Choosing the best health insurance plan under the Affordable Care Act (Obamacare) requires careful consideration of your individual needs, budget, and available options. Start by assessing your healthcare requirements, including anticipated medical expenses, prescription needs, and preferred doctors or hospitals. Compare plans based on premiums, deductibles, copayments, and out-of-pocket maximums, ensuring the plan aligns with your financial situation. Evaluate the provider network to confirm your preferred healthcare professionals are included, and check the coverage for essential health benefits like preventive care, maternity care, and mental health services. Utilize the Health Insurance Marketplace to explore subsidies or tax credits that can lower costs, and consider factors like plan metal tiers (Bronze, Silver, Gold, Platinum) to balance coverage and affordability. Finally, read reviews and seek guidance from insurance experts or navigators to make an informed decision that best suits your health and financial goals.

Explore related products

What You'll Learn

- Understand ACA Plans: Learn about Bronze, Silver, Gold, and Platinum plans and their coverage levels

- Check Network Providers: Ensure your preferred doctors and hospitals are in the plan’s network

- Estimate Costs: Compare premiums, deductibles, copays, and out-of-pocket maximums for affordability

- Review Subsidy Eligibility: Check if you qualify for premium tax credits or cost-sharing reductions

- Assess Coverage Needs: Evaluate essential health benefits and additional services like dental or vision

![]()

Understand ACA Plans: Learn about Bronze, Silver, Gold, and Platinum plans and their coverage levels

The Affordable Care Act (ACA) categorizes health insurance plans into four metal tiers: Bronze, Silver, Gold, and Platinum. Each tier reflects a different balance between monthly premiums and out-of-pocket costs, designed to meet varying financial and health needs. Understanding these differences is crucial for selecting a plan that aligns with your budget and healthcare usage.

Analytical Breakdown:

Bronze plans, with the lowest monthly premiums, cover approximately 60% of healthcare costs, leaving you responsible for 40%. They’re ideal for healthy individuals who rarely visit the doctor but want protection against catastrophic events. Silver plans, covering about 70% of costs, are a middle-ground option often paired with cost-sharing reductions (CSRs) for lower-income enrollees, reducing deductibles and copays. Gold plans, covering 80% of costs, offer lower out-of-pocket expenses but come with higher premiums, suitable for those with frequent medical needs. Platinum plans, covering 90% of costs, have the highest premiums but the lowest out-of-pocket costs, best for individuals anticipating extensive healthcare use.

Practical Tips:

To choose the right tier, evaluate your annual healthcare spending. If you rarely see a doctor, a Bronze plan may suffice, but ensure you can afford the high deductible. For moderate healthcare use, Silver plans often provide the best value, especially if you qualify for CSRs. Gold and Platinum plans are prudent for chronic conditions or anticipated surgeries, as they minimize out-of-pocket expenses despite higher premiums. Use the ACA’s subsidy calculator to estimate your net premium costs, as tax credits can significantly reduce expenses for Silver and higher-tier plans.

Comparative Insight:

Consider a 35-year-old earning $40,000 annually. A Bronze plan might cost $250/month with a $6,000 deductible, while a Silver plan could be $300/month with a $4,000 deductible. If this individual anticipates $5,000 in medical expenses, the Bronze plan would cost $7,750 ($250 x 12 + $5,000), while the Silver plan would cost $7,600 ($300 x 12 + $4,000). Here, the Silver plan offers better value despite the higher premium.

Takeaway:

The ACA’s metal tiers are not one-size-fits-all. Bronze suits the healthy and budget-conscious, Silver balances cost and coverage, Gold caters to frequent healthcare users, and Platinum is for those prioritizing minimal out-of-pocket costs. Pair your health needs with financial analysis to make an informed decision. Always factor in subsidies and potential healthcare expenses to maximize your plan’s value.

Texas Insurance Premium Hikes: Who Approves Rate Increases?

