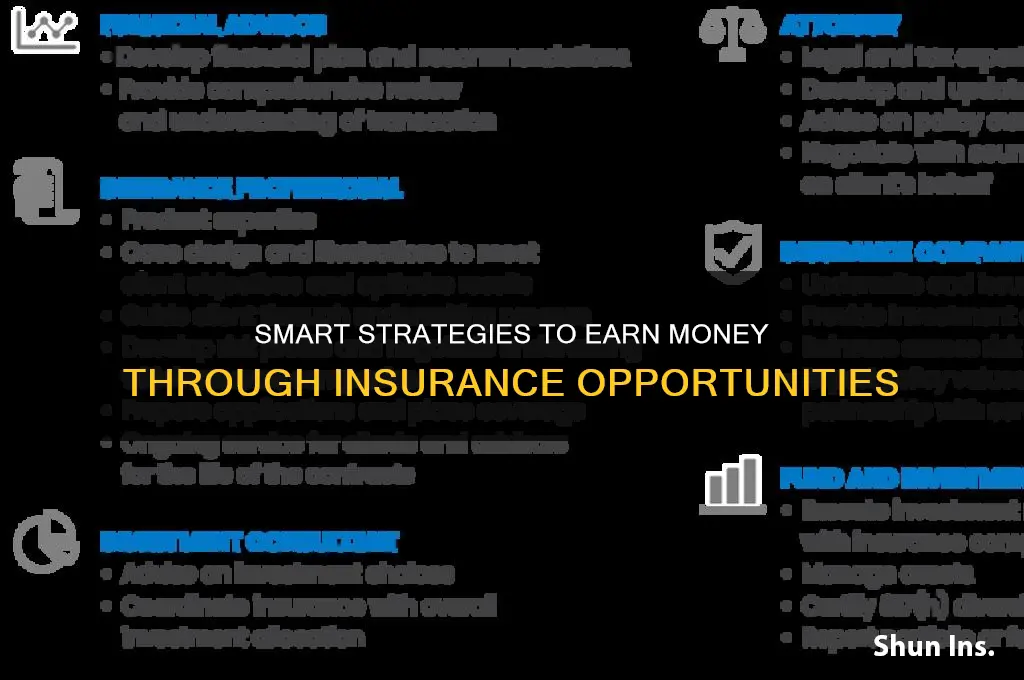

Earning money from insurance involves leveraging various strategies within the insurance industry, whether as an agent, broker, or through investment opportunities. As an insurance professional, you can generate income by selling policies, earning commissions, and building a client base through referrals and networking. Additionally, investing in insurance products like annuities or life insurance policies can provide long-term returns. For those with a financial background, reinsurance or insurance-linked securities offer alternative investment avenues. Understanding the market, staying updated on industry trends, and providing excellent customer service are key to maximizing earnings in this field.

Explore related products

What You'll Learn

- Sell Insurance Policies: Become an agent, earn commissions by selling life, health, auto, or property insurance plans

- Referral Programs: Earn bonuses by referring clients to insurance companies or agents for policy purchases

- Claims Assistance: Offer claim filing or dispute resolution services for a fee to policyholders

- Insurance Blogging: Create content, monetize through ads, affiliate marketing, or sponsored posts in the insurance niche

- Consulting Services: Provide expert advice on policy selection, risk management, or cost optimization for businesses/individuals

![]()

Sell Insurance Policies: Become an agent, earn commissions by selling life, health, auto, or property insurance plans

Becoming an insurance agent is a direct path to earning money through commissions by selling policies that protect individuals and businesses. The role requires licensing, which involves passing state-specific exams and completing pre-licensing courses. Focus on a niche—life, health, auto, or property insurance—to tailor your expertise and attract a targeted client base. For instance, life insurance agents often work with families planning for the future, while auto insurance agents cater to drivers seeking mandatory coverage. Each policy sold earns you a commission, typically a percentage of the premium, providing a scalable income based on your sales volume.

