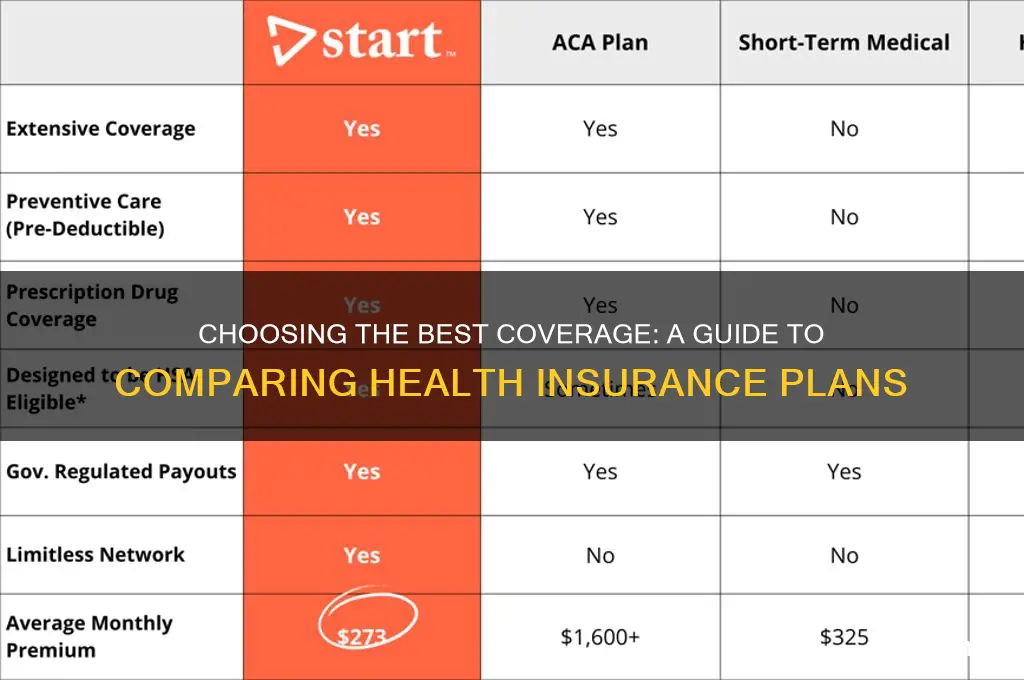

Comparing two health insurance plans requires a careful evaluation of several key factors to ensure you choose the best option for your needs. Start by examining the monthly premiums, deductibles, and out-of-pocket maximums, as these directly impact your costs. Next, assess the coverage scope, including which medical services, prescriptions, and specialists are included or excluded. Consider the network of providers each plan offers, as staying in-network can significantly reduce expenses. Additionally, review co-pays, co-insurance rates, and any additional benefits like preventive care, mental health services, or telemedicine options. Finally, check customer reviews and the insurer’s reputation for customer service and claims processing efficiency. By systematically comparing these elements, you can make an informed decision that balances cost and coverage.

Explore related products

What You'll Learn

- Coverage Analysis: Compare benefits, exclusions, and limits for hospitalization, treatments, and pre-existing conditions

- Premium Costs: Evaluate monthly/annual premiums, payment flexibility, and long-term affordability

- Network Providers: Check hospital and doctor networks for accessibility and preferred healthcare providers

- Claim Process: Assess ease of filing claims, settlement ratios, and customer support efficiency

- Add-On Benefits: Compare additional features like maternity cover, critical illness, or wellness programs

![]()

Coverage Analysis: Compare benefits, exclusions, and limits for hospitalization, treatments, and pre-existing conditions

Health insurance policies often differ significantly in what they cover, exclude, and limit, making a detailed coverage analysis essential. Start by listing the benefits each plan offers for hospitalization, such as room charges, ICU stays, and surgeon fees. For instance, Plan A might cover up to $5,000 per day for a private room, while Plan B caps it at $3,000 but includes a longer maximum stay. Identify which plan aligns better with your anticipated needs—frequent travelers might prioritize higher daily limits, while those with chronic conditions may benefit from extended stay coverage.