You may want to see also

Explore related products

$13.63 $17.95

$86.49 $245.95

![]()

Check Network Providers: Ensure your preferred doctors and hospitals are in the plan’s network

One of the most critical yet overlooked steps in choosing an Obamacare plan is verifying that your preferred healthcare providers are in-network. Out-of-network care can result in significantly higher out-of-pocket costs, even for essential services. For instance, a routine visit to an out-of-network specialist might cost $250 instead of the $50 copay you’d pay in-network. To avoid this, start by listing all the doctors, specialists, and hospitals you currently use or anticipate needing. Then, cross-reference this list with the plan’s provider directory, which is typically available on the insurer’s website or through Healthcare.gov. If you’re unsure how to access this information, call the insurance company directly—it’s better to spend 15 minutes verifying now than face unexpected bills later.

Consider this scenario: You’re a 35-year-old with a primary care physician you’ve seen for years and a dermatologist who manages your chronic skin condition. Before enrolling in a plan, check if both providers are in-network. If only one is covered, weigh the pros and cons. Is it worth switching plans to keep both, or can you afford to pay out-of-pocket for one? Some plans may offer out-of-network coverage but with higher deductibles or coinsurance, so factor this into your decision. For families, this step is even more crucial. If your child sees a pediatrician or your spouse has a preferred OB/GYN, ensure they’re covered to avoid disruptions in care.

A common mistake is assuming that a provider’s participation in one plan from an insurer means they’re in-network for all plans offered by that company. This isn’t always true. For example, a Bronze plan and a Gold plan from the same insurer might have different provider networks. Always check the specific plan’s directory, not just the insurer’s general network. Additionally, if you’re considering a narrow-network plan (often cheaper but with fewer providers), be extra diligent. These plans may exclude major hospitals or specialists, which could limit your care options in emergencies or for complex conditions.

Here’s a practical tip: If you’re switching plans but want to keep your current providers, contact their office directly. They may have insights into which plans they’ll accept in the coming year or can help you navigate the insurer’s directory. Another strategy is to prioritize plans with broader networks if you frequently travel or live in a rural area. A larger network increases the likelihood of finding in-network care wherever you are. Finally, don’t forget to verify pharmacy networks if you take prescription medications. Some plans have separate networks for pharmacies, and using an out-of-network pharmacy can drastically increase drug costs.

In conclusion, checking network providers isn’t just a box to tick—it’s a cornerstone of selecting a plan that aligns with your healthcare needs. By investing time upfront to ensure your preferred doctors and hospitals are in-network, you’ll avoid costly surprises and maintain continuity of care. Remember, the goal of health insurance is to provide financial protection and access to quality care, not to add layers of complexity. This step simplifies that process, ensuring your plan works for you, not against you.

Why Insurance Companies Mandate House Painting: Uncovering the Hidden Reasons

You may want to see also

Explore related products

![]()

Estimate Costs: Compare premiums, deductibles, copays, and out-of-pocket maximums for affordability

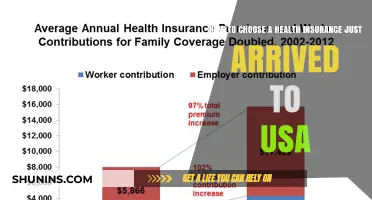

Understanding the financial implications of your health insurance plan is crucial when navigating the Obamacare marketplace. A key aspect of this is estimating costs, which involves a detailed comparison of premiums, deductibles, copays, and out-of-pocket maximums. These components collectively determine the affordability and suitability of a plan for your specific needs.

Premiums: The Monthly Commitment

The premium is your monthly payment for health insurance coverage, due regardless of whether you use medical services. When comparing plans, consider how the premium fits into your budget. For instance, a 30-year-old individual might find that a Bronze plan offers lower premiums but higher out-of-pocket costs, while a Gold plan provides more comprehensive coverage at a higher monthly cost. Balancing this expense with other financial obligations is essential. A practical tip is to calculate the annual premium cost (monthly premium × 12) to better understand the long-term financial commitment.

