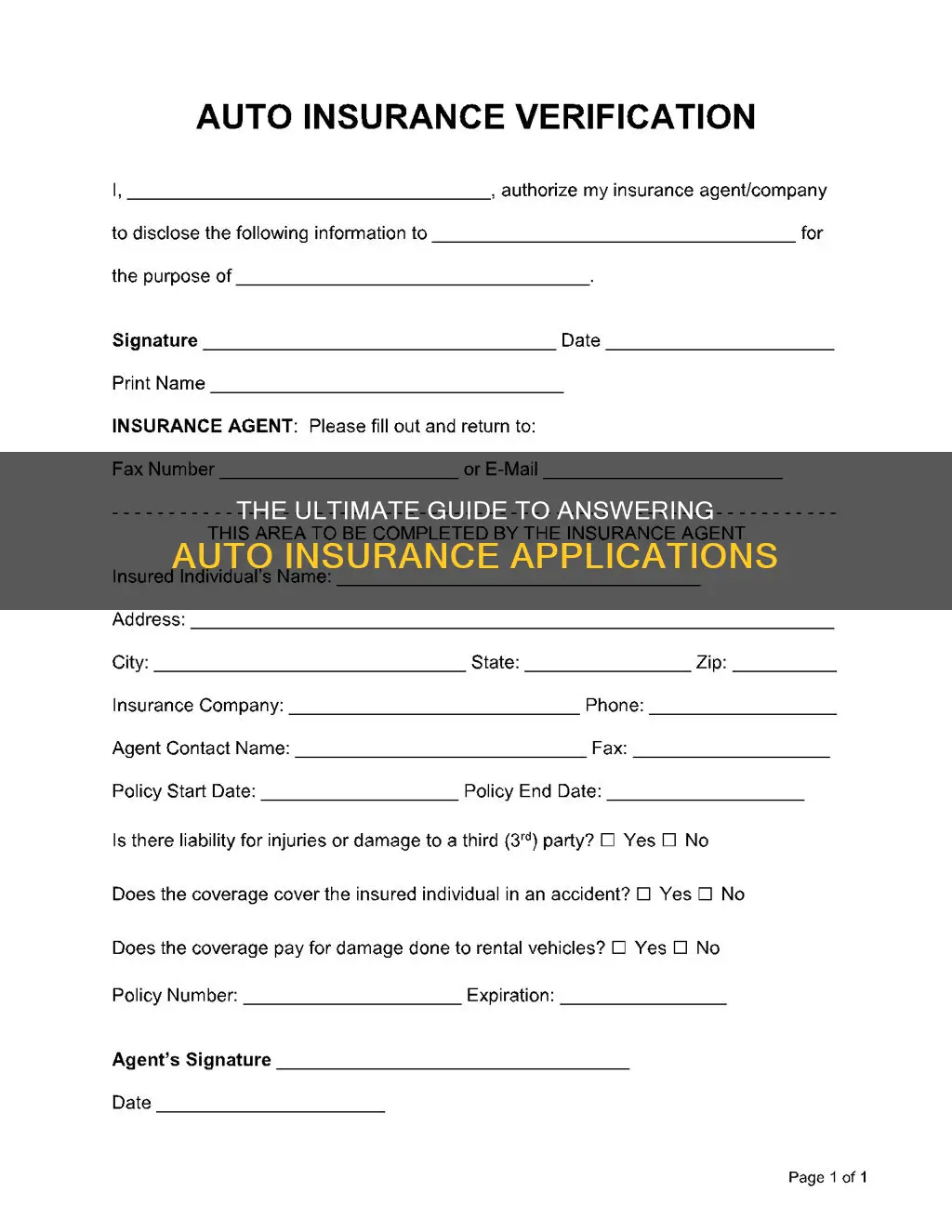

Filling out an auto insurance application is a crucial step in obtaining coverage. The application process can be done by the individual seeking insurance, or by an insurance broker, agent, or insurance company on their behalf. It is important to be prepared with the right information to ensure you get an accurate quote and are offered the right policy. The questions asked on an auto insurance application are designed to determine the type of policy to be issued and whether or not the insurance company will issue it. The application will ask for basic information about the driver(s) and the vehicle(s), including insurance history. It is important to answer all questions honestly, as providing inaccurate information can result in increased rates or even a voided policy.

| Characteristics | Values |

|---|---|

| Address | Home address, including unit number if applicable |

| Contact details | Phone number, email address |

| Personal details | Gender, date of birth, marital status, occupation, highest level of education, homeownership status |

| Vehicle details | Make, model, year, lease/finance/ownership status, purchase date, odometer reading, VIN, anti-theft devices, snow tires |

| Driving record | License type and number, dates of obtaining each level of license, license jurisdiction, insurance history, driving convictions/infringements, accidents, claims, license suspensions, driver training course completion |

| Driving habits | Primary use of vehicle, annual mileage, business use, ride-sharing, food delivery, vehicle rental, parking location and type |

| Coverage and discounts | Type of coverage, deductible amount, monitoring devices, payment frequency, bundling options |

Explore related products

What You'll Learn

![]()

Vehicle information

When applying for auto insurance, you will be asked to provide detailed information about your vehicle. This is because the insurance company needs to assess the risk factors associated with that particular vehicle. Here is a comprehensive guide on what information you will need to provide about your vehicle when applying for auto insurance:

Vehicle Make, Model, and Year

You will need to know the make, model, and year of your vehicle. This information is essential for the insurance company to determine the vehicle's value and repair costs in the event of an accident. Older vehicles may also be considered higher risk, so the year of your car is crucial.