To succeed, build a strong network through referrals, community involvement, and digital marketing. Attend local events, join professional organizations, and leverage social media to establish credibility and reach potential clients. Tools like customer relationship management (CRM) software can help track leads and follow-ups, ensuring no opportunity slips through the cracks. For example, a health insurance agent might partner with small businesses to offer group plans, while a property insurance agent could collaborate with real estate agents to reach homebuyers. Diversifying your product offerings within your niche can also increase earning potential.

However, the role comes with challenges. Commission-based income means earnings fluctuate, especially in the early stages. Agents must also stay updated on industry regulations and policy changes to provide accurate advice. Investing in ongoing education, such as continuing education courses, is essential to maintain licensure and stay competitive. Additionally, balancing client acquisition with policy servicing requires strong time management skills. For instance, a life insurance agent might spend mornings prospecting and afternoons meeting with clients to review policies.

Despite these challenges, the earning potential is significant. Top-performing agents often earn six-figure incomes by combining high sales volumes with residual commissions from policy renewals. For example, selling a whole life insurance policy can yield both upfront and recurring commissions over the policy’s lifetime. Agents can further boost earnings by specializing in high-value policies, such as commercial property insurance or comprehensive health plans. Success hinges on persistence, relationship-building, and a deep understanding of client needs.

In conclusion, selling insurance policies as an agent offers a clear pathway to earning money through commissions. By focusing on a specific insurance type, building a robust network, and staying informed, agents can create a sustainable and lucrative career. While the role demands dedication and adaptability, the financial rewards and opportunity to help others make it a compelling choice for those willing to invest time and effort.

Is KoFC Insurance a Budget-Friendly Choice for Your Needs?

You may want to see also

Explore related products

![]()

Referral Programs: Earn bonuses by referring clients to insurance companies or agents for policy purchases

Referral programs in the insurance industry are a powerful tool for both individuals and businesses to generate additional income. By leveraging your network, you can earn bonuses or commissions for every successful policy purchase made through your referral. Insurance companies often design these programs to incentivize word-of-mouth marketing, recognizing that personal recommendations carry significant weight in decision-making. For instance, a typical referral bonus might range from $25 to $100 per policy, depending on the type and value of the insurance product. This approach not only benefits the referrer but also helps insurance agents and companies expand their client base with minimal advertising costs.

To maximize earnings from referral programs, it’s essential to understand the mechanics and optimize your strategy. Start by identifying insurance companies or agents that offer competitive referral bonuses. Some programs provide flat-rate rewards, while others offer a percentage of the policy’s first-year premium. For example, referring someone to a life insurance policy might yield a higher bonus compared to a basic auto insurance policy. Additionally, track your referrals using unique codes or links provided by the insurance company to ensure proper credit. Building trust with your network is crucial; only recommend policies or agents you genuinely believe in to maintain credibility and encourage repeat referrals.

A comparative analysis reveals that referral programs in insurance often outperform other side-income strategies due to their scalability and low effort. Unlike selling products or freelancing, referring clients requires minimal time investment once your network is established. For instance, a part-time freelancer might earn $20 per hour, but a single successful referral could yield a $50 bonus in less time. Moreover, insurance referral programs often have no cap on earnings, allowing you to scale your income based on your network’s size and engagement. However, it’s important to compare programs across different companies to find the most lucrative opportunities and avoid those with restrictive terms or low payouts.

Practical tips can significantly enhance your success in insurance referral programs. First, target specific demographics within your network, such as young professionals for renters’ insurance or families for life or health insurance. Tailor your pitch to address their unique needs, increasing the likelihood of conversion. Second, utilize social media and email campaigns to reach a broader audience, but personalize your messages to avoid appearing spammy. Finally, stay informed about seasonal promotions or limited-time bonuses that insurance companies may offer to boost referral activity. By combining strategic targeting with consistent effort, you can turn referral programs into a steady income stream.

