Mortgage insurance is an insurance policy that protects the lender or titleholder against financial loss if the borrower defaults on payments or fails to meet their mortgage obligations. It is usually required when homebuyers make a down payment of less than 20% of the purchase price of the home, although there may be exceptions. Mortgage insurance also applies to Federal Housing Administration (FHA) and U.S. Department of Veterans Affairs (VA) loans, where the borrower pays a monthly premium. This additional layer of protection for the lender allows them to offer loans to borrowers who may not otherwise qualify, although it increases the cost of the loan for the borrower.

| Characteristics | Values |

|---|---|

| Who does it protect? | The lender or titleholder |

| Who pays for it? | The borrower |

| When is it required? | When the down payment is less than 20% of the purchase price |

| What is the cost? | Depends on the type of loan and the borrower's credit score |

| How is it paid? | Monthly premium, upfront premium, or a combination of both |

| Can it be cancelled? | Yes, once the loan balance reaches 80% of the original value |

| Are there alternatives? | Yes, such as a "piggyback" second mortgage or a VA-backed loan |

| What happens if the borrower defaults? | The insurance company reimburses the lender for the remaining balance |

Explore related products

$10.81 $17.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

The requirement to buy PMI usually applies when refinancing a conventional loan, where the borrower's equity is less than 20% of the home's value. PMI is arranged by the lender and provided by private insurance companies. The cost of PMI varies depending on the loan and down payment size, the type of mortgage (fixed or adjustable-rate), and the borrower's credit score. Generally, those with higher credit scores will pay lower PMI rates.

PMI can be paid in different ways. Some borrowers pay a monthly premium on top of their regular mortgage payment, while others may have the option to pay the premium upfront at closing or through a combination of upfront and monthly payments. It is also possible to include the premium in the mortgage itself, but this will result in paying interest on that additional amount, increasing the overall cost of the loan.

While PMI increases the cost of the loan, it can help borrowers qualify for loans they might not otherwise obtain. It lowers the risk to the lender, making them more confident in extending credit to high-risk buyers. Once the borrower has reached a certain level of equity in their home or paid off a significant portion of the loan, they may be able to cancel the PMI.

Insurance Dividends: Tax Reporting Time

You may want to see also

Explore related products

![]()

When mortgage insurance is required

Mortgage insurance is typically required when a borrower's down payment is less than 20% of the purchase price of the home. In this case, the borrower may need to purchase private mortgage insurance (PMI) to secure a loan. PMI rates vary based on credit score and down payment amount but are generally cheaper for borrowers with good credit.

Mortgage insurance is also typically required for loans backed by the Federal Housing Administration (FHA) and the U.S. Department of Agriculture (USDA). FHA loans require an upfront mortgage insurance premium and an annual premium, regardless of the down payment amount. The upfront premium is 1.75% of the loan amount and is due when the mortgage closes. The annual premium ranges from 0.15% to 0.75% of the average outstanding loan balance.

USDA loans, which are for rural home buyers, have an upfront guarantee fee of 1% of the loan amount and an annual fee for the life of the loan. While VA-backed loans do not require monthly mortgage insurance premiums, there is an upfront "funding fee" that can be rolled into the mortgage.

Mortgage insurance protects the lender in the event that the borrower falls behind on payments. It lowers the lender's risk and can help high-risk buyers qualify for a loan. However, it increases the overall cost of the loan for the borrower.

The Evolution of Farmers Insurance: A Legacy of Protection and Service

You may want to see also

Explore related products

![]()

How mortgage insurance works

Mortgage insurance is an insurance policy that protects the lender or titleholder against financial loss if the borrower defaults on payments or fails to meet their contractual obligations. It does not extend the same protection to borrowers, who can still lose their homes through foreclosure if they fall behind on payments.

Lenders typically require mortgage insurance for homebuyers whose down payment is less than 20% of the purchase price of their new home. This allows lenders to offer loans to borrowers who might not otherwise qualify. However, it increases the cost of the loan.

