Calculating annual hazard insurance involves assessing the potential risks to a property and determining the appropriate coverage to mitigate financial losses from events like fire, storms, or theft. The process typically begins with evaluating the property's location, construction materials, and proximity to hazards such as flood zones or wildfire-prone areas. Insurance providers then consider factors like the property's value, replacement cost, and the policyholder's claims history to estimate the annual premium. Additionally, deductibles and coverage limits play a crucial role in tailoring the policy to the homeowner's needs. Understanding these components ensures accurate and adequate protection against unforeseen damages.

| Characteristics | Values |

|---|---|

| Definition | Annual hazard insurance is calculated based on the cost to replace or repair a property in case of damage from covered perils (e.g., fire, wind, hail). |

| Key Factors | Property value, location, construction type, coverage limits, deductible, and risk factors (e.g., crime rate, weather patterns). |

| Property Value | Typically based on replacement cost, not market value. Calculated using local construction costs per square foot. |

| Location | High-risk areas (e.g., flood zones, wildfire-prone regions) increase premiums. ZIP code-specific data is used. |

| Construction Type | Frame, masonry, or fire-resistant materials impact costs. Fire-resistant homes often have lower premiums. |

| Coverage Limits | Minimum coverage is usually 80% of the property's replacement value. Higher limits increase premiums. |

| Deductible | Higher deductibles lower annual premiums but increase out-of-pocket costs at claim time. |

| Risk Factors | Proximity to fire stations, crime rates, and historical weather data influence pricing. |

| Average Annual Cost (2023) | $1,400–$2,500 (varies by state and property specifics). |

| Calculation Formula | Annual Premium = (Replacement Cost × Coverage Limit Percentage) × Risk Factor Multiplier ± Deductible Adjustment. |

| Tools for Estimation | Online calculators, insurance agent consultations, or using local construction cost data. |

| Discounts | Available for safety features (e.g., smoke detectors, storm shutters), bundled policies, or claims-free history. |

| Review Frequency | Annually or after significant property changes (e.g., renovations, additions). |

Explore related products

What You'll Learn

- Understanding Coverage Limits: Determine necessary coverage for property value, location, and potential risks

- Assessing Deductible Options: Choose deductible amount balancing premium costs and out-of-pocket expenses

- Evaluating Risk Factors: Consider location-specific risks like floods, earthquakes, or hurricanes for accurate premiums

- Comparing Policy Providers: Research and compare insurance companies for rates, reviews, and reliability

- Calculating Annual Premiums: Use property value, coverage limits, and deductibles to estimate yearly costs

![]()

Understanding Coverage Limits: Determine necessary coverage for property value, location, and potential risks

The value of your property is the cornerstone of determining adequate hazard insurance coverage. Insufficient coverage leaves you vulnerable to significant out-of-pocket expenses after a loss. For instance, if your home is valued at $300,000 and you only carry $200,000 in coverage, you’ll be responsible for the remaining $100,000 in damages. To avoid this, start by obtaining an accurate property valuation, factoring in construction costs, market trends, and any recent renovations. Many insurers offer tools or consultations to help estimate replacement costs, ensuring your coverage aligns with your property’s true value.

Location plays a critical role in assessing risk and setting coverage limits. Homes in flood zones, wildfire-prone areas, or regions with high crime rates face unique challenges. For example, a coastal property may require additional flood insurance, while a home in a wildfire zone might need higher coverage for structural damage. Analyze local risk factors by consulting FEMA flood maps, wildfire risk assessments, or crime statistics. Some insurers may mandate specific coverage types based on location, so understanding these requirements upfront can prevent gaps in protection.

Potential risks extend beyond natural disasters to include human-made hazards and unforeseen events. Consider the likelihood of burglaries, vandalism, or even liability claims if someone is injured on your property. For instance, if you own a swimming pool, your liability coverage should account for the increased risk of accidents. Similarly, if you live in an area prone to power outages, ensure your policy covers damage from electrical surges. A comprehensive risk assessment, often available through insurance providers, can help identify these potential threats and guide your coverage decisions.

Balancing coverage needs with affordability is key. While it’s tempting to opt for minimal coverage to lower premiums, this approach can backfire in the event of a major loss. Instead, focus on optimizing your policy by choosing a deductible that aligns with your financial situation. A higher deductible reduces annual premiums but requires a larger out-of-pocket payment during a claim. Conversely, a lower deductible increases premiums but minimizes immediate costs after a loss. Regularly review and adjust your coverage as your property value, location risks, or financial circumstances change to ensure ongoing protection.