Haven Life Insurance: A Longstanding Provider of Financial Security

You may want to see also

Explore related products

![]()

Claims Assistance: Offer claim filing or dispute resolution services for a fee to policyholders

Policyholders often find the claims process daunting, with complex paperwork, tight deadlines, and unclear communication from insurers. This frustration creates a lucrative opportunity for claims assistance services. By offering to handle claim filing or dispute resolution for a fee, you can position yourself as a trusted intermediary, alleviating stress for policyholders while generating income.

Identifying Your Niche:

Not all claims are created equal. Focus on specific insurance types (e.g., health, auto, property) or claim complexities (e.g., denied claims, underpaid settlements). For instance, health insurance claims involving chronic conditions or specialized treatments often require meticulous documentation and appeals. Similarly, property claims after natural disasters can overwhelm policyholders, making your expertise invaluable.

Pricing Your Services:

Fee structures can vary. Consider a flat fee for straightforward filings, a percentage-based fee for successful dispute resolutions, or a retainer model for ongoing assistance. For example, charging $200 for a basic claim filing or 10% of the recovered amount for disputed claims can balance accessibility and profitability. Transparency in pricing builds trust and attracts clients.

Building Credibility:

Success in this field hinges on expertise and reliability. Obtain certifications in insurance claims processing or dispute resolution, and showcase case studies of successful outcomes. Partnering with insurance brokers or legal professionals can enhance your credibility and expand your network. Additionally, offer free initial consultations to assess claim viability and demonstrate your value.

Navigating Challenges:

Be prepared for insurers’ resistance during disputes. Stay updated on insurance regulations and leverage your knowledge to advocate for policyholders. Document every interaction meticulously, as this can be pivotal in resolving disputes. Also, manage client expectations by clearly communicating potential timelines and outcomes, ensuring satisfaction even in challenging cases.

By specializing in claims assistance, you not only tap into a growing demand but also provide a service that significantly impacts policyholders’ financial well-being. With the right approach, this venture can be both profitable and rewarding.

Exploring San Lake Mutual Insurance: Benefits, Coverage, and Customer Reviews

You may want to see also

Explore related products

![]()

Insurance Blogging: Create content, monetize through ads, affiliate marketing, or sponsored posts in the insurance niche

Blogging about insurance might seem like a niche endeavor, but it’s a goldmine for monetization if done strategically. The insurance industry is vast, with consumers constantly seeking clarity on policies, comparisons, and cost-saving tips. By creating a blog focused on this niche, you position yourself as an authority while tapping into multiple revenue streams. The key lies in understanding your audience’s pain points—whether it’s deciphering complex policies, finding affordable plans, or understanding claims processes—and delivering content that solves these problems.

To monetize effectively, start by diversifying your income sources. Display ads, such as Google AdSense, can generate passive income based on traffic volume. For instance, a blog with 10,000 monthly visitors could earn $100–$300 per month, depending on ad placement and click-through rates. However, ads alone may not maximize earnings. Affiliate marketing is another powerful tool. Partner with insurance comparison platforms like Policygenius or insurers themselves, earning commissions for every lead or sale generated through your unique affiliate links. A single conversion could yield $20–$50, making this a lucrative option if your content drives targeted traffic.

Sponsored posts offer a third monetization avenue, but they require a delicate balance. Brands may pay $200–$1,000 per post, depending on your blog’s reach and engagement. The challenge? Maintaining credibility. Always disclose sponsorships and ensure the content aligns with your audience’s interests. For example, a sponsored post about renters insurance should provide genuine value, not just promote a product. Transparency builds trust, which is essential for long-term success in this niche.

Success in insurance blogging hinges on consistency and SEO optimization. Focus on long-tail keywords like “best life insurance for seniors over 65” or “how to lower car insurance premiums for young drivers.” These phrases have lower competition but higher intent, attracting readers ready to take action. Pair this with engaging, actionable content—think step-by-step guides, infographics, or case studies—and you’ll not only rank higher on search engines but also convert readers into revenue.

