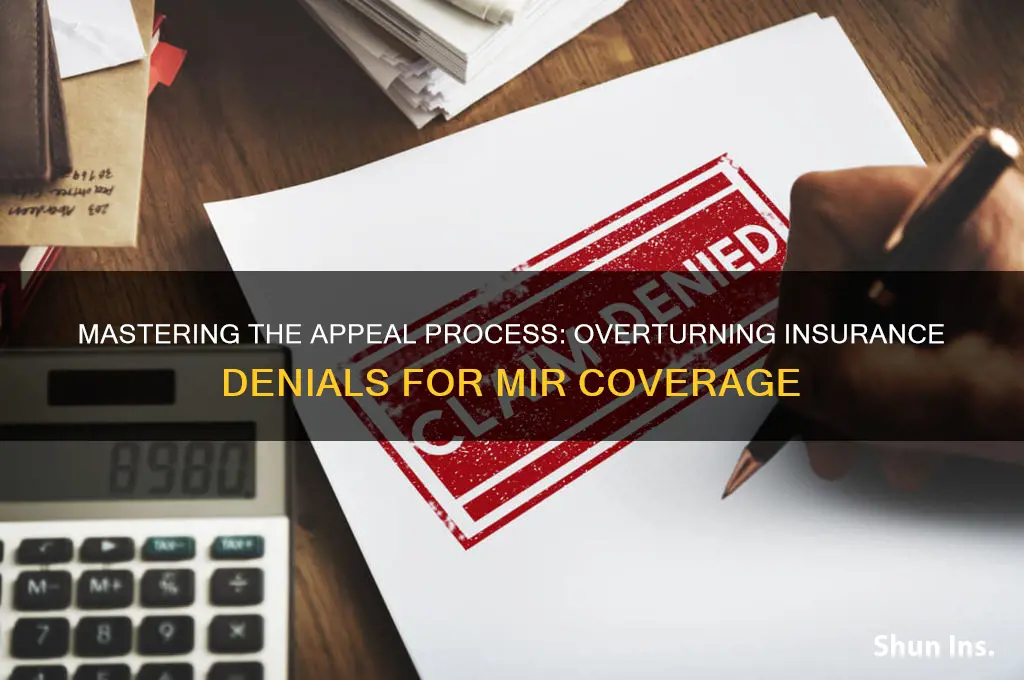

Navigating an insurance denial for a medically necessary procedure like a myomectomy in radiology (MIR) can be overwhelming, but understanding the appeals process is crucial to securing the care you need. Insurance denials often stem from discrepancies in medical coding, insufficient documentation, or policy exclusions, leaving patients feeling frustrated and uncertain. However, by carefully reviewing the denial letter, gathering comprehensive medical evidence from your healthcare provider, and submitting a well-structured appeal, you can challenge the decision effectively. This process typically involves multiple levels of review, from internal appeals with the insurer to external reviews by independent entities, ensuring a fair assessment of your case. With persistence and the right approach, appealing an insurance denial for MIR can lead to approval and access to essential treatment.

| Characteristics | Values |

|---|---|

| Understand the Denial Reason | Review the denial letter carefully to identify the specific reason for denial (e.g., lack of medical necessity, incomplete documentation, policy exclusions). |

| Gather Medical Evidence | Collect all relevant medical records, test results, physician notes, and treatment plans that support the medical necessity of the MIR (Magnetic Resonance Imaging). |

| Consult Your Healthcare Provider | Work with your doctor to obtain a detailed letter of medical necessity (LMN) explaining why the MIR is essential for diagnosis or treatment. |

| Review Insurance Policy | Carefully read your insurance policy to understand coverage details, exclusions, and appeal procedures. |

| Submit a Written Appeal | Prepare a formal written appeal including the denial letter, medical evidence, LMN, and a clear explanation of why the denial should be overturned. Follow the insurer’s specific appeal submission process. |

| Use Standard Appeal Forms | Some insurers require specific appeal forms. Ensure you use the correct form and include all requested information. |

| Include Supporting Documentation | Attach all relevant documents, such as medical records, imaging reports, and correspondence with the insurer. |

| Be Timely | Submit the appeal within the insurer’s specified deadline (typically 30-60 days from the denial date). |

| Follow Up | Track the status of your appeal and follow up with the insurer if there are delays. |

| Consider External Review | If the internal appeal is denied, request an external review by an independent third party as allowed by your state or federal law. |

| Seek Legal or Professional Help | Consult an attorney, patient advocate, or insurance broker specializing in appeals if the process becomes complex or if you need additional support. |

| Document Everything | Keep detailed records of all communications, submissions, and deadlines related to the appeal. |

| Stay Persistent | Appeals may take time and require multiple steps. Stay persistent and continue to provide necessary evidence to support your case. |

