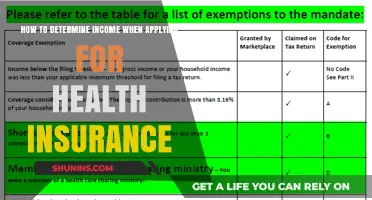

Determining mental health tier insurance involves understanding the specific coverage levels offered by your insurance plan for mental health services. Insurance providers typically categorize mental health care into tiers, which dictate the extent of coverage, out-of-pocket costs, and access to providers. These tiers often align with the type of service, such as therapy sessions, psychiatric consultations, or inpatient treatment, and may vary based on the plan’s structure, such as HMO, PPO, or EPO. To determine your mental health tier, review your insurance policy documents, contact your insurance provider directly, or consult with a benefits specialist. Understanding your tier is crucial for managing costs and ensuring access to the mental health care you need.

Mental Health Tier Insurance Characteristics

| Characteristics | Values |

|---|---|

| Tier Level | Typically categorized as Tier 1 (lowest cost, most restrictive), Tier 2, Tier 3, and sometimes Tier 4 (highest cost, most comprehensive) |

| Network Coverage | In-network providers offer lower out-of-pocket costs. Out-of-network providers may be covered at a reduced rate or not at all. |

| Deductible | The amount you pay out-of-pocket before insurance coverage kicks in. Deductibles can vary significantly between tiers. |

| Copay/Coinsurance | Fixed fee (copay) or percentage (coinsurance) you pay for each mental health visit. Tiers often have different copay/coinsurance rates. |

| Out-of-Pocket Maximum | The maximum amount you'll pay for covered services in a year. Higher tiers usually have higher out-of-pocket maximums. |

| Covered Services | Varies by tier and plan. May include therapy sessions, psychiatric consultations, medication management, inpatient/outpatient treatment, and crisis intervention. |

| Pre-authorization Requirements | Some tiers may require pre-authorization for certain services, like inpatient treatment or specialized therapies. |

| Provider Availability | Higher tiers often offer access to a wider network of mental health providers. |

| Medication Coverage | Coverage for psychiatric medications may vary by tier, including formulary restrictions and prior authorization requirements. |

| Telehealth Coverage | Some plans may offer telehealth mental health services, with coverage varying by tier. |

Explore related products

What You'll Learn

- Understanding Tiered Plans: Learn how insurance tiers categorize mental health coverage levels

- Coverage Limits: Check session caps, medication coverage, and hospitalization limits per tier

- Provider Networks: Verify in-network mental health providers available under each insurance tier

- Cost Comparison: Compare premiums, deductibles, and copays across different mental health tiers

- Policy Exclusions: Identify services or conditions not covered in specific mental health tiers

![]()

Understanding Tiered Plans: Learn how insurance tiers categorize mental health coverage levels

Insurance plans often use tiered systems to categorize coverage levels, and mental health services are no exception. These tiers—typically labeled as Bronze, Silver, Gold, and Platinum—dictate how much you’ll pay out-of-pocket for therapy, medication, and other treatments. For instance, a Bronze plan might cover 60% of mental health costs, leaving you responsible for the remaining 40%, while a Platinum plan could cover 90%. Understanding these tiers is crucial for budgeting and ensuring you receive the care you need without unexpected expenses.

Consider a scenario where you require weekly therapy sessions at $120 each. Under a Bronze plan, you might pay $72 per session, totaling $3,744 annually for 52 sessions. In contrast, a Platinum plan could reduce your cost to $12 per session, or $624 annually. This stark difference highlights why tier selection matters. To determine the best tier, evaluate your current and anticipated mental health needs, including frequency of therapy, medication costs, and potential hospitalization.

Analyzing the specifics of each tier reveals hidden nuances. For example, some plans may offer lower copays for in-network providers but exclude coverage for out-of-network specialists. Others might cap the number of therapy sessions per year, such as 20 visits, after which you’d pay full price. Review the Summary of Benefits and Coverage (SBC) document provided by your insurer to identify these details. Look for terms like "coinsurance," "deductible," and "out-of-pocket maximum" to understand your financial responsibility.

A persuasive argument for higher-tier plans is their long-term cost-effectiveness for individuals with chronic or severe mental health conditions. While premiums are higher, the reduced out-of-pocket costs for frequent treatments can save money over time. For example, a Gold plan with a $500 monthly premium might save you $2,000 annually compared to a Bronze plan if you require extensive care. Conversely, if you rarely use mental health services, a lower-tier plan could be more economical.

Finally, practical tips can streamline your decision-making process. Start by listing all potential mental health expenses, including therapy, psychiatry visits, and medications. Compare these costs across tiers using your insurer’s cost estimator tool. If you’re unsure about future needs, opt for a middle-tier plan like Silver, which balances premiums and coverage. Additionally, leverage employer-sponsored wellness programs or community resources to supplement insurance gaps. By strategically navigating tiered plans, you can secure adequate mental health coverage without overspending.