Next, scrutinize exclusions, the fine print that can derail your financial plans. Treatments like cosmetic surgery, alternative therapies, or specific medications (e.g., high-cost biologics) are often excluded. For example, Plan A may exclude all mental health treatments, while Plan B covers outpatient therapy but not inpatient psychiatric care. Cross-reference these exclusions with your medical history and lifestyle. If you’re prone to allergies requiring immunotherapy, a plan excluding such treatments could leave you vulnerable to out-of-pocket expenses.

Limits—annual, lifetime, or per-incident—are another critical factor. A plan might offer comprehensive hospitalization coverage but cap chemotherapy sessions at 12 per year, insufficient for some cancer treatments. Compare these limits against average healthcare costs in your region. For instance, if knee replacement surgery averages $35,000 in your area, a plan with a $30,000 limit for orthopedic procedures could leave you underinsured.

Pre-existing conditions require special attention. Some insurers impose waiting periods (e.g., 2 years) before covering conditions like diabetes or hypertension, while others exclude them entirely. If you have a pre-existing condition, prioritize plans with shorter waiting periods or those that offer partial coverage during the waiting period. For example, Plan A might cover 50% of diabetes-related expenses after 1 year, while Plan B provides no coverage until year 3.

Finally, consider practical tips to streamline your analysis. Create a comparison table listing benefits, exclusions, and limits side by side. Use real-life scenarios—imagine a 3-day hospital stay or a course of physical therapy—to estimate out-of-pocket costs under each plan. Consult a broker or use online tools to decode complex policy language. Remember, the goal isn’t to find the cheapest plan but the one that offers the most comprehensive, relevant coverage for your health profile and lifestyle.

Dermatologist and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Premium Costs: Evaluate monthly/annual premiums, payment flexibility, and long-term affordability

Premium costs are the backbone of any health insurance comparison, but they’re more than just a number on a page. Start by laying out the monthly or annual premiums side by side. For instance, Plan A might charge $300 monthly, while Plan B costs $250. At first glance, Plan B seems cheaper, but dig deeper. Does Plan A offer more comprehensive coverage or lower out-of-pocket costs that could save you money in the long run? Use a spreadsheet to compare these figures directly, ensuring you account for all variables. This initial step is critical—it sets the stage for understanding the financial commitment you’re making.

Payment flexibility is often overlooked but can significantly impact your budget. Some insurers allow quarterly or annual payments, which might reduce overall costs through discounts. Others offer autopay options that could save you 5–10% on premiums. For example, if Plan A offers a 7% discount for annual payments, that $300 monthly premium could effectively drop to $279. Conversely, Plan B might only accept monthly payments, limiting your flexibility. Evaluate your cash flow and financial habits to determine which payment structure aligns best with your lifestyle. Rigid payment terms can turn a seemingly affordable plan into a financial burden.

Long-term affordability requires a forward-thinking approach. Premiums often increase annually, so consider how these hikes might affect your budget over time. For instance, if Plan A historically raises premiums by 5% yearly, your $300 monthly cost could balloon to $380 in five years. Plan B, with a 3% increase, would only reach $323. Factor in inflation, potential income changes, and life events like retirement or family expansion. A plan that’s affordable now might not be sustainable in a decade. Use online calculators to project these costs, ensuring you’re not just choosing for today but for the years ahead.

Practical tip: Don’t forget to assess penalties for missed payments or late fees, which can add up quickly. Some insurers charge up to $25 per late payment, while others offer grace periods. Additionally, inquire about premium adjustments based on age or health status. For example, premiums often spike after age 50, so a plan that’s affordable in your 30s might become prohibitively expensive later. By scrutinizing these details, you’ll avoid hidden costs and ensure your chosen plan remains within reach over time.

In conclusion, evaluating premium costs isn’t just about finding the lowest number—it’s about aligning payment structures, flexibility, and long-term projections with your financial reality. A plan that offers discounts for annual payments or has a history of modest premium increases could save you thousands over time. Conversely, rigid payment terms or steep annual hikes can turn a seemingly affordable option into a financial strain. By taking a holistic view of premiums, you’ll make a decision that’s not just cost-effective today but sustainable for years to come.

Health Insurers: Monopolistic Competition or Perfect Market Dynamics?