Deductibles and Copays: Unraveling the Cost-Sharing

Deductibles and copays are critical in understanding your potential expenses. A deductible is the amount you pay for covered services before your insurance plan starts to pay. For example, if you have a $2,000 deductible, you're responsible for the first $2,000 of covered medical expenses. Copays, on the other hand, are fixed amounts you pay for specific services, like a doctor's visit or prescription medication. When evaluating plans, consider your expected healthcare usage. If you anticipate frequent medical visits, a plan with a higher premium but lower deductibles and copays might be more cost-effective.

Out-of-Pocket Maximums: Capping Your Expenses

The out-of-pocket maximum is a critical safety net in health insurance. This is the most you'll have to pay for covered services in a plan year. Once you reach this limit, the insurance company covers all additional costs. For instance, a plan with a $5,000 out-of-pocket maximum means your expenses are capped at this amount, providing financial protection against catastrophic health events. When comparing plans, especially for families or individuals with chronic conditions, choosing a plan with a lower out-of-pocket maximum can offer significant savings and peace of mind.

Strategic Cost Comparison: A Practical Approach

To effectively estimate costs, create a comparison chart listing different plans' premiums, deductibles, copays, and out-of-pocket maximums. Consider your past healthcare usage and anticipated needs. For instance, if you require regular specialist visits, compare the copays for these services across plans. Additionally, factor in the potential for unexpected medical events. A plan with a slightly higher premium but lower out-of-pocket maximum might be more affordable in the long run if it provides better protection against unforeseen health issues. This strategic approach ensures you choose a plan that aligns with your financial capabilities and healthcare requirements.

In the complex landscape of health insurance, estimating costs is a powerful tool for making informed decisions. By meticulously comparing premiums, deductibles, copays, and out-of-pocket maximums, you can identify the most affordable and suitable Obamacare plan. This process empowers you to navigate the marketplace with confidence, ensuring your health insurance choice is both financially viable and comprehensively protective.

Nevada Carpenters Union Trust Insurance Company: Understanding Its Role and Benefits

You may want to see also

Explore related products

![]()

Review Subsidy Eligibility: Check if you qualify for premium tax credits or cost-sharing reductions

One of the most significant advantages of the Affordable Care Act (ACA), often referred to as Obamacare, is the availability of financial assistance through premium tax credits and cost-sharing reductions. These subsidies can dramatically lower your health insurance costs, but only if you qualify. Eligibility is primarily based on your household income and the size of your family. For 2023, individuals earning between 100% and 400% of the federal poverty level (FPL) generally qualify for premium tax credits. For a single person, this translates to an annual income range of approximately $13,590 to $54,360. Families of four can earn between $27,750 and $111,000 to be eligible. However, recent legislative changes have expanded eligibility, allowing some individuals with incomes above 400% of the FPL to qualify for subsidies if their premiums exceed 8.5% of their income.

To determine your subsidy eligibility, start by gathering your financial information, including your household income, the number of dependents, and any other sources of income. Use the Healthcare.gov subsidy calculator or consult a certified insurance navigator to estimate your potential savings. Keep in mind that eligibility is based on your projected income for the year, so be as accurate as possible. If you underestimate your income, you may have to repay some or all of the subsidy when you file your taxes. Conversely, overestimating could mean missing out on financial assistance you’re entitled to.

Cost-sharing reductions (CSRs) are another form of subsidy available to individuals and families with incomes between 100% and 250% of the FPL. These reductions lower out-of-pocket costs like deductibles, copayments, and coinsurance, making healthcare more affordable for those with modest incomes. For example, a silver-level plan with CSRs might have a deductible of $200 instead of $4,000 for someone at 150% of the FPL. To qualify for CSRs, you must enroll in a silver-level plan through the ACA marketplace. These reductions are applied automatically if you meet the income criteria, so there’s no separate application process.

A practical tip for maximizing your subsidy benefits is to shop for plans during the annual Open Enrollment Period or a Special Enrollment Period if you qualify. Premiums and plan options change each year, so reviewing your choices annually ensures you’re getting the best value. Additionally, if your income fluctuates during the year—due to job loss, a raise, or other changes—report these updates to the marketplace promptly. Adjusting your income information can prevent overpayment or underpayment of subsidies and ensure your coverage remains affordable.

