Comparing health insurance and Medicare is essential for making informed decisions about your healthcare coverage, especially as you navigate different life stages or changing needs. Health insurance typically refers to private plans offered through employers or individual marketplaces, which vary widely in terms of premiums, deductibles, and coverage options. Medicare, on the other hand, is a federal program primarily for individuals aged 65 and older, as well as certain younger people with disabilities, and it consists of different parts (A, B, C, and D) that cover hospital stays, medical services, prescription drugs, and more. To effectively compare the two, consider factors such as eligibility, cost, coverage scope, provider networks, and additional benefits like vision or dental care. Understanding these differences will help you determine whether a private health insurance plan, Medicare, or a combination of both (such as a Medicare Advantage or Medigap plan) best meets your healthcare and financial needs.

Explore related products

What You'll Learn

- Coverage Differences: Compare Medicare vs. private insurance benefits, exclusions, and network restrictions

- Cost Analysis: Evaluate premiums, deductibles, copays, and out-of-pocket maximums for each plan

- Provider Networks: Check if preferred doctors, hospitals, and specialists are in-network

- Prescription Drug Plans: Compare Part D coverage and formularies for medication needs

- Supplemental Options: Assess Medigap policies to fill Medicare Original gaps

![]()

Coverage Differences: Compare Medicare vs. private insurance benefits, exclusions, and network restrictions

Medicare and private insurance plans often diverge in their coverage of prescription drugs, a critical factor for many, especially seniors. Medicare Part D, the prescription drug benefit, typically categorizes medications into tiers, with each tier having a different cost-sharing structure. For instance, Tier 1 (generic drugs) might have a $10 copay, while Tier 3 (brand-name drugs) could cost $45 or more per prescription. Private insurance plans, on the other hand, may offer more flexibility in drug coverage, sometimes including newer, specialty medications not covered by Medicare. However, these plans often require prior authorization or step therapy, where you must try a less expensive drug first. To navigate this, compare the formularies (list of covered drugs) of both options, focusing on the medications you currently take or anticipate needing.

Benefit exclusions are another area where Medicare and private insurance differ significantly. Medicare Part A and Part B have specific gaps, such as limited coverage for dental, vision, and hearing services. For example, Medicare does not cover routine dental check-ups or eyeglasses, which can be costly out of pocket. Private insurance plans, particularly Medicare Advantage (Part C) plans, often bundle these additional benefits, providing more comprehensive coverage. However, these plans may come with higher premiums or stricter provider networks. When evaluating, consider your current and future health needs—if you require frequent dental work or vision care, a private plan might offer better value despite the added cost.

Network restrictions can dramatically impact your healthcare experience. Original Medicare (Part A and Part B) allows you to visit any doctor or hospital that accepts Medicare, providing broad flexibility. Private insurance, including Medicare Advantage plans, often limits you to a specific network of providers. While this can reduce costs, it may also restrict access to specialists or preferred healthcare providers. For example, if you have a trusted oncologist outside the network, a private plan could force you to switch providers or pay out-of-network rates. To avoid surprises, verify whether your preferred doctors and hospitals are in-network for any private plan you’re considering.

Lastly, understanding the trade-offs between out-of-pocket costs and coverage is essential. Medicare typically has lower premiums but higher deductibles and coinsurance, especially for hospital stays (Part A) or outpatient services (Part B). For example, Medicare Part A has a $1,600 deductible per benefit period for hospital stays, while Part B covers 80% of approved services after a $226 annual deductible. Private insurance plans often have higher monthly premiums but may offer lower deductibles and caps on out-of-pocket expenses. For instance, a Medicare Advantage plan might limit annual out-of-pocket costs to $5,000, providing financial predictability. Assess your budget and health status—if you’re generally healthy, Medicare’s lower premiums might be preferable, but if you anticipate frequent medical needs, a private plan’s cost structure could be more advantageous.

Top Health Insurance Providers Covering Breast Reduction Surgery: A Guide

You may want to see also

Explore related products

![]()

Cost Analysis: Evaluate premiums, deductibles, copays, and out-of-pocket maximums for each plan

Premiums are the recurring payments that keep your Medicare plan active, and they’re the first line item to scrutinize. For instance, Medicare Part B premiums in 2023 start at $164.90 monthly for individuals earning under $97,000 annually, but rise to $560.50 for those earning above $500,000. When comparing plans, consider how these fixed costs align with your budget. A Medicare Advantage plan might bundle Part A, B, and D for a single premium, often lower than separate plans, but verify if the trade-off limits provider networks or coverage breadth.