Explore related products

What You'll Learn

- Gather Medical Evidence: Collect all relevant medical records, test results, and doctor’s notes supporting the necessity of the MIR

- Review Policy Details: Carefully examine your insurance policy to understand coverage terms and exclusions related to MIR

- Write a Strong Appeal Letter: Draft a concise, clear letter explaining why the MIR is medically necessary and policy-compliant

- Include Physician Support: Obtain a detailed statement from your doctor advocating for the medical necessity of the MIR

- Follow Up Consistently: Track your appeal status, stay in contact with the insurer, and meet all deadlines promptly

![]()

Gather Medical Evidence: Collect all relevant medical records, test results, and doctor’s notes supporting the necessity of the MIR

Medical records are the backbone of any successful insurance appeal, particularly for procedures like Magnetic Resonance Imaging (MRI). Insurers often deny claims due to perceived lack of medical necessity, making comprehensive documentation your strongest ally. Begin by requesting a complete copy of your medical file from every healthcare provider involved in your diagnosis and treatment. This includes primary care physicians, specialists, and any urgent care visits related to the condition prompting the MRI. Ensure these records span the entire timeline of your symptoms, treatments, and responses to previous interventions. Incomplete records can leave gaps in your case, so be meticulous in your collection efforts.

Once gathered, scrutinize these documents for key elements that directly support the need for an MRI. Look for diagnostic notes detailing persistent or worsening symptoms despite conservative treatments, such as physical therapy or medication. For example, if you’re appealing for a knee MRI, records should show failed attempts at managing pain with anti-inflammatory drugs (e.g., ibuprofen 800 mg, three times daily for six weeks) or corticosteroid injections. Test results, like X-rays indicating soft tissue abnormalities or blood work ruling out rheumatoid arthritis, further strengthen your case. Highlight these specifics in a summary document to make it easier for the insurer to connect the dots.

Physician support is equally critical. Request a detailed letter from your treating doctor explicitly stating why the MRI is medically necessary. This letter should reference your medical history, current symptoms, and the limitations of alternative diagnostic methods. For instance, a neurologist might explain why an MRI is essential for evaluating a suspected brain lesion, as CT scans lack the necessary resolution. Include the doctor’s credentials and contact information to lend credibility to their endorsement. If possible, obtain letters from multiple specialists to demonstrate consensus on the need for the procedure.

Finally, organize your evidence systematically to maximize its impact. Create a chronological timeline of your medical journey, annotated with key events and treatments. Label each document clearly (e.g., “Dr. Smith’s Progress Notes, March 2023” or “Knee X-ray Report, January 2024”) and include a table of contents for easy navigation. If your insurer provides a specific appeal form, ensure your evidence aligns with its requirements. By presenting a well-structured, evidence-based case, you shift the burden of proof back to the insurer, increasing your chances of a favorable outcome.

Securing Your Legacy: A Guide to Insuring Revocable Trusts

You may want to see also

Explore related products

![]()

Review Policy Details: Carefully examine your insurance policy to understand coverage terms and exclusions related to MIR

Insurance policies are complex documents, often filled with jargon and fine print that can make understanding your coverage a daunting task. When faced with a denial for a Medically Necessary Procedure (MIR), the first step in your appeal process should be a meticulous review of your policy. This is not merely a cursory glance but a detailed analysis to identify the specific clauses related to MIR coverage. Start by locating the section that outlines 'Covered Procedures' or 'Medical Benefits,' where you might find a list of approved treatments, often categorized by medical specialty or condition. For instance, MIR procedures could be listed under 'Diagnostic Imaging' or 'Cardiology,' depending on the type of MIR in question.

Unraveling the Policy Language:

Insurance policies use precise language, and understanding the terminology is crucial. Look for definitions of key terms like 'Medically Necessary,' 'Experimental Treatment,' or 'Pre-existing Condition,' as these can significantly impact your coverage. For example, some policies may define 'Medically Necessary' as a procedure required to diagnose or treat an illness, injury, or symptom, but the specifics can vary. If your MIR is deemed experimental or investigational, it may be excluded from coverage, so identifying such exclusions is vital.

A Practical Approach:

Begin by gathering all relevant policy documents, including the original policy booklet, any amendments, and the denial letter from the insurance company. Create a checklist of the following:

- Coverage Period: Ensure the procedure date falls within the active policy period.

- Eligible Members: Confirm that the policy covers the individual requiring the MIR, especially in group or family plans.

- Procedure Codes: Cross-reference the MIR's medical code (e.g., CPT or HCPCS codes) with the policy's covered services list.

- Exclusions and Limitations: Identify any clauses that explicitly exclude MIR or impose restrictions, such as age limits (e.g., MIR for patients over 65) or frequency caps (e.g., one MIR per year).