Strategies for Sending Medical Bills After Primary Insurance Payment

You may want to see also

Explore related products

![]()

Coverage Limits: Check session caps, medication coverage, and hospitalization limits per tier

Mental health insurance tiers often dictate how much you can access therapy sessions, medications, and inpatient care—and these limits vary wildly. For instance, a Bronze plan might cap therapy at 10 sessions annually, while a Platinum plan could offer unlimited visits. Medication coverage can range from generic-only options to comprehensive brand-name inclusions, with copays differing by tier. Hospitalization limits are equally critical: some plans restrict inpatient stays to 15 days per year, while others provide up to 60 days. Understanding these caps ensures you’re not blindsided by out-of-pocket costs when you need care most.

To navigate these limits effectively, start by reviewing your plan’s Summary of Benefits and Coverage (SBC). Look for specific terms like "session maximums," "formulary tiers," and "inpatient day limits." For example, if you’re prescribed an antidepressant like escitalopram, check if it’s covered under Tier 1 (lowest copay) or Tier 3 (highest copay). If you’re in therapy, note whether the cap resets annually or per condition. Pro tip: If you anticipate needing frequent care, consider a higher-tier plan to avoid hitting limits mid-treatment.

Comparing tiers reveals stark differences in coverage generosity. A Silver plan might cover 80% of medication costs after a $20 copay, while a Bronze plan could leave you paying 40% coinsurance with no copay cap. Hospitalization limits are even more dramatic: a Gold plan might fully cover a 30-day stay, whereas a Bronze plan could leave you responsible for $5,000 in out-of-pocket costs after 10 days. For families or individuals with chronic mental health needs, these disparities can mean the difference between manageable care and financial strain.

Finally, don’t overlook the fine print. Some plans impose age-based restrictions, like limiting adolescent therapy sessions to 12 per year, or require preauthorization for inpatient stays. Others may exclude coverage for certain medications, such as long-acting injectables for schizophrenia. If you’re unsure, call your insurer directly to clarify limits and ask for examples of how they apply in real-world scenarios. Knowing these details upfront empowers you to choose a tier that aligns with your mental health needs—not just your budget.

Insurance Claims: When to Report an Accident

You may want to see also

Explore related products

![]()

Provider Networks: Verify in-network mental health providers available under each insurance tier

Insurance tiers often dictate access to mental health providers, making it crucial to verify in-network options before committing to a plan. Start by obtaining a provider directory from your insurance company, typically available online or upon request. Cross-reference this list with your preferred mental health professionals or specialties, such as psychiatrists, psychologists, or licensed therapists. If you’re already seeing a provider, confirm their participation in your tier’s network to avoid out-of-pocket costs. For instance, a Gold tier plan might offer access to a broader network, including specialists in trauma or addiction, while a Bronze tier may limit options to general practitioners. This step ensures alignment between your mental health needs and the plan’s coverage.

Analyzing provider networks across tiers reveals significant disparities in accessibility and quality. Higher-tier plans often include providers with shorter wait times and more flexible scheduling, whereas lower tiers may restrict access to overburdened clinics or telehealth-only options. For example, a Silver tier plan might cover in-person sessions with a licensed clinical social worker but exclude psychiatrists for medication management. Conversely, a Platinum tier could offer comprehensive care, including group therapy sessions or integrative treatment programs. Understanding these differences helps you prioritize what matters most—whether it’s cost, provider expertise, or treatment modality.

To streamline the verification process, use online tools like provider search portals or third-party platforms that filter mental health professionals by insurance tier. Input your plan details and location to generate a list of in-network providers, complete with contact information and specialties. For instance, Psychology Today’s “Find a Therapist” tool allows you to filter by insurance accepted, while some insurers offer mobile apps with real-time provider availability. If you’re unsure about a provider’s network status, call their office directly and ask if they accept your specific tier and plan type. This proactive approach prevents billing surprises and ensures uninterrupted care.

A cautionary note: provider networks can change annually, so reverify in-network status during open enrollment or after significant life events like moving or switching jobs. Insurance companies may drop providers mid-year, leaving you with unexpected out-of-network costs. For example, a therapist in-network under your current tier might not be covered if you downgrade to a lower tier next year. Keep a record of your verification efforts, including dates and representative names, to resolve disputes if billing issues arise. Staying informed about network changes empowers you to make timely adjustments to your mental health care plan.

Ultimately, verifying in-network mental health providers by tier is a cornerstone of maximizing insurance benefits while minimizing costs. It requires diligence—combining research, direct communication, and periodic updates—but pays dividends in accessible, affordable care. By understanding the nuances of each tier’s network, you can select a plan that not only fits your budget but also supports your mental health journey effectively. Treat this step as an investment in your well-being, ensuring that your insurance works for you, not against you.

Maximize Family Coverage: Combining Multiple Health Insurance Plans Effectively

You may want to see also

Explore related products

![]()

Cost Comparison: Compare premiums, deductibles, and copays across different mental health tiers

Understanding the cost implications of mental health insurance tiers is crucial for making informed decisions. Each tier—typically categorized as Bronze, Silver, Gold, or Platinum—offers varying levels of coverage, directly impacting premiums, deductibles, and copays. For instance, Bronze plans often have the lowest monthly premiums but come with higher out-of-pocket costs, while Platinum plans feature higher premiums but significantly lower deductibles and copays. This trade-off demands careful consideration of your mental health needs and financial situation.