Deductibles represent the amount you pay out-of-pocket before insurance coverage kicks in, and they vary wildly across plans. Original Medicare Part A has a $1,600 deductible per benefit period for hospital stays, while Part B’s deductible is $226 annually. Medicare Advantage plans often combine these into a single deductible, sometimes as low as $0, but may offset this with higher copays. For seniors on fixed incomes, a lower deductible plan might be preferable, even if it means slightly higher premiums.

Copays are the fixed fees you pay for specific services, like $25 for a doctor’s visit or $40 for a specialist. These small costs add up, especially for chronic conditions requiring frequent care. For example, a plan with a $10 copay for generic drugs might save you hundreds annually if you take multiple prescriptions. However, some plans waive copays for preventive services, making them ideal for those prioritizing routine care. Always calculate estimated annual copay expenses based on your healthcare usage patterns.

Out-of-pocket maximums cap your total spending, shielding you from catastrophic costs. Original Medicare has no out-of-pocket limit, but Medicare Advantage plans must cap this at $8,300 for in-network services in 2023. For those with high-risk health profiles, choosing a plan with a lower out-of-pocket maximum—even if premiums are higher—can provide financial security. Conversely, healthy individuals might opt for a higher maximum to reduce monthly premiums, betting on minimal healthcare needs.

To synthesize these factors, create a cost-comparison spreadsheet. List each plan’s premium, deductible, average copays for your common services, and out-of-pocket maximum. Multiply premiums by 12, estimate annual copays based on past usage, and add these to the deductible. The plan with the lowest total cost for your anticipated needs is often the best choice. However, factor in intangible costs like provider restrictions or prescription coverage gaps, as these can negate savings.

Travel Medical Insurance: United Credit Card Benefits Explained

You may want to see also

Explore related products

![]()

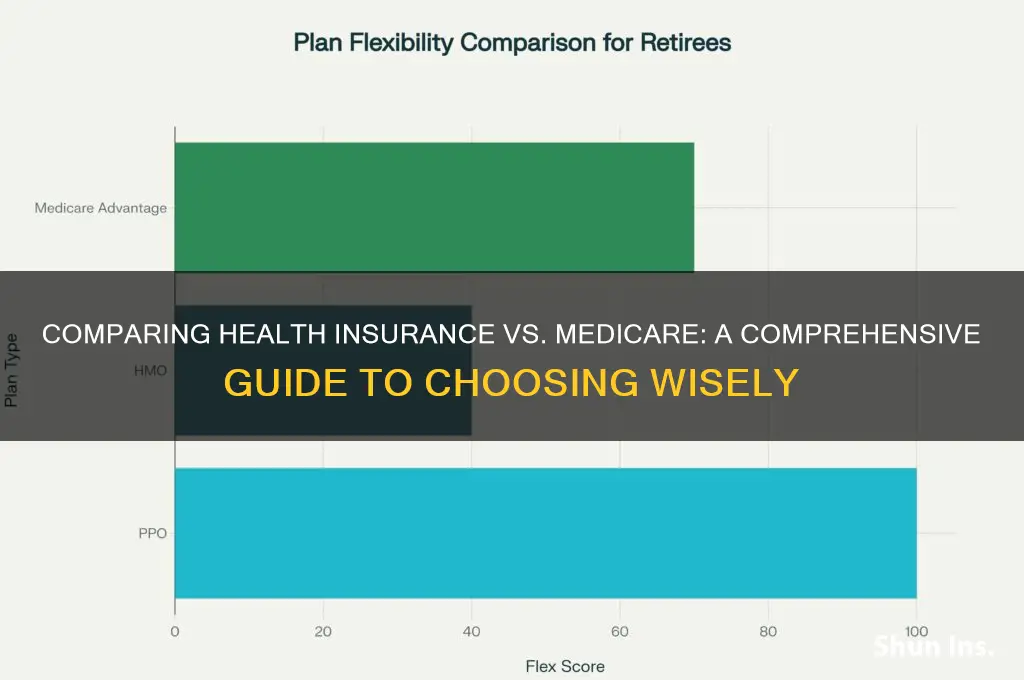

Provider Networks: Check if preferred doctors, hospitals, and specialists are in-network