Analyzing Denial Reasons:

The denial letter from your insurance provider is a critical document. It should outline the specific reasons for the rejection, often referencing particular policy sections. For instance, the letter might state, "The requested MIR is not covered under Section 4.2, which excludes diagnostic procedures for patients under 18." This provides a direct link between the denial and your policy, making it easier to formulate a targeted appeal. If the denial reason is unclear, contact your insurance provider for clarification, ensuring you document all communication.

Empowering Your Appeal:

By thoroughly reviewing your policy, you gain a powerful tool for your appeal. You can now construct a compelling argument, citing specific policy sections to support your case. For instance, if the policy covers 'Diagnostic Services' without age restrictions, but the denial was based on age, you can challenge this discrepancy. Additionally, understanding the policy's language allows you to anticipate potential counterarguments and prepare evidence to address them. This proactive approach transforms your appeal from a reactive response to a strategic, evidence-based argument, significantly improving your chances of a successful outcome.

Does Saga Offer Van Insurance? A Comprehensive Coverage Guide

You may want to see also

Explore related products

![]()

Write a Strong Appeal Letter: Draft a concise, clear letter explaining why the MIR is medically necessary and policy-compliant

A strong appeal letter is your advocate when challenging an insurance denial for a Medically Necessary MRI (MIR). It’s not a plea, but a structured argument backed by evidence. Begin by clearly stating the purpose: you’re appealing the denial of a MIR prescribed by your physician. Include the date of the denial, policy number, and specific procedure code (e.g., CPT 72148 for a lumbar spine MRI). This establishes context and demonstrates your understanding of the process.

The core of your letter hinges on demonstrating medical necessity. Detail the symptoms prompting the MIR request, using specific language from your doctor’s notes. For instance, instead of "back pain," specify "chronic, radiating pain in the left lumbar region, worsening over six weeks despite physical therapy and NSAIDs (800mg ibuprofen tid)." Cite relevant diagnostic guidelines – for example, the American College of Radiology appropriateness criteria for lumbar spine MRI in patients with suspected herniated discs.

Don’t merely assert compliance with policy; prove it. Carefully review your insurance policy’s coverage criteria for MIRs. Highlight the sections that align with your situation. For instance, if the policy covers MIRs for "persistent, unexplained pain unresponsive to conservative treatment," explicitly connect your symptoms and treatment history to this criterion. Include copies of relevant medical records, physician notes, and imaging reports as supporting evidence.

Think of your letter as a roadmap for the reviewer, making it effortless to see the direct link between your condition, the MIR’s necessity, and policy coverage.

Conclude with a clear request for approval, reiterating the urgency of the MIR for accurate diagnosis and appropriate treatment. Provide your contact information and express your willingness to supply additional information. Remember, conciseness is key. Aim for a single page, using clear, professional language. Avoid emotional appeals; let the medical facts and policy alignment speak for themselves. A well-structured, evidence-based letter significantly increases your chances of a successful appeal.

Portable Life Insurance: Rates Rising, What to Know

You may want to see also

Explore related products

![]()

Include Physician Support: Obtain a detailed statement from your doctor advocating for the medical necessity of the MIR

A denial of insurance coverage for a medically necessary procedure like a Magnetic Resonance Imaging (MRI) scan can be a frustrating and daunting experience. However, one of the most effective ways to strengthen your appeal is to include a detailed statement from your physician advocating for the medical necessity of the MRI. This statement should be comprehensive, clear, and tailored to your specific medical condition.

The Power of Physician Advocacy

Imagine your physician as your medical ambassador, armed with the knowledge and expertise to communicate the intricacies of your condition to the insurance company. A well-crafted statement from your doctor can bridge the gap between medical necessity and insurance requirements. For instance, if you're a 45-year-old patient with a history of chronic back pain, your physician can outline the progression of your condition, previous treatments attempted (e.g., physical therapy, medication management), and the rationale for requesting an MRI to rule out structural abnormalities like herniated discs or spinal stenosis. Be sure to ask your doctor to include specific details, such as the frequency and dosage of medications tried (e.g., 800 mg of ibuprofen thrice daily for 6 weeks) and the results of any previous diagnostic tests.

Crafting a Compelling Physician Statement

To maximize the impact of your physician's statement, provide them with a clear understanding of the insurance company's denial reasons. This will enable your doctor to address these concerns directly, using evidence-based medicine and clinical guidelines to support the need for an MRI. For example, if the insurance company denied coverage based on a lack of medical necessity, your physician can cite relevant studies or consensus statements from organizations like the American College of Radiology (ACR) that recommend MRI as the diagnostic modality of choice for certain conditions. Additionally, encourage your doctor to use clear, concise language and avoid medical jargon that may confuse the insurance reviewer.

