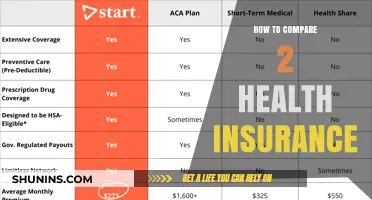

Comparing health insurance quotes is a crucial step in finding the right coverage that meets your needs and budget. To start, gather quotes from multiple providers, ensuring they include details on premiums, deductibles, copayments, and out-of-pocket maximums. Carefully review the coverage limits, exclusions, and network restrictions to understand what services are included and which providers are in-network. Pay attention to additional benefits like prescription drug coverage, mental health services, and preventive care, as these can vary significantly between plans. Use online comparison tools or consult with a licensed insurance broker to simplify the process and clarify any confusing terms or conditions. Finally, consider your personal health needs, financial situation, and long-term goals to choose a plan that offers the best value and protection for you and your family.

Comparing Health Insurance Quotes: Key Characteristics

| Characteristics | Values |

|---|---|

| Coverage Options | In-network vs. out-of-network coverage, preventive care, hospitalization, prescription drugs, mental health services, maternity care, specialist visits, pre-existing conditions coverage |

| Premiums | Monthly cost, annual cost, potential for premium increases |

| Deductibles | Amount you pay out-of-pocket before insurance kicks in, individual vs. family deductibles |

| Co-pays & Co-insurance | Fixed amount paid per visit/service (co-pay), percentage of cost shared with insurer (co-insurance) |

| Out-of-Pocket Maximum | Maximum amount you'll pay annually for covered services |

| Provider Network | Size and accessibility of network, inclusion of preferred doctors/hospitals |

| Prescription Drug Coverage | Formulary (list of covered drugs), tiers of coverage, generic vs. brand-name drug costs |

| Telehealth Services | Availability and coverage for virtual doctor visits |

| Preventive Care Coverage | Coverage for check-ups, screenings, vaccinations |

| Maternity & Newborn Care | Coverage for prenatal care, delivery, postpartum care, newborn care |

| Mental Health & Substance Abuse Coverage | Inpatient and outpatient treatment coverage, therapy sessions |

| Pre-existing Conditions | Coverage for conditions existing before policy start date (guaranteed under ACA in the US) |

| Customer Service & Reviews | Reputation for claims processing, customer support, online tools and resources |

| Policy Exclusions & Limitations | Services not covered, waiting periods, pre-authorization requirements |

| Additional Benefits | Vision, dental, wellness programs, gym memberships |

Explore related products

What You'll Learn

- Understand Coverage Limits: Check what each policy covers, including hospitalization, prescriptions, and specialist visits

- Compare Premiums & Deductibles: Evaluate monthly costs versus out-of-pocket expenses for each plan

- Review Network Providers: Ensure your preferred doctors and hospitals are in-network

- Analyze Additional Benefits: Look for extras like dental, vision, or wellness programs

- Check Customer Reviews: Assess insurer reputation and customer satisfaction for claims processing

![]()

Understand Coverage Limits: Check what each policy covers, including hospitalization, prescriptions, and specialist visits

Health insurance policies often look similar at first glance, but their coverage limits can vary dramatically. A plan with a low monthly premium might seem appealing, but it could leave you with high out-of-pocket costs if it caps hospitalization coverage at $100,000 per year while another plan offers unlimited coverage. Similarly, prescription drug coverage can differ widely—some policies cover only generic medications, while others include brand-name drugs but with high copays. Specialist visits, too, may be limited to a certain number per year or require prior authorization, which can delay necessary care. Understanding these limits is crucial to avoid unexpected expenses and ensure you have the care you need.

To effectively compare coverage limits, start by listing your anticipated healthcare needs. For instance, if you have a chronic condition requiring frequent specialist visits, prioritize policies with higher visit allowances or lower copays. For prescriptions, check the plan’s formulary—a list of covered medications—and note if your current medications are included. If you’re on a brand-name drug like insulin (which can cost up to $300 per vial without coverage), ensure the policy covers it at a manageable cost. Hospitalization limits are equally critical; consider your age, health status, and family medical history. Younger, healthier individuals might opt for lower limits to save on premiums, but those with higher risk factors should seek comprehensive coverage.