To begin your cost comparison, start by examining premiums across tiers. Premiums are the monthly payments you make to maintain coverage. For a 30-year-old individual, a Bronze plan might cost $200 per month, while a Platinum plan could exceed $500. However, if you anticipate frequent therapy sessions or psychiatric consultations, the higher premium of a Platinum plan could offset the cumulative cost of copays and deductibles in a lower-tier plan. Use online tools like Healthcare.gov or insurance comparison platforms to input your age, location, and income for personalized premium estimates.

Next, analyze deductibles, the amount you pay out-of-pocket before insurance coverage kicks in. Mental health services often count toward this deductible, so a Bronze plan with a $6,000 deductible means you’ll pay that full amount before coverage begins. In contrast, a Gold plan might have a $1,000 deductible, making it more cost-effective if you require regular mental health care. Consider your annual mental health expenses—for example, weekly therapy sessions at $150 each—to determine which deductible aligns with your budget.

Copays, the fixed amount you pay per visit, also vary significantly across tiers. A Bronze plan might charge $60 per therapy session, while a Platinum plan could reduce this to $20 or less. For individuals needing specialized care, such as psychiatric evaluations or medication management, these differences can add up quickly. Calculate the annual cost of copays based on your expected frequency of visits to identify the most economical tier.

Finally, weigh the long-term financial impact of each tier. While a Bronze plan may seem affordable upfront, unexpected mental health needs could lead to substantial out-of-pocket expenses. Conversely, a Platinum plan’s higher premiums provide comprehensive coverage, minimizing financial stress during crises. For families or individuals with pre-existing mental health conditions, investing in a higher tier often proves more cost-effective over time. Use spreadsheets or budgeting apps to model different scenarios and choose the tier that balances affordability with adequate coverage.

Understanding Health Insurance: Age Limits for Dependent Coverage Explained

You may want to see also

Explore related products

![]()

Policy Exclusions: Identify services or conditions not covered in specific mental health tiers

Understanding policy exclusions is crucial when navigating mental health insurance tiers, as these exclusions can significantly impact the care you receive. Each tier—typically categorized as bronze, silver, gold, or platinum—may omit specific services or conditions, leaving you financially responsible for uncovered treatments. For instance, a bronze plan might exclude intensive outpatient programs (IOPs) or family therapy, while a gold plan could still limit coverage for specialized treatments like transcranial magnetic stimulation (TMS) for depression. Always review the Summary of Benefits and Coverage (SBC) to identify these gaps, as they vary widely between insurers and plans.

Consider the case of substance use disorder treatment, a common area for exclusions. Lower-tier plans often restrict access to residential rehab facilities or medication-assisted treatment (MAT) with drugs like buprenorphine or naltrexone. Even if a plan covers MAT, it might cap the number of prescriptions per year or require prior authorization, delaying critical care. Conversely, higher-tier plans may offer more comprehensive coverage but still exclude experimental therapies or long-term inpatient stays. Understanding these nuances ensures you select a plan aligned with your specific mental health needs.

Another critical area to scrutinize is coverage for pre-existing conditions. While the Affordable Care Act prohibits denying coverage for pre-existing mental health conditions, some plans may still exclude specific treatments related to these conditions. For example, a plan might cover therapy sessions for anxiety but exclude coverage for anxiety-related hospitalizations or intensive treatments like dialectical behavior therapy (DBT). Similarly, plans may exclude coverage for self-inflicted injuries or eating disorder treatments if they fall under certain diagnostic codes. Always cross-reference your medical history with the policy’s exclusion list to avoid unexpected out-of-pocket costs.

Practical tips can help you navigate these exclusions effectively. First, use the insurer’s online tool or call their customer service line to verify coverage for specific treatments or providers. Second, if you anticipate needing excluded services, consider supplemental insurance or health savings accounts (HSAs) to offset costs. Finally, document all communications with your insurer regarding exclusions—this can be invaluable if disputes arise. By proactively identifying and addressing policy exclusions, you can maximize your mental health benefits and minimize financial surprises.

Why Insurance Companies and Foundations Prefer Limited Partnerships

You may want to see also

Frequently asked questions

Mental health tiers refer to the levels of coverage provided by insurance plans for mental health services. These tiers typically categorize services into different levels of coverage, such as preventive care, outpatient therapy, inpatient treatment, and prescription medications.

To determine your mental health tier, review your insurance plan's Summary of Benefits and Coverage (SBC) or contact your insurance provider directly. Look for sections related to mental health and substance use disorder services, which should outline the specific coverage levels or tiers for different types of care.

No, mental health tiers can vary significantly between insurance plans and providers. Some plans may offer more comprehensive coverage with lower out-of-pocket costs, while others may have higher deductibles, copays, or limitations on certain services. It's essential to review your specific plan details.

Yes, if you disagree with your insurance company's decision regarding mental health coverage tiers or denied claims, you have the right to appeal. Start by reviewing your plan's appeals process, gather supporting documentation from your healthcare provider, and submit a formal appeal to your insurance company within the specified timeframe.