Finally, leverage professional guidance to fine-tune your coverage limits. Insurance agents or brokers can provide tailored advice based on your specific situation. They can also help you explore policy endorsements or riders to address unique risks not covered by standard policies. For example, if you own high-value items like jewelry or art, consider scheduling them separately for full replacement value. By combining expert insights with a thorough understanding of your property and risks, you can craft a hazard insurance policy that offers robust protection without unnecessary costs.

Mastering QuickBooks: How to Accurately List Insurance Expenses

You may want to see also

Explore related products

![]()

Assessing Deductible Options: Choose deductible amount balancing premium costs and out-of-pocket expenses

Selecting the right deductible for your hazard insurance policy is a critical decision that directly impacts both your annual premiums and potential out-of-pocket costs in the event of a claim. A deductible is the amount you agree to pay before your insurance coverage kicks in, and it’s a lever you can adjust to manage your overall insurance expenses. For instance, opting for a higher deductible—say, $2,500 instead of $500—typically lowers your annual premium but requires you to pay more upfront if you file a claim. Conversely, a lower deductible increases your premium but reduces immediate financial strain during a loss. This trade-off demands careful consideration of your financial stability, risk tolerance, and the likelihood of needing to file a claim.

To assess deductible options effectively, start by evaluating your emergency fund and overall financial health. A general rule of thumb is to choose a deductible you can comfortably afford to pay without dipping into essential savings or going into debt. For example, if you have $5,000 set aside for emergencies, a $2,000 deductible might be manageable, whereas a $5,000 deductible could leave you vulnerable. Additionally, consider the frequency and severity of hazards in your area. If you live in a region prone to hurricanes, wildfires, or floods, a lower deductible might be wiser, as the probability of filing a claim is higher. Conversely, if your area has minimal risk, a higher deductible could save you money over time.

Another practical approach is to calculate the break-even point for different deductible options. For instance, if raising your deductible from $500 to $1,000 saves you $200 annually on premiums, it would take five years to recoup the additional $500 out-of-pocket cost if you never file a claim. Multiply this analysis across various deductible levels to identify the sweet spot where premium savings align with your risk appetite. Tools like online insurance calculators can simplify this process, allowing you to input your specific circumstances and compare scenarios side by side.

Finally, don’t overlook the psychological aspect of deductible selection. While a higher deductible may seem appealing due to lower premiums, the stress of covering a large out-of-pocket expense during a crisis can outweigh the savings. Conversely, a lower deductible provides peace of mind but may feel financially inefficient if you rarely file claims. Striking a balance requires honesty about your financial habits and emotional resilience. For example, if you’re disciplined about saving and live in a low-risk area, a higher deductible might be a smart long-term strategy. However, if unpredictability makes you uneasy, a lower deductible could be worth the extra cost.

In conclusion, choosing the right deductible is a personalized decision that hinges on your financial situation, risk exposure, and psychological comfort. By methodically evaluating your emergency funds, calculating break-even points, and considering your risk tolerance, you can select a deductible that optimizes both premium costs and out-of-pocket expenses. Remember, the goal isn’t to minimize one at the expense of the other but to find a sustainable balance that protects your home and finances effectively.

Life Insurance: Understanding Non-Convertible Policies and Their Implications

You may want to see also

Explore related products

![]()