You may want to see also

Explore related products

![]()

Network Providers: Check hospital and doctor networks for accessibility and preferred healthcare providers

One of the most critical yet overlooked aspects of comparing health insurance plans is the network of providers each plan covers. A plan’s network determines where and from whom you can receive care without incurring out-of-pocket costs. For instance, if your preferred cardiologist or local hospital isn’t in-network, you could face significantly higher expenses or be forced to switch providers. Start by listing the doctors, specialists, and hospitals you currently use or would prefer to access. Then, cross-reference this list with each plan’s provider directory, often available online. This simple step can prevent unexpected costs and ensure continuity of care.

Analyzing network accessibility goes beyond confirming names on a list. Consider geographic coverage, especially if you travel frequently or live in a rural area. A plan with a narrow network might offer lower premiums but limit your options to a small cluster of providers. Conversely, a broader network may come with higher costs but provide flexibility. For example, a plan with a national network like Aetna or UnitedHealthcare could be advantageous if you split time between states. Additionally, check if the network includes urgent care centers or telehealth services, which can be lifesavers for minor illnesses or after-hours needs.

Preferred healthcare providers often dictate the quality and convenience of your care. If you have a chronic condition, such as diabetes or hypertension, ensure the plan’s network includes specialists and facilities experienced in managing your specific needs. For instance, a plan that includes access to a top-tier cancer center like MD Anderson or Mayo Clinic could be invaluable if you’re at high risk for certain diseases. Similarly, if you prioritize holistic or alternative medicine, verify that the network includes integrative health providers. Don’t assume all plans cover the same types of care—some may exclude naturopaths, acupuncturists, or mental health professionals from their networks.

A practical tip for evaluating networks is to simulate real-life scenarios. Imagine you need emergency care—does the plan cover out-of-network hospitals in urgent situations, or will you be responsible for a portion of the bill? What if you require a specialist referral? Some plans mandate in-network referrals, while others allow more flexibility. Another strategy is to call your preferred providers directly and ask if they accept both plans you’re comparing. This can uncover discrepancies in the insurer’s directory, which may not always be up-to-date.

Ultimately, the network providers in a health insurance plan can significantly impact your healthcare experience and costs. A plan with a robust, accessible network tailored to your needs can save you money and hassle in the long run. Conversely, a plan with limited options might lead to frustration and unexpected expenses. By meticulously comparing networks, you’re not just choosing an insurance plan—you’re securing peace of mind and ensuring you can access the care you need, when and where you need it.

Getting Medical Insurance: The Right Age to Start

You may want to see also

Explore related products

![]()

Claim Process: Assess ease of filing claims, settlement ratios, and customer support efficiency

Filing a health insurance claim should be straightforward, but the reality often involves navigating complex paperwork, unclear guidelines, and frustrating delays. When comparing two health insurance plans, scrutinize the claim process as if you’re already in a hospital bed—because that’s when it truly matters. Look for insurers that offer digital claim filing (via app or portal) with step-by-step guidance, as this reduces errors and speeds up processing. For instance, Insurer A might allow cashless claims at 8,000+ network hospitals, while Insurer B requires manual submission of physical documents, which can take weeks longer. Prioritize plans that simplify this process, especially if you’re in an age group (e.g., seniors or young professionals) where quick access to funds is critical.

Settlement ratios are the unsung hero of health insurance comparisons. This metric reveals the percentage of claims an insurer actually pays out. A settlement ratio of 95% means the company settles 95 out of 100 claims, while a 70% ratio should raise red flags. Cross-reference this with customer reviews to spot patterns—does Insurer X frequently deny claims for pre-existing conditions, or does Insurer Y delay payouts for high-value treatments? For example, if you’re comparing plans for a family with a history of chronic illnesses, a higher settlement ratio for critical illnesses could save you thousands in out-of-pocket expenses.

Customer support efficiency isn’t just about polite representatives—it’s about resolving issues during high-stress moments. Test this by calling both insurers’ helplines with a hypothetical claim scenario. Note response times, clarity of information, and whether they offer multilingual support (crucial for non-English speakers). Insurer A might have 24/7 support but lack expertise in handling complex claims, while Insurer B could provide dedicated claim managers but operate only during business hours. If you’re someone who values peace of mind over cost, prioritize insurers with robust support systems, even if premiums are slightly higher.