Vehicle Identification Number (VIN)

The Vehicle Identification Number (VIN) is a unique code assigned to your vehicle. It serves as an identification mark and helps track the vehicle. While you don't need the VIN to get a quote, it is required to purchase the policy.

Safety Features and Anti-Theft Devices

Information about safety features such as passive restraint systems and anti-lock brakes is important for assessing risk and may also qualify you for discounts. Similarly, anti-theft devices like GPS trackers can lower the risk of theft and may result in a discount on comprehensive coverage.

Main Use and Expected Mileage

Insurance companies will want to know the primary use of your vehicle, such as commuting to work or school. The more you drive, the higher the risk of an accident, so the expected annual mileage is crucial. Be prepared to provide a fair estimate of how many miles you drive each year.

Insurance and Claims History

You will need to disclose your current insurance status, including years of continuous coverage and any previous insurance cancellations. Additionally, provide details about any accidents, tickets, or claims involving your vehicle. This information helps the insurance company assess your risk as a driver.

Additional Discount Information

You may also be asked for further information to determine if you qualify for any discounts. For example, some companies offer retiree discounts, multi-vehicle discounts, or multi-policy discounts.

Coverage Type and Deductibles

Finally, you will need to choose your coverage type and deductibles, which will impact your insurance premium. It is essential to understand the different types of coverage, such as liability, comprehensive, and collision insurance, to make an informed decision.

Remember, honesty is crucial when providing information for your auto insurance application. Inaccurate or misleading information can result in increased rates or even a voided policy.

Quicksilver Credit Card Auto Rental Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Driver information

When filling out an auto insurance application, the driver information you'll need to provide includes:

- The number of drivers in your household, along with their basic information, such as their full name, date of birth, age, and marital status.

- The type of driver's license each driver holds, including any international licenses.

- Details of safe driving courses completed by each driver.

- Information on student drivers, including their grades, as good grades may qualify them for a discount.

- A record of any driving convictions or violations, accidents, claims, or moving violations on each driver's record.

- The primary address where the vehicle is kept, as well as parking accommodations.

- The number of miles driven annually and the primary use of the vehicle.

- Information on any anti-theft devices installed in the vehicle.

- Details of the driver's current insurance status, including years of continuous coverage and any previous insurance cancellations.

Auto Insurance: Immigrants and Legalities

You may want to see also

Explore related products

![]()

Driving record

When applying for auto insurance, you will be asked about your driving record. This is because your driving record is one of the key factors that affect how much you pay for car insurance. A good driving record generally results in lower premiums, while a history of accidents or serious traffic violations will make your insurance more expensive as you will be deemed a high-risk driver.

Your driving record includes a history of minor and major traffic violations, including speeding tickets, accidents and/or arrests for more serious violations such as driving under the influence. It may also include your name and address, driver's license number, license status, and any convictions related to motor vehicle violations.

Insurance companies will typically look back at the previous three to five years of your driving record, but this can vary depending on the company and state regulations. Some companies may look back as few as three years, while others will go back as far as seven to ten years. DUI charges also tend to stay on your record the longest, sometimes for up to ten years.

You can check your driving record by requesting a copy through your state's Department of Motor Vehicles (DMV), usually for a small fee. Some states allow residents to check their driving record for free. It's a good idea to check your driving record periodically to make sure everything is accurate and to see when a violation occurred.

Allstate Auto Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![Texas Property and Casualty Insurance License Exam Prep - Full-Length Practice Tests, Secrets Study Guide and Review: [Detailed Answer Explanations]](https://m.media-amazon.com/images/I/610og6OB+0L._AC_UY218_.jpg)

![]()

Insurance history

When applying for auto insurance, you will need to provide information about your insurance history. This is because insurance companies use your claims history to determine your rates. They can't follow drivers around to see if they're driving responsibly, so they base risk and rates on the driver's past driving and claims history.

You can provide proof of your claims history by asking your insurer for a letter of experience. This is a document that contains all information about your policy, including the claims you've made, how the company investigated them, and how they were settled. A letter of experience must be printed on the company's letterhead and signed by an authorized representative to be considered valid.

Alternatively, if you don't want to contact your insurance company, you can get your claims history by ordering a C.L.U.E. (Comprehensive Loss Underwriting Exchange) report directly from consumer reporting agency LexisNexis. This is a free service and you're entitled to one copy every 12 months. Your C.L.U.E. report will show up to seven years of claims history for auto and home insurance policies.