Addressing Common Insurance Concerns

Insurance companies often scrutinize MRI requests for patients in certain age categories or with specific diagnoses. For instance, they may question the need for an MRI in a 25-year-old patient with acute low back pain, citing guidelines that recommend conservative management as the initial approach. In such cases, your physician can highlight aggravating factors, such as severe neurological symptoms (e.g., radiculopathy or cauda equina syndrome), that warrant expedited diagnostic workup, including MRI. By anticipating and addressing these concerns proactively, your physician can increase the likelihood of a successful appeal.

Practical Tips for Obtaining Physician Support

To facilitate the process of obtaining a detailed physician statement, schedule a dedicated appointment with your doctor to discuss the appeal. Bring a copy of the insurance denial letter, your medical records, and any relevant diagnostic reports. Be prepared to provide a concise summary of your symptoms, treatment history, and the impact of the denied MRI on your overall care plan. After the appointment, follow up with your physician's office to ensure the statement is completed and submitted to the insurance company in a timely manner, typically within 30-60 days of the denial. By working collaboratively with your physician and providing them with the necessary tools and information, you can significantly enhance the strength of your appeal and increase your chances of obtaining coverage for the medically necessary MRI.

Canceling American Life Insurance Membership: Steps to Take

You may want to see also

Explore related products

![Fiddler: Miracle of Miracles [OV]](https://m.media-amazon.com/images/I/81gxZjv4i5L._AC_UY218_.jpg)

![]()

Follow Up Consistently: Track your appeal status, stay in contact with the insurer, and meet all deadlines promptly

After an insurance denial for a medication like Mirena (MIR), the appeals process can feel like navigating a labyrinth. But consistency in follow-up is your Ariadne's thread. Think of it as a marathon, not a sprint.

Step 1: Establish a Tracking System

Don't rely on memory. Create a dedicated folder, digital or physical, for all appeal-related documents. Record every interaction with the insurer: dates, names of representatives, conversation summaries, and any reference numbers provided. Use a spreadsheet or calendar to track deadlines for submitting additional information, hearing dates, and expected response times.

Consider using a free project management tool like Trello or Asana to visually organize your appeal timeline and tasks.

Step 2: Become a Persistent (but Polite) Communicator

Silence doesn't mean progress. Proactively contact the insurer every 7-10 days to inquire about the status of your appeal. Be polite but firm. Ask specific questions: "Has my appeal been assigned to a reviewer?" "What additional information is needed?" "When can I expect a decision?" Document each call, including the representative's name and any new information. If you're met with resistance or unhelpful responses, politely escalate your inquiry to a supervisor.

Remember, persistence doesn't mean aggression. Maintain a professional tone and express your desire for a resolution.

Step 3: Deadlines are Non-Negotiable

Insurance companies are notorious for strict deadlines. Missing one can derail your entire appeal. Set reminders for all deadlines, including those for submitting medical records, attending hearings, or providing additional documentation. If you need more time, request an extension in writing, explaining your reasons clearly and concisely.

Caution: Don't Fall for Stalling Tactics

Insurance companies may try to delay the process by requesting unnecessary information or claiming they haven't received documents. If you suspect stalling, politely but firmly request written confirmation of what is needed and a clear timeline for resolution. Keep copies of all correspondence and consider sending important documents via certified mail for proof of delivery.

Consistency is key in the insurance appeal process. By diligently tracking your appeal status, maintaining regular contact with the insurer, and meeting deadlines promptly, you increase your chances of a successful outcome. Remember, you are your own best advocate. Stay organized, be persistent, and don't be afraid to ask for help if needed.

QuickBooks Insurance Entry Guide: Simplifying Post-Insurance Transactions Efficiently

You may want to see also

Frequently asked questions

The first step is to carefully review the denial letter from your insurance company to understand the specific reason for the denial. This will help you determine the appropriate grounds for your appeal.

Submit a written appeal to your insurance company, including any supporting documentation such as your doctor’s recommendation, medical records, and evidence of the procedure’s medical necessity. Follow the insurer’s specific appeal process outlined in the denial letter.

Your appeal letter should include your policy number, a clear explanation of why the procedure is medically necessary, a copy of your doctor’s recommendation, and any relevant medical records or research supporting the need for MIR.

Yes, your doctor can play a crucial role by providing a detailed letter of medical necessity, explaining why MIR is the best treatment option for your condition, and possibly contacting the insurance company directly to support your case.

If your initial appeal is denied, you can request an external review by an independent third party. Check your insurance policy or state regulations to understand your rights and the process for external review.

![Mir nach, Canaillen! - HD Remastered [Blu-ray] [1964]](https://m.media-amazon.com/images/I/81PAF-8At1L._AC_UY218_.jpg)

![SING MIR DAS LIED DER RACHE [BLU-RAY & DVD]](https://m.media-amazon.com/images/I/71XEWzkQutL._AC_UY218_.jpg)