A practical tip is to use a spreadsheet to compare policies side by side. List categories like hospitalization, prescriptions, and specialist visits, then fill in the details for each plan. For example, under hospitalization, note the annual limit and whether it includes intensive care or emergency room visits. For prescriptions, specify if the plan covers generics, brand-name drugs, or both, and list copay amounts. This visual comparison makes it easier to identify gaps in coverage and choose a plan aligned with your needs.

Finally, don’t overlook the fine print. Some policies may advertise broad coverage but impose hidden restrictions, such as excluding certain procedures or requiring lengthy pre-authorization processes. For instance, a plan might cover specialist visits but limit them to in-network providers, which could be scarce in your area. Similarly, prescription coverage may exclude newer, high-cost medications, leaving you to pay out of pocket. By scrutinizing these details, you can avoid policies that appear comprehensive but fall short when you need them most. Understanding coverage limits isn’t just about comparing numbers—it’s about ensuring your insurance works for your unique health situation.

Who Insures E-Liquid Companies? A Guide to Vape Industry Coverage

You may want to see also

Explore related products

![]()

Compare Premiums & Deductibles: Evaluate monthly costs versus out-of-pocket expenses for each plan

Health insurance plans often present a trade-off between monthly premiums and out-of-pocket costs, such as deductibles. A plan with a lower monthly premium typically comes with a higher deductible, meaning you'll pay more when you need medical care. Conversely, a higher premium plan usually offers a lower deductible, reducing your costs at the point of service. For instance, a 30-year-old individual might choose a plan with a $200 monthly premium and a $3,000 deductible, while a 55-year-old with more frequent medical needs may opt for a $500 premium plan with a $1,000 deductible. Understanding this balance is crucial for selecting a plan that aligns with your healthcare usage and financial situation.

To effectively compare premiums and deductibles, start by assessing your annual healthcare expenses. If you rarely visit the doctor and have no chronic conditions, a high-deductible plan paired with a Health Savings Account (HSA) could save you money. For example, if your annual medical costs are around $1,500, a plan with a $2,500 deductible and a $150 monthly premium might be cost-effective. However, if you anticipate frequent doctor visits or prescription needs, a lower deductible plan, even with higher premiums, could prevent unexpected financial strain. Tools like online calculators can help estimate total yearly costs for each plan based on your expected usage.

Consider the impact of age and health status on your decision. Younger, healthier individuals often benefit from high-deductible plans, as they’re less likely to meet a high deductible. For example, a 25-year-old with no pre-existing conditions might save $1,200 annually by choosing a high-deductible plan over a low-deductible one. In contrast, older adults or those with chronic illnesses may find lower-deductible plans more economical, as they’re more likely to exceed the deductible threshold. A 60-year-old with diabetes, for instance, could save $2,500 annually by opting for a plan with a $1,000 deductible instead of a $3,000 one.

When evaluating plans, don’t overlook additional out-of-pocket costs like copays and coinsurance, which can significantly affect overall expenses. A plan with a $300 premium and a $1,500 deductible might seem affordable until you factor in $50 specialist copays and 20% coinsurance for procedures. For a family of four, these additional costs could add up to $1,000 annually, making a slightly higher-premium plan with lower copays and coinsurance a better value. Always review the Summary of Benefits and Coverage (SBC) to understand the full cost structure of each plan.

Finally, think long-term when comparing premiums and deductibles. If you’re in a life stage where healthcare needs are likely to increase—such as planning for pregnancy or managing aging parents—investing in a lower-deductible plan now could provide financial stability later. For example, a couple expecting a child might save $3,000 in out-of-pocket costs by choosing a plan with a $2,000 deductible over a $4,000 one. Conversely, if your health and lifestyle are stable, sticking with a high-deductible plan could yield significant savings over time. Regularly reassess your plan during open enrollment to ensure it continues to meet your evolving needs.