Finally, don’t overlook the fine print in claim policies. Some insurers cap payouts for specific treatments (e.g., ₹5 lakh for cancer care) or exclude certain procedures altogether. Others may require pre-authorization for hospital admissions, adding an extra layer of bureaucracy. For instance, Insurer B might cover alternative therapies like Ayurveda, while Insurer A sticks to conventional treatments. Align these details with your health needs—if you’re an athlete prone to injuries, ensure physiotherapy is covered without hidden limits. A plan that looks cheaper upfront might cost more in the long run if its claim process is riddled with exclusions and delays.

Medical Insurance: Telling HR About Its Poor Performance

You may want to see also

Explore related products

![]()

Add-On Benefits: Compare additional features like maternity cover, critical illness, or wellness programs

Health insurance policies often differentiate themselves through add-on benefits, which can significantly impact your coverage and out-of-pocket expenses. When comparing two plans, scrutinize these additional features to ensure they align with your current and future needs. For instance, maternity cover is a critical add-on for individuals or couples planning to start a family. It typically includes pre-natal care, delivery expenses, and post-natal care, but coverage limits and waiting periods vary widely. One policy might offer up to ₹5 lakh for maternity-related expenses with a 2-year waiting period, while another might cap it at ₹3 lakh with a 4-year waiting period. Understanding these nuances ensures you’re not caught off guard during a life milestone.

Critical illness coverage is another add-on that warrants careful comparison. This benefit provides a lump-sum payout upon diagnosis of severe conditions like cancer, heart attack, or stroke. However, the list of covered illnesses and payout amounts differ across policies. For example, Policy A might cover 15 critical illnesses with a payout of ₹10 lakh, while Policy B covers 20 illnesses but offers only ₹8 lakh. Additionally, some policies require a survival period (e.g., 30 days post-diagnosis) before releasing the payout. If you have a family history of specific ailments, prioritize a policy with comprehensive coverage for those conditions.

Wellness programs are increasingly popular add-ons, designed to encourage policyholders to maintain a healthy lifestyle. These programs often include gym memberships, nutrition consultations, or discounts on health screenings. However, their value depends on your willingness to engage with them. For instance, Policy X might offer a free annual health check-up and a 20% discount on fitness trackers, while Policy Y provides access to a wellness app with personalized health plans. If you’re already health-conscious, these perks could add tangible value. Otherwise, they might be unnecessary extras driving up your premium.

When evaluating add-ons, consider your life stage and long-term goals. A 25-year-old single professional might prioritize critical illness coverage over maternity benefits, while a 35-year-old couple would likely value both. Additionally, assess the cost-benefit ratio. Some add-ons increase premiums significantly but offer limited utility. For example, a wellness program might add ₹2,000 annually to your premium but save you only ₹1,500 in gym fees. Finally, read the fine print for exclusions and conditions. A maternity cover might exclude complications like pre-term labor, or a critical illness payout might not cover experimental treatments. By dissecting these details, you can choose a policy whose add-ons genuinely enhance your coverage rather than merely inflate its price.

Does Higher Pay Mean Higher Health Insurance Premiums? Exploring the Link

You may want to see also

Frequently asked questions

When comparing health insurance plans, focus on premiums, deductibles, out-of-pocket maximums, network coverage, prescription drug coverage, and included services (e.g., preventive care, mental health, or maternity care). Also, check if your preferred doctors and hospitals are in-network.

Evaluate your healthcare usage (e.g., frequent doctor visits, chronic conditions, or prescriptions) and compare the total costs, including premiums, deductibles, and copays/coinsurance. A plan with higher premiums but lower out-of-pocket costs may be better if you use healthcare often.

Prioritize based on your health needs and budget. If you rarely visit the doctor, a lower premium with a higher deductible might save you money. If you need frequent medical care, a higher premium with a lower deductible could reduce overall costs.

The provider network is crucial because plans with narrow networks may limit your choice of doctors and hospitals. Ensure your preferred healthcare providers are in-network to avoid higher out-of-network costs or lack of coverage. Check the plan’s network directory before deciding.