One of the most critical yet overlooked aspects of comparing Medicare health insurance plans is verifying provider networks. Your preferred doctors, hospitals, and specialists may not be in-network with every plan, which can significantly impact your out-of-pocket costs and access to care. For instance, Original Medicare (Part A and Part B) typically allows you to visit any provider that accepts Medicare, but Medicare Advantage (Part C) plans often restrict you to a specific network. Before enrolling, cross-reference your current providers with the plan’s network directory, usually available on the insurer’s website. This small step can prevent unexpected expenses and ensure continuity of care, especially if you have an ongoing treatment plan or a trusted physician you’d like to keep.

Consider this scenario: You’ve been seeing the same cardiologist for years, and they’re not in-network with the Medicare Advantage plan you’re eyeing. Visiting them could cost you hundreds of dollars per visit, as out-of-network services are often not covered or covered at a lower rate. To avoid this, use the plan’s provider search tool to input your doctor’s name or specialty. If they’re not listed, contact the insurer directly to confirm—sometimes directories aren’t updated in real-time. Alternatively, if you’re open to switching providers, look for plans with larger networks or those that include top-rated hospitals in your area, such as those recognized by U.S. News & World Report for specialties like oncology or orthopedics.

For those with specific health needs, such as chronic conditions or upcoming surgeries, the provider network becomes even more crucial. Specialists like endocrinologists, rheumatologists, or neurologists may not be widely available in all networks. If you require frequent visits, ensure the plan covers both in-network and out-of-network specialist care, or prioritize plans with a robust specialist network. For example, some Medicare Advantage plans offer tiered networks, where certain specialists are only available at higher cost-sharing levels. Understanding these tiers can help you balance cost and access to the care you need.

Finally, don’t overlook the importance of hospital networks, especially if you have a preferred facility for surgeries or emergency care. Hospitals like Mayo Clinic or Cleveland Clinic may not be in-network with all plans, and out-of-network hospitalizations can lead to exorbitant costs. If you’re considering a Medicare Advantage plan, check if your preferred hospital is included and whether the plan requires prior authorization for certain procedures. For those on Original Medicare, most hospitals are covered, but supplemental plans like Medigap may offer additional benefits for out-of-network care. Always weigh the network restrictions against the plan’s premiums and benefits to find the best fit for your healthcare needs.

Understanding Medicaid Eligibility with Employer-Offered Insurance

You may want to see also

Explore related products

![]()

Prescription Drug Plans: Compare Part D coverage and formularies for medication needs

Medicare Part D plans are not one-size-fits-all, especially when it comes to prescription drug coverage. Each plan has its own formulary, a list of covered medications, which can significantly impact your out-of-pocket costs and access to necessary treatments. For instance, a 65-year-old with diabetes might find that one plan covers insulin glargine at a lower tier, meaning lower copays, while another plan places it in a higher tier, increasing costs. Understanding these differences is crucial for managing chronic conditions effectively.

To compare Part D plans, start by listing all medications you currently take, including dosage and frequency. Use Medicare’s Plan Finder tool to input this information and compare formularies across plans. Pay attention to tier placement, as drugs in lower tiers are generally less expensive. For example, a statin like atorvastatin 20mg might be in Tier 1 in one plan but Tier 2 in another, resulting in a monthly cost difference of $10 to $20. Additionally, check if your preferred pharmacy is in the plan’s network, as out-of-network pharmacies often charge higher prices.

Beware of plans with restrictive formularies that exclude certain medications or require prior authorization. For instance, a plan might cover only one type of antidepressant, limiting options if your doctor prescribes a specific brand. Similarly, some plans may impose quantity limits, such as a 30-day supply of a 90-day prescription, forcing you to refill more frequently. These limitations can disrupt treatment and increase administrative burdens, so read the plan’s summary of benefits carefully.

Finally, consider the trade-off between monthly premiums and out-of-pocket costs. A plan with a higher premium might offer lower copays for your medications, saving you money in the long run. For example, a plan with a $50 monthly premium and $5 copays for your drugs could be more cost-effective than a $20 premium plan with $25 copays. Evaluate your annual medication expenses and choose a plan that aligns with your budget and health needs. Regularly reviewing your Part D coverage during Medicare’s Annual Enrollment Period ensures you’re always getting the best value for your medication needs.