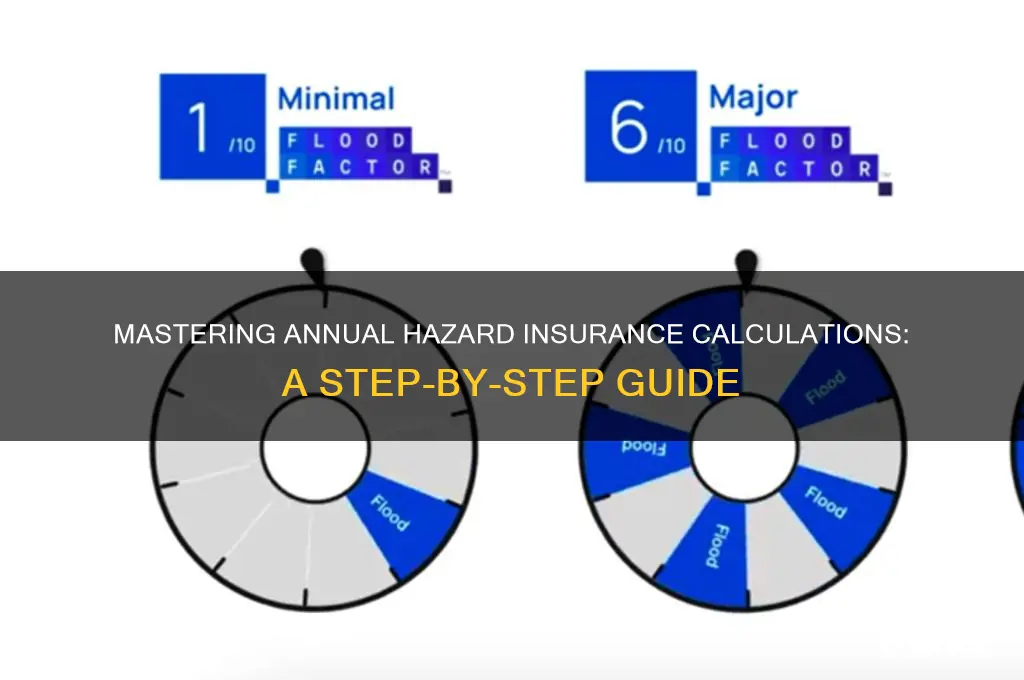

Evaluating Risk Factors: Consider location-specific risks like floods, earthquakes, or hurricanes for accurate premiums

Geographic location profoundly influences hazard insurance premiums because natural disasters are not evenly distributed. For instance, properties in Florida face a 26% chance of hurricane damage over 30 years, while California homes in high-risk seismic zones have a 1-in-6 chance of earthquake damage within the same period. Insurers use FEMA flood maps, USGS seismic data, and NOAA hurricane tracks to quantify these risks, adjusting premiums accordingly. A coastal Miami home might pay $4,000 annually for hazard insurance, whereas a similar inland property could pay half that amount. Understanding these location-specific risks is the first step in calculating accurate premiums.

To evaluate these risks, insurers employ risk-modeling tools that simulate disaster scenarios. For example, flood risk is assessed using elevation certificates and historical water levels, while earthquake risk considers proximity to fault lines and soil type. In hurricane-prone areas, wind mitigation features like impact-resistant windows can reduce premiums by up to 45%. Policyholders can access these models through their insurers or third-party platforms like Risk Factor by First Street Foundation, which provides property-specific risk scores. By cross-referencing these tools with local building codes, homeowners can identify vulnerabilities and take proactive measures to lower costs.

A comparative analysis reveals how location-specific risks drive premium disparities. In New Orleans, where flood insurance averages $700 annually, properties in Zone A (high-risk) pay double those in Zone X (low-risk). Similarly, in California, homes within 5 miles of the San Andreas Fault may see premiums 30% higher than those farther away. These variations underscore the importance of granular risk assessment. Insurers often use tiered pricing, categorizing properties into risk bands based on geographic data. For policyholders, this means that even small differences in location—such as being on the north vs. south side of a river—can significantly impact costs.

Persuasively, homeowners should not rely solely on insurers to assess their risks. Instead, they should conduct their own due diligence by reviewing local hazard maps and investing in mitigation measures. For flood-prone areas, elevating electrical systems and installing sump pumps can reduce damage by 70%. In earthquake zones, retrofitting foundations and securing heavy furniture lowers structural risk. These actions not only protect property but also demonstrate to insurers a commitment to risk reduction, often qualifying homeowners for discounts. By taking control of their risk profile, policyholders can ensure premiums reflect their actual exposure, not just their ZIP code.

Finally, a practical takeaway is to integrate location-specific risk assessments into annual insurance reviews. Premiums should be recalibrated if local risk factors change—for example, if a new flood map reclassifies a property or if a hurricane season exceeds historical averages. Homeowners can request updated quotes or shop around for insurers specializing in their region’s risks. For instance, companies like Kin Insurance focus on hurricane-prone states, offering tailored policies with lower premiums for homes with reinforced roofs. By staying informed and proactive, homeowners can avoid overpaying while ensuring adequate coverage for their unique risks.

Insurance Coverage in Penang: AM Assurance

You may want to see also

Explore related products

![]()

Comparing Policy Providers: Research and compare insurance companies for rates, reviews, and reliability

Calculating annual hazard insurance isn’t just about crunching numbers—it’s about finding the right provider. Start by researching insurance companies systematically. Begin with rates, as they’re the most tangible factor. Use online comparison tools like The Zebra or Policygenius to input your property details and receive quotes from multiple providers. Pay attention to deductibles, coverage limits, and discounts for bundling policies or installing safety features like smoke detectors or storm shutters. For instance, a homeowner in a flood-prone area might find that Company A offers a lower base rate but excludes flood coverage, while Company B charges more but includes it. This step isn’t just about finding the cheapest option—it’s about understanding what you’re paying for.

Next, dive into reviews to gauge customer satisfaction and reliability. Platforms like J.D. Power, the National Association of Insurance Commissioners (NAIC), and Google Reviews provide insights into claims processing, customer service, and overall experience. Look for patterns: does a company consistently delay payouts, or do they excel in handling emergencies? For example, a provider with a high NAIC complaint ratio might signal red flags, even if their rates are competitive. Conversely, a company with glowing reviews for their responsive claims team could justify a slightly higher premium. Remember, insurance is a long-term relationship—you want a partner, not just a policy.