There are several types of mortgage insurance:

- Private mortgage insurance (PMI): This is the most common type of mortgage insurance and is arranged by the lender and provided by private insurance companies. It is required for conventional loans with a down payment of less than 20%.

- Qualified mortgage insurance premium (MIP): This is required for loans backed by the Federal Housing Administration (FHA), regardless of the size of the down payment. It also includes an upfront cost of 1.75% of the loan amount, which can be added to the loan balance.

- Mortgage title insurance: This protects the titleholder if the borrower defaults on payments or passes away.

- Borrower-paid mortgage insurance (BPMI): The borrower pays a monthly premium attached to their regular mortgage payments.

- Single-premium mortgage insurance (SPMI): The buyer pays a lump sum either at closing or financed into the mortgage itself, reducing monthly payments. However, interest is charged on the additional amount, increasing the cost of the loan over time.

- Lender-paid mortgage insurance (LPMI): The lender covers the premium, but the borrower pays a higher interest rate on the mortgage.

- Split-premium mortgage insurance: This divides the premium into an upfront cost and a balance paid over time with monthly mortgage payments. This can reduce monthly payments and the amount of cash needed at closing.

Eradicating Direct Payment Hassles: A Guide to Canceling Farmers Insurance Auto-Payments

You may want to see also

Explore related products

![]()

Different types of mortgage insurance

Mortgage insurance is typically required for loans where the borrower has made a down payment of less than 20%. This insurance protects the lender in the event that the borrower defaults on the loan. While it does not protect the borrower, it does enable borrowers who may not otherwise qualify for a loan to secure one.

There are two main types of mortgage insurance: Mortgage Insurance Premium (MIP) and Private Mortgage Insurance (PMI). MIP is required for all Federal Housing Administration (FHA) loans, while PMI is typically required for conventional loans.

Mortgage Insurance Premium (MIP)

MIP is a special type of mortgage insurance for loans backed by the Federal Housing Administration (FHA). It is required for every FHA loan, regardless of the down payment amount. MIP includes an upfront cost, which is typically 1.75% of the base loan amount, and a monthly cost, which is generally between 0.15% and 0.75% of the loan amount. If you make a down payment of less than 10%, you will need to pay MIP for the life of the loan.

Private Mortgage Insurance (PMI)

PMI is typically required for conventional loans, which are not backed by a federal government organisation. The cost of PMI varies depending on factors such as the down payment amount and the borrower's credit score. It is generally between 0.5% and 2% of the loan amount. PMI can be paid in different ways, including borrower-paid mortgage insurance (BPMI), lender-paid mortgage insurance (LPMI), and split-premium mortgage insurance.

Borrower-Paid Mortgage Insurance (BPMI)

BPMI is the most common type of PMI, where the borrower pays a monthly premium that is attached to their regular mortgage payments. BPMI can generally be cancelled once the borrower reaches 20% equity in their home.

Lender-Paid Mortgage Insurance (LPMI)

With LPMI, the lender covers the premium, but the borrower pays a higher interest rate on the mortgage. LPMI cannot be cancelled, even when the borrower reaches 20% equity, and the elevated interest rate continues until the loan is paid off.

Split-Premium Mortgage Insurance

This type of insurance divides the premium into two parts. The borrower pays a portion upfront, typically at closing, and the balance is paid over time with the monthly mortgage payments. Split-premium mortgage insurance can reduce both monthly payments and the amount of cash needed at closing.