Insurance Stocks Plunge: Unraveling the Decline in Market Value

You may want to see also

Explore related products

![]()

Review Network Providers: Ensure your preferred doctors and hospitals are in-network

One of the most critical yet overlooked aspects of comparing health insurance quotes is verifying that your preferred healthcare providers are in-network. Out-of-network care can result in significantly higher out-of-pocket costs, even if the plan seems affordable upfront. Start by compiling a list of your current doctors, specialists, and hospitals you trust or frequently visit. Most insurance companies offer online provider directories where you can cross-reference these names. If you’re switching plans, this step is non-negotiable—don’t assume your current providers will remain in-network under a new policy.

Consider this scenario: You’re a 35-year-old with a primary care physician you’ve seen for years and a specialist managing a chronic condition. A plan with a lower monthly premium might exclude these providers, forcing you to pay 50–70% more for out-of-network visits. Over a year, this could add up to thousands of dollars in unexpected expenses. To avoid this, prioritize plans that include your essential providers, even if the premium is slightly higher. Use the insurance company’s online tools or call their customer service to confirm network status, as directories aren’t always up-to-date.

If you’re flexible with providers, use this as an opportunity to evaluate network quality. Larger networks often include top-rated hospitals and specialists, which can be crucial for complex medical needs. For instance, if you’re over 50 or have a family history of heart disease, ensure the plan includes cardiologists and hospitals with high success rates in cardiac care. Conversely, if you’re generally healthy and only need routine care, a narrower network with lower premiums might suffice. Balance your current needs with potential future scenarios to make an informed decision.

A practical tip: Don’t wait until you’re sick to discover your provider isn’t covered. During open enrollment or when comparing quotes, contact your preferred doctors’ offices directly to confirm they accept the plan you’re considering. Ask about any upcoming changes to their network participation, as providers can leave networks mid-year. Additionally, if you’re on prescription medications, verify that both the provider prescribing them and the pharmacy you use are in-network. This dual check ensures seamless care and avoids hidden costs.

Finally, weigh the trade-offs if your preferred providers aren’t in-network. Some plans offer out-of-network coverage, but it typically comes with higher deductibles, copays, and coinsurance. Calculate the potential costs for both in-network and out-of-network care based on your expected usage. For example, if you visit your out-of-network specialist four times a year at $300 per visit, that’s $1,200 annually—an amount that might justify paying a higher premium for in-network access. Ultimately, aligning your plan with your provider preferences ensures both financial and medical peace of mind.

Medical Emergencies: Family Insurance for Peace of Mind

You may want to see also

Explore related products

![]()

Analyze Additional Benefits: Look for extras like dental, vision, or wellness programs

Beyond the basics of coverage and cost, health insurance plans often include additional benefits that can significantly enhance your overall well-being. These extras, such as dental, vision, and wellness programs, are not always prominently featured in plan summaries but can provide substantial value. For instance, a plan with comprehensive dental coverage might include cleanings, fillings, and even orthodontic work, potentially saving you hundreds of dollars annually. Similarly, vision benefits can cover eye exams, glasses, or contact lenses, which are essential for maintaining good eye health. Wellness programs, on the other hand, may offer gym memberships, mental health resources, or smoking cessation aids, promoting a healthier lifestyle. When comparing health insurance quotes, it’s crucial to scrutinize these additional benefits to ensure they align with your personal health needs and long-term goals.

To effectively analyze these extras, start by listing your specific health priorities. For example, if you wear glasses or have a family history of dental issues, prioritize plans with robust vision and dental coverage. Next, compare the scope of each benefit across different plans. Does the dental coverage include orthodontics for adults, or is it limited to basic services? Are there restrictions on the type of glasses or contact lenses covered under vision care? Wellness programs can vary widely, from discounted gym memberships to comprehensive mental health apps or nutrition counseling. Look for programs that offer tangible, actionable resources rather than vague promises of "wellness support." Additionally, check if these benefits come with out-of-pocket costs or if they are fully covered under the plan.