Reliability is the backbone of any insurance provider, so investigate their financial stability. Check ratings from agencies like A.M. Best, Moody’s, or Standard & Poor’s to ensure the company can pay out claims, especially after widespread disasters. A provider with an A+ rating is more likely to stand firm when you need them most. For instance, during Hurricane Harvey, some smaller insurers struggled to meet claims, while larger, more stable companies handled payouts efficiently. This step is non-negotiable—a low rate means nothing if the company can’t deliver when disaster strikes.

Finally, balance these factors to make an informed decision. Create a spreadsheet to compare rates, reviews, and reliability side by side. For example, Company X might offer the lowest rate but has mediocre reviews and a B financial rating, while Company Y charges 10% more but boasts excellent reviews and an A+ rating. Practical tip: prioritize reliability and reviews over rates, especially if you live in a high-risk area. A slightly higher annual premium is a small price for peace of mind. By taking this structured approach, you’ll not only calculate your hazard insurance accurately but also secure a policy that truly protects your investment.

Life Insurance and Probate: What's the Connection?

You may want to see also

Explore related products

![]()

Calculating Annual Premiums: Use property value, coverage limits, and deductibles to estimate yearly costs

The annual cost of hazard insurance isn’t arbitrary—it’s a calculated figure tied to the specifics of your property and policy choices. At its core, insurers use three key variables: property value, coverage limits, and deductibles. Understanding how these factors interact allows you to estimate your yearly premium with reasonable accuracy. For instance, a $300,000 home with $250,000 in coverage and a $1,000 deductible will yield a different premium than a $500,000 home with $400,000 in coverage and a $2,500 deductible. This isn’t guesswork; it’s a formula rooted in risk assessment.

Let’s break it down step-by-step. First, property value serves as the baseline. Insurers typically charge $350 to $2,000 annually per $100,000 of home value, depending on location and risk factors. For example, a $400,000 home might start at $1,400 annually in a low-risk area but climb to $4,000 in a hurricane-prone zone. Next, coverage limits—the maximum amount your policy will pay—directly influence costs. Opting for 80% of your home’s value (a common benchmark) will be cheaper than full replacement cost coverage. Finally, deductibles act as a cost-sharing mechanism. A $2,500 deductible can reduce premiums by 5–10% compared to a $500 deductible, but ensure it’s an amount you can afford in an emergency.

Consider this comparative analysis: In Texas, where hail damage is common, a homeowner with a $350,000 property might pay $1,800 annually with a $1,000 deductible and $250,000 in coverage. In contrast, a similar home in Ohio, with lower disaster risk, could cost $1,200 annually. The difference? Location-specific hazards and how insurers weigh property value against regional risks. This highlights why a one-size-fits-all approach doesn’t work—premiums are hyper-personalized.

A persuasive argument for proactive planning: Don’t wait until renewal to scrutinize these factors. Adjusting coverage limits or raising deductibles can yield immediate savings. For example, if your home’s value has dropped since your last appraisal, reducing coverage limits could lower premiums by 10–15%. Conversely, underinsuring to save money is risky; a $200,000 policy on a $300,000 home could leave you $100,000 short in a total loss. Balance cost with protection by annually reviewing these variables with your insurer or using online calculators for quick estimates.

In conclusion, calculating annual hazard insurance premiums isn’t a black box. By focusing on property value, coverage limits, and deductibles, you can demystify the process and take control of your costs. Treat these variables as levers—adjust them strategically to align with your budget and risk tolerance. Whether you’re a first-time homeowner or a seasoned policyholder, this approach ensures you’re not overpaying or underprotected.

Does Vanliner Insure Suddath? Exploring Coverage and Partnership Details

You may want to see also

Frequently asked questions

Annual hazard insurance is a type of property insurance that protects against specific risks like fire, theft, or natural disasters. It’s important because it provides financial coverage for damages or losses to your property, ensuring you’re not left with significant out-of-pocket expenses.

To calculate the annual hazard insurance premium, insurers consider factors like property value, location, construction type, and risk of hazards. Multiply the property’s insured value by the insurance rate per $1,000 of coverage, then add any additional fees or discounts.

Yes, location significantly impacts the cost. Properties in areas prone to natural disasters (e.g., floods, hurricanes, or wildfires) or high crime rates typically have higher premiums due to increased risk.

Yes, you can reduce premiums by increasing your deductible, bundling policies, improving home safety features (e.g., smoke detectors, security systems), or maintaining a claims-free history. Regularly reviewing and comparing policies can also help find better rates.