Finally, track your performance relentlessly. Use tools like Google Analytics to monitor traffic sources, bounce rates, and conversion metrics. Experiment with different monetization strategies to see what resonates with your audience. For example, if affiliate links outperform ads, double down on product reviews and comparison posts. Insurance blogging isn’t a quick-win scheme, but with patience, strategic planning, and a focus on value, it can become a sustainable, profitable venture.

Should You Inform Your Insurance About a Lifted Truck Modification?

You may want to see also

Explore related products

![]()

Consulting Services: Provide expert advice on policy selection, risk management, or cost optimization for businesses/individuals

Businesses and individuals often find themselves overwhelmed by the complexity of insurance policies, leading to suboptimal coverage or unnecessary expenses. This is where consulting services step in, offering a lifeline to those navigating the intricate world of insurance. As an insurance consultant, your role is to demystify the process, ensuring clients make informed decisions tailored to their unique needs.

The Art of Policy Selection: Imagine a small business owner, Sarah, who runs a thriving online retail store. She's concerned about potential liabilities but is unsure which insurance policies are essential. This is a common scenario where your expertise becomes invaluable. You'd begin by assessing Sarah's business operations, identifying risks such as product liability, cyber threats, or property damage. Then, you'd educate her on the relevant policies: General Liability, Cyber Insurance, and Commercial Property Insurance. By explaining the coverage, exclusions, and potential costs, you empower Sarah to make an informed choice, ensuring her business is adequately protected without overspending.

Risk Management Strategies: Consulting goes beyond policy selection. It involves crafting risk management plans to minimize potential losses. For instance, for a client with a high-risk profession, like a roofing contractor, you might advise on safety protocols and training programs to reduce accident rates. This not only lowers insurance premiums but also creates a safer work environment. You could provide data-driven insights, showing how implementing specific safety measures has historically reduced claims by a certain percentage, thus saving clients money in the long run.

Cost Optimization Techniques: Insurance costs can be a significant burden, especially for businesses. Here, your analytical skills come into play. You'd review existing policies, identifying areas for cost reduction without compromising coverage. This might involve negotiating with insurers, bundling policies, or adjusting deductibles. For instance, you could suggest increasing the deductible on a low-risk policy to lower the premium, but only if the client has sufficient funds to cover the deductible in case of a claim. This strategy requires a delicate balance, ensuring clients understand the trade-offs.

To excel in this consulting role, consider the following steps: First, obtain relevant certifications and stay updated on industry trends. Second, develop strong communication skills to simplify complex insurance concepts for clients. Third, build a network of insurance providers to offer a wide range of options. Lastly, provide personalized service, understanding each client's unique circumstances. By offering expert guidance, you not only help clients navigate the insurance maze but also establish a profitable consulting business, filling a critical gap in the market. This approach ensures clients receive tailored advice, making informed decisions that protect their assets and financial well-being.

How to File a Claim with Globe Life Insurance

You may want to see also

Frequently asked questions

You can earn money from insurance by becoming an insurance agent or broker, selling policies to clients and earning commissions. Alternatively, you can invest in insurance-related stocks, mutual funds, or ETFs to benefit from the industry's growth.

Passive income from insurance can be generated by purchasing dividend-paying whole life insurance policies or investing in insurance-focused real estate investment trusts (REITs) that manage properties insured by insurance companies.

Yes, many insurance companies offer referral programs where you can earn cash rewards, gift cards, or discounts on your premiums for successfully referring new customers who purchase policies.

You can earn money by working in roles like claims adjuster, underwriter, or insurance consultant. These positions often offer competitive salaries and bonuses without requiring direct sales. Additionally, you can start a blog or YouTube channel about insurance and monetize it through ads, sponsorships, or affiliate marketing.