A comparative approach can help you identify the best value. For instance, Plan A might offer extensive dental coverage but limited vision benefits, while Plan B provides excellent vision care and a robust wellness program but minimal dental coverage. If you rarely visit the dentist but need frequent eye care and are committed to fitness, Plan B might be the better choice. Conversely, a family with children who need braces and regular dental check-ups may find Plan A more cost-effective. Consider using a spreadsheet to compare these benefits side by side, ensuring you don’t overlook any details.

Finally, don’t underestimate the long-term impact of these additional benefits on your health and finances. For example, regular dental check-ups can prevent costly procedures down the line, while access to a wellness program might help you manage chronic conditions more effectively. Vision care is particularly important for children and older adults, as early detection of eye issues can prevent serious complications. By taking the time to analyze these extras, you’re not just comparing insurance plans—you’re investing in a healthier future. Practical tip: If a plan’s additional benefits aren’t clearly outlined, contact the insurer directly for detailed information. This small step can make a big difference in your decision-making process.

Startup Guide: Selecting the Right Health Insurance for Your Team

You may want to see also

Explore related products

$8.59 $18.15

![]()

Check Customer Reviews: Assess insurer reputation and customer satisfaction for claims processing

Customer reviews are a goldmine of insights when comparing health insurance quotes, offering a glimpse into the real-world experiences of policyholders. While insurers may promise seamless claims processing, it’s the feedback from actual customers that reveals how well they deliver on those promises. Scour platforms like Trustpilot, Consumer Affairs, or the Better Business Bureau to gauge satisfaction levels. Look for recurring themes—are customers praising quick reimbursements, or are they frustrated by delays and denials? Patterns in reviews can highlight red flags or confirm an insurer’s reliability, helping you avoid companies with a history of poor claims handling.

Analyzing reviews requires a critical eye. Don’t just skim star ratings; dive into the details. Pay attention to how insurers respond to negative feedback. A company that addresses complaints professionally and offers resolutions demonstrates accountability, a trait that could benefit you during claims disputes. Conversely, dismissive or absent responses may indicate a lack of customer care. Cross-reference reviews with independent ratings from organizations like J.D. Power or the National Committee for Quality Assurance (NCQA) for a more comprehensive view of an insurer’s reputation.

Practical tip: Filter reviews by age group or policy type if possible, as experiences can vary. For instance, younger policyholders might prioritize digital claims processing, while seniors may value personalized customer service. If you’re comparing plans for a family, look for reviews from policyholders with similar needs, such as frequent pediatric claims or maternity coverage. This tailored approach ensures the reviews you’re assessing align with your specific expectations.

While customer reviews are invaluable, they’re not infallible. Some reviews may be biased, exaggerated, or outdated. To mitigate this, focus on recent reviews (within the past year) and look for consistency across multiple sources. Additionally, balance qualitative feedback with quantitative data, such as claims approval rates or average processing times, which insurers may disclose in their marketing materials or regulatory filings. This dual approach ensures you’re making an informed decision based on both personal experiences and hard metrics.

Ultimately, checking customer reviews isn’t just about avoiding bad insurers—it’s about finding the best fit for your needs. A company with glowing reviews for claims processing might still fall short in other areas, like network coverage or premium costs. Use reviews as one piece of the puzzle, weighing them against other factors like policy benefits, provider networks, and affordability. By doing so, you’ll not only identify an insurer with a strong reputation but also one that aligns with your priorities and expectations.

Health Insurance: Trust, Transparency, and Your Financial Security Explained

You may want to see also

Frequently asked questions

Focus on premiums, deductibles, out-of-pocket maximums, network coverage, prescription drug benefits, and included services like preventive care or specialist visits.

Check if your preferred doctors, hospitals, and specialists are in-network to avoid higher out-of-network costs. Use the insurer’s provider directory for verification.

It depends on your health needs. Lower premiums often mean higher deductibles, suitable for those who rarely need care. Lower deductibles are better if you anticipate frequent medical expenses.

Review the plan’s coverage details for services you require, such as mental health care, maternity care, or chronic condition management, and confirm any exclusions or limitations.