In conclusion, reviewing your subsidy eligibility is a critical step in choosing the best health insurance under Obamacare. By understanding the income thresholds, using available tools to estimate your savings, and staying informed about changes to your financial situation, you can take full advantage of the financial assistance available. Subsidies can make the difference between affordable coverage and going uninsured, so don’t overlook this opportunity to reduce your healthcare costs.

Medical Insurance Coverage Options in San Diego

You may want to see also

Explore related products

$69.69 $105.95

![]()

Assess Coverage Needs: Evaluate essential health benefits and additional services like dental or vision

Understanding your health coverage needs is the cornerstone of selecting the right Obamacare plan. Start by identifying essential health benefits (EHBs), which are mandated under the Affordable Care Act (ACA) and include outpatient care, emergency services, hospitalization, maternity and newborn care, mental health services, and prescription drugs, among others. These benefits form the baseline of any ACA-compliant plan, ensuring comprehensive coverage for critical health needs. For instance, if you have a chronic condition requiring regular medication, scrutinize the prescription drug coverage to ensure your medications are included in the plan’s formulary.

Next, consider additional services like dental, vision, or wellness programs, which are not always included in standard plans. While EHBs cover the essentials, these add-ons can address specific health priorities. For example, if you wear glasses or contacts, a plan with vision coverage could save you hundreds of dollars annually. Similarly, dental coverage is crucial for preventive care, such as cleanings and fillings, which can prevent costly procedures later. Evaluate your lifestyle and health history to determine if these services align with your needs.

A practical approach is to categorize your health expenses into three tiers: predictable, occasional, and rare. Predictable expenses, like annual check-ups or ongoing prescriptions, should align with EHBs. Occasional needs, such as dental cleanings or eye exams, may warrant additional coverage. Rare but high-cost scenarios, like emergency surgeries, are typically covered under EHBs but require reviewing out-of-pocket maximums. For instance, a family with young children might prioritize pediatric dental coverage, while an older individual might focus on vision and preventive care.

When assessing coverage, compare plans using real-life scenarios. For example, if you’re considering a Silver plan with dental coverage versus a Gold plan without it, calculate the annual cost of dental services out-of-pocket versus the premium difference. Tools like Healthcare.gov’s plan comparison feature can help visualize these trade-offs. Additionally, consider age-specific needs: children under 10 may benefit from pediatric dental and vision coverage, while adults over 40 might prioritize preventive screenings included in EHBs.

Finally, balance cost and value by weighing premiums against potential out-of-pocket expenses. A plan with lower premiums but high deductibles might be suitable if you’re healthy and rarely visit the doctor. Conversely, if you anticipate frequent medical visits or have ongoing health needs, a higher-premium plan with lower copays and deductibles could offer better long-term savings. For instance, a 30-year-old with no chronic conditions might opt for a Bronze plan, while a 50-year-old with hypertension might choose a Gold plan for lower out-of-pocket costs on medications and specialist visits.

By systematically evaluating essential health benefits and additional services, you can tailor your Obamacare plan to meet both your immediate and long-term health needs, ensuring you’re neither overpaying nor underinsured.

Disabled Veterans' Family Health Insurance: Coverage, Benefits, and Eligibility Explained

You may want to see also

Frequently asked questions

Consider your budget, healthcare needs, preferred doctors and hospitals, prescription drug coverage, and the plan’s metal tier (Bronze, Silver, Gold, Platinum) to balance premiums and out-of-pocket costs.

Check the plan’s provider network directory or contact the insurance company directly to verify if your preferred doctors, specialists, and hospitals are in-network.

The metal tiers indicate the plan’s cost-sharing structure. Bronze has lower premiums but higher out-of-pocket costs, while Platinum has higher premiums but lower out-of-pocket costs.

Yes, if your income falls within certain limits, you may qualify for premium tax credits or cost-sharing reductions. Use the Healthcare.gov marketplace to determine eligibility.