If you can't remember which insurance company you've used in the past, you can try contacting your state's Department of Motor Vehicles, as they may have information on your previous insurance policies.

It's important to be honest when providing information about your insurance history. If you fail to disclose something significant, the insurance company may decide to decline to offer you a policy or change your rate once the information is exposed.

Understanding Your Auto Insurance Deductible and Costs

You may want to see also

Explore related products

![]()

Discount eligibility

Multi-Policy or Bundling Discounts

If you purchase multiple types of insurance policies from the same company, such as combining car insurance with home, renters, condo, life, motorcycle, or RV insurance, you can often qualify for a bundling discount. This is typically one of the most significant discounts, ranging from 5% to 25% off your premium.

Vehicle Safety Discounts

Insurance companies may offer discounts if your car is equipped with advanced safety features. This includes anti-lock brakes, airbags, and daytime running lights. Airbag discounts can be substantial, sometimes offering up to 40% off your medical payments or personal injury protection coverage. Additionally, cars less than three years old may qualify for a new car discount, often ranging from 10% to 15% off.

Anti-Theft Device Discounts

If your vehicle has anti-theft features, you can generally expect a discount on your comprehensive coverage. This can range from 5% to 25% off. Examples of anti-theft devices include GPS-based systems, stolen vehicle recovery systems, and VIN etching, which permanently engraves the vehicle identification number on the windshield and windows.

Good Driver Discounts

Insurance companies often reward safe drivers with discounts. For instance, Geico offers up to 26% in potential savings if you have been accident-free for five years. Similarly, State Farm offers a good driver discount to new customers who have gone three years or more without moving violations or at-fault accidents.

Defensive Driver Discounts

Taking an approved defensive driving course can result in a discount on your insurance premium. This discount usually applies to qualified drivers aged 50 or older, and the discount amount typically ranges from 5% to 10%. In some states, this discount is mandated for mature drivers.

Good Student Discount

If you or your student driver achieves good grades (usually a B average or above) and meets age requirements (often between 16 and 25), you may qualify for a good student discount. The discount amount can vary, but it typically ranges from 8% to 25% off your premium.

Student Away at School Discount

If your student driver is away at school and doesn't have regular access to your car, you may be eligible for a discount. The requirements vary, but it typically applies when the student is under 25 years old, lives more than 100 miles from home, and only uses the insured car during school vacations and holidays.

Payment Method Discounts

Insurance companies may offer discounts if you pay your policy in full upfront or set up automatic payments from your checking account. Paying in full can result in a discount ranging from 6% to 14%, while automatic payments can provide a small discount, typically between 3% and 6%.

Paperless Billing Discount

While this discount is less common nowadays as paperless billing becomes the norm, some insurance companies may still offer a small discount (around 3%) for choosing paperless billing and receiving your policy documents and billing electronically.

Online Quote Discount

Some insurance companies provide a discount if you obtain an online quote and then sign up for a policy. This discount can range from 4% to 12% off your premium.

Early Signing or Renewal Discount

Shopping for insurance early and renewing your policy before it expires can sometimes lead to a discount. This discount typically ranges from 2% to 15%, depending on how many days in advance you purchase or renew your policy.

Occupational Discounts

Your occupation may also qualify you for a discount. For example, Liberty Mutual offers special policy features for educators, and Geico provides up to 15% off for military personnel. It's worth asking your insurance agent if your profession qualifies for any discounts.

Alumni Associations and Professional Organizations

Being a member of certain alumni associations, fraternities, sororities, or professional organizations can sometimes lead to a discount on your auto insurance.

Usage-Based Insurance Program Discount

Usage-based insurance (UBI) programs adjust insurance rates based on your driving habits and frequency. Enrolling in a UBI program can provide an initial discount of 5% to 10%, and your actual driving behavior may lead to additional discounts of up to 40% at policy renewal time. However, it's important to note that your rates could also increase if your driving score is low.

Auto Insurance Claims: Can You Get Paid?

You may want to see also

Frequently asked questions

Basic information about all drivers and vehicles in the household is required. This includes the address where the vehicle is kept, the year, make and model of the car, the primary use of the vehicle, and the expected usage (mileage). You will also need to provide information on your driving record, insurance history, and any additional details that may qualify you for discounts.

You will be asked for personal information, including your home address, phone number, email address, gender, date of birth, and marital status. You may also be asked if you are retired or a student, as this could make you eligible for certain discounts.

You will be asked about your class of license, the dates you obtained each level of license, your driver's license number, and when you first became licensed. You will also be asked about your driving history, including any traffic convictions, accidents, or claims. It is important to answer these questions honestly, as inaccurate information can affect the final price you pay for insurance.

You will be asked about the year, make, and model of your vehicle, as well as whether it is leased, financed, or owned outright. You may also be asked if you put snow tires on your vehicle during the winter months and whether it is parked in a private garage, driveway, or on the street.