Vision Benefits: Are They Covered by My Medical Insurance?

You may want to see also

Explore related products

$10.86 $14.99

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UL320_.jpg)

![]()

Supplemental Options: Assess Medigap policies to fill Medicare Original gaps

Medicare Original, while comprehensive, leaves beneficiaries exposed to out-of-pocket costs like deductibles, copayments, and coinsurance. Medigap policies, also known as Medicare Supplement Insurance, are designed to bridge these gaps, offering standardized plans labeled A through N. Each plan provides a unique combination of benefits, allowing individuals to choose coverage tailored to their healthcare needs and budget. For instance, Plan F covers all Medicare-approved expenses not fully paid by Original Medicare, including the Part B deductible, while Plan G excludes this deductible but is often more cost-effective. Understanding these differences is crucial for maximizing financial protection.

When assessing Medigap policies, consider your healthcare utilization patterns and long-term financial goals. For example, if you frequently visit specialists or anticipate high prescription drug costs, a plan like F or G might be ideal. However, if you rarely require medical services, a lower-cost plan like K or L, which covers only a percentage of Medicare’s costs, could suffice. Additionally, note that Medigap policies do not cover services like dental, vision, or long-term care, so pairing them with standalone plans for these areas may be necessary. Age and location also influence premiums, with younger enrollees often securing lower rates.

A critical aspect of Medigap policies is the open enrollment period, which begins the month you turn 65 and have Part B. During this six-month window, insurers cannot deny coverage or charge higher premiums based on pre-existing conditions. Missing this period may result in medical underwriting, potentially increasing costs or limiting options. For those under 65 and eligible for Medicare due to disability, rules vary by state, so research local regulations carefully. Proactively enrolling during the open enrollment period ensures access to the best rates and coverage.

Comparing Medigap policies requires a balance between immediate needs and future flexibility. While Plan F offers the most comprehensive coverage, it is no longer available to new enrollees as of 2020, making Plan G the next best option for most. However, if you prioritize lower premiums, Plan N, which excludes coverage for Part B excess charges and requires copays for doctor visits and emergency room trips, might be more suitable. Use online comparison tools or consult a licensed insurance broker to evaluate premiums, benefits, and insurer ratings, ensuring the chosen policy aligns with your health and financial priorities.

Finally, remember that Medigap policies work exclusively with Original Medicare, not Medicare Advantage plans. If you’re considering switching from Medicare Advantage to Original Medicare, you have a guaranteed issue right to a Medigap policy during specific periods. Conversely, dropping a Medigap policy to join Medicare Advantage may complicate future re-enrollment. Weigh these factors carefully, as the decision impacts long-term healthcare coverage and costs. By thoroughly assessing Medigap options, you can fill the gaps in Medicare Original and secure a more predictable, affordable healthcare experience.

Will Insurance Cover Your Deductible? Understanding Your Policy's Role

You may want to see also

Frequently asked questions

Medicare is a federal health insurance program primarily for individuals aged 65 and older, while private health insurance is offered by private companies and can be tailored to various age groups and needs. Medicare typically covers hospital stays, doctor visits, and some prescription drugs, whereas private insurance plans may offer additional benefits like dental, vision, and wellness programs.

To compare Medicare plans, evaluate factors such as premiums, deductibles, out-of-pocket costs, prescription drug coverage, and provider networks. Use tools like the Medicare Plan Finder on the official Medicare website to compare Original Medicare, Medicare Advantage, and Part D prescription drug plans based on your specific healthcare needs and budget.

Yes, you can switch to Medicare when you become eligible, typically at age 65. However, it’s important to enroll during your Initial Enrollment Period to avoid penalties. Compare your current private insurance benefits with Medicare options to ensure you don’t lose coverage for services important to you, such as vision or dental care, which may not be covered under Original Medicare.

Medicare Advantage plans often include additional benefits like vision, dental, and prescription drug coverage, which Original Medicare does not cover. While Medicare Advantage may have lower premiums, it typically has provider networks and may require higher out-of-pocket costs for out-of-network care. Original Medicare offers more flexibility in choosing providers but may require supplemental plans like Medigap to cover additional costs.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)