Alliance Global Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

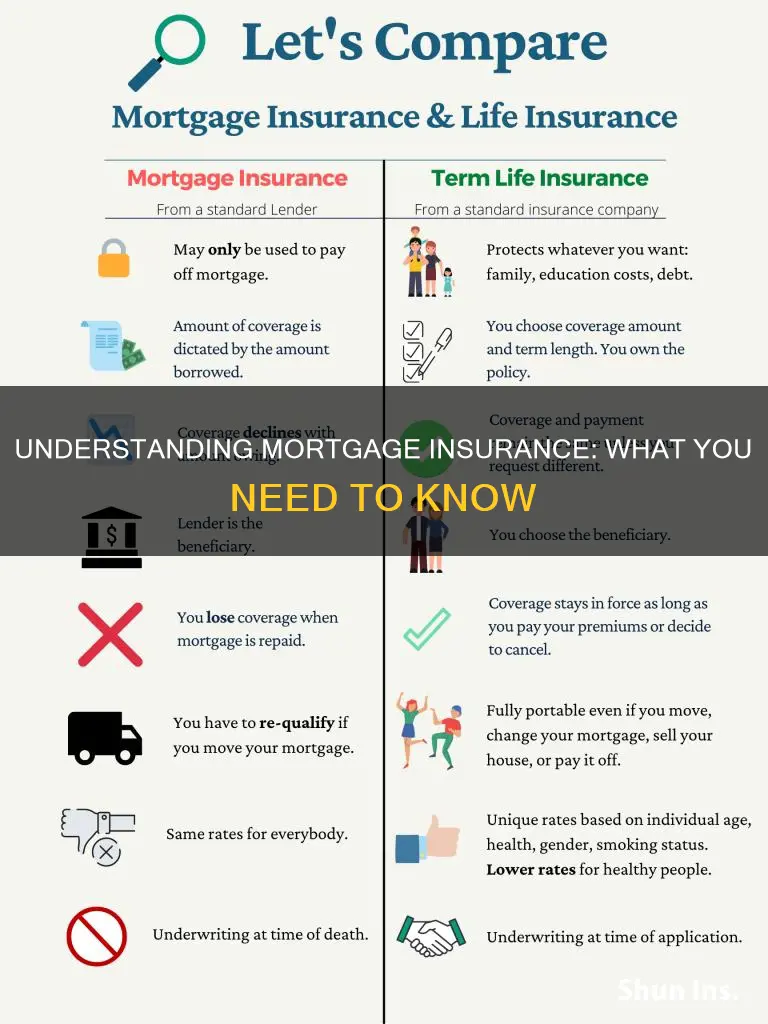

Mortgage insurance vs mortgage life insurance

Mortgage insurance, also known as private mortgage insurance (PMI), is not the same as life insurance. It protects the lender in the event that the borrower defaults on their mortgage. Typically, borrowers who make a down payment of less than 20% of the purchase price of the home are required to pay for mortgage insurance. It is also usually required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. Mortgage insurance can be paid monthly or as a lump sum at closing, and it increases the overall cost of the loan.

Mortgage protection insurance, on the other hand, is a type of life insurance that pays off the remaining balance of the mortgage directly to the lender in the event of the borrower's death. It is sometimes referred to as "mortgage life insurance" and is typically sold by mortgage lenders. The payout from mortgage protection insurance ensures that the borrower's loved ones can keep the house. However, unlike life insurance, it does not offer flexibility in how the payout is used. Additionally, the payout from mortgage protection insurance decreases over time as the mortgage balance is paid off, while the premiums remain the same.

Life insurance, unlike mortgage protection insurance, provides a lump-sum death benefit to the beneficiaries, who can then choose to use it to pay off the mortgage or for any other purpose. It can be purchased as a term life policy, which covers a temporary period, or as whole life insurance, where the policyholder decides on the level of coverage. Life insurance policies also do not decrease in value over time, unlike mortgage protection insurance.

In summary, mortgage insurance protects the lender, while mortgage protection insurance and life insurance provide financial protection for the borrower's loved ones in the event of their death. The main difference between mortgage protection insurance and life insurance is the flexibility offered by the latter in terms of payout usage and the fact that the payout amount does not decrease over time.

Air Vac Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance is an insurance policy that protects the lender or titleholder against financial loss if the borrower defaults on payments or cannot meet mortgage obligations. It is usually paid monthly, but can also be paid in a lump sum.

Mortgage insurance protects the lender, not the borrower. If the borrower defaults on their payments, the insurance company will reimburse the lender a percentage of the amount owed.

Mortgage insurance is typically required when the down payment on a home is less than 20%. It is also usually required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans.

The cost of mortgage insurance depends on the type of loan and the size of the down payment. The lower the down payment, the higher the lender's risk, and the more expensive the insurance premiums will be.