FHA loans are a popular option for first-time homebuyers as they are designed to be easier to qualify for, with more lenient standards for credit scores and down payments. FHA loans are insured by the Federal Housing Administration (FHA), which compensates the lender for the outstanding balance in case of borrower default. To secure an FHA loan, borrowers are required to pay a mortgage insurance premium (MIP) to protect the lender's financial interests. This additional expense is a drawback for borrowers, but it makes the FHA program possible by mitigating the risk of lending to applicants with lower credit scores and smaller down payments. This article will explore the requirements and process of qualifying for FHA mortgage insurance, including the costs involved and methods to reduce or remove FHA mortgage insurance premiums.

| Characteristics | Values |

|---|---|

| FHA loan type | Mortgage that's backed by the Federal Housing Administration (FHA) |

| FHA loan benefit | More lenient standards for borrowers, like credit score and down payment requirements |

| FHA loan insurance requirement | Mortgage Insurance Premium (MIP) |

| FHA MIP purpose | Provides protection to the mortgage lender in the event that the borrower defaults on their loan |

| FHA MIP payment | Two payments: an upfront premium (1.75% of the loan amount) and an additional annual payment (0.55% of the loan amount) |

| FHA MIP removal | Possible through refinancing to a conventional loan with at least 20% equity |

| FHA MIP reduction | Possible through an FHA Streamline Refinance, which allows for a lower interest rate without a new appraisal or income verification |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance premium (MIP)

The FHA MIP involves two payments: an upfront premium and an additional annual payment. The upfront premium, also known as the Upfront Mortgage Insurance Premium (UFMIP), is charged as a lump sum of 1.75% of the loan amount. This can be financed into the mortgage amount or paid in cash in full. The annual premium is charged monthly, with the premium amount divided by 12 and added to your monthly mortgage payment. The cost of the annual MIP ranges between 15 and 75 basis points (0.15% to 0.75% of the loan amount). It is important to note that FHA mortgage insurance rates can increase, but your existing MIP will not be affected.

To reduce or remove your FHA MIP, there are a few options. One option is to make a larger down payment of at least 10%. With a down payment of 10% or more, you can remove the MIP after 11 years. Another option is to refinance your FHA loan into a conventional loan once you have at least 20% equity. Refinancing to a conventional loan will eliminate the need for mortgage insurance altogether. However, it is important to consider factors such as credit score, debt-to-income ratio, interest rates, and closing costs when deciding to refinance. Additionally, an FHA Streamline Refinance allows you to refinance your existing FHA loan to a lower interest rate without a new appraisal or income verification, which can lower your overall mortgage payment.

Insuring Your Flip House

You may want to see also

Explore related products

![]()

How to qualify with a lower credit score

FHA loans are insured by the Federal Housing Administration (FHA). They are designed to help first-time buyers or those with less-than-perfect credit scores to get on the property ladder. The FHA insures these loans, so lenders are more willing to approve applicants with lower credit scores.

FHA loans have more lenient standards for borrowers, such as lower credit score and down payment requirements. You may be able to qualify with a credit score as low as 500, but you will need a down payment of at least 10%. With a credit score of 580 or higher, you may be able to get an FHA loan with a down payment as low as 3.5%. Applicants with higher credit scores typically qualify for better rates.

If you have a bankruptcy in your credit profile, you may still qualify for an FHA loan if it was discharged at least two years before you apply. If you have a history of foreclosure or default on a previous FHA loan, you may be eligible after three years.

To qualify for an FHA loan, you must prove you have a steady employment history. Your income must be verifiable by sharing pay stubs, W-2s, federal tax returns, and bank statements with your lenders. You must also meet the debt requirements. The lower your debt-to-income ratio (DTI), the better your chances of qualifying. Your monthly mortgage payment should be no more than 31% of your monthly gross income, and your DTI should not exceed 43% of monthly gross income.

If you are looking to improve your credit score, it is recommended that you start preparing several months in advance. You can check your credit score for free and correct any inaccuracies. The stronger your credit score, the better your chances of getting approved and receiving a lower interest rate.

House Flippers: What Insurance?

You may want to see also

Explore related products

![]()

FHA loan refinancing options

FHA loans are a good option for first-time homebuyers who may not have saved enough for a large down payment. They are backed by the Federal Housing Administration and typically have more lenient standards for borrowers, like credit score and down payment requirements.

FHA loans require borrowers to pay a mortgage insurance premium (MIP), which is an additional payment that provides the mortgage lender with protection in the event that you default on your loan. This means that lenders are more willing to approve applicants with lower credit scores.

If you want to remove your FHA mortgage insurance, you can refinance and change your FHA loan into a conventional mortgage to cancel your MIP payments. Here are some refinancing options to consider:

FHA Streamline Refinance

This option is available to borrowers with an existing FHA loan who are looking to lower their interest rate and monthly payments. It requires limited borrower credit documentation and underwriting and is available under credit-qualifying and non-credit-qualifying options. To qualify, you must have made at least 6 months of on-time payments on your current FHA loan and demonstrate that the refinance will result in a "net tangible benefit", such as a lower payment or shorter loan term.

FHA Simple Refinance

This option is for homeowners who originally purchased their home with an FHA loan and want to lower their interest rate or monthly mortgage payment. It also allows homeowners to switch from an adjustable-rate mortgage (ARM) to a fixed-rate loan. To qualify, you typically need a credit score of 580 and to have made all your loan payments from the last 6 months.

Cash-Out Refinance

This option allows homeowners to refinance their existing mortgage by taking out another mortgage for more than they currently owe. To be eligible, borrowers need at least 20% equity in the property based on a new appraisal. This can be used for home improvement, college tuition, debt consolidation, or other personal finance goals.

When deciding whether refinancing is a good option for FHA mortgage insurance removal, there are several factors to consider, including your equity, credit score, debt-to-income ratio, interest rates, and closing costs.

Farmers Insurance Open's Wednesday Start: A Tradition Unlike Any Other

You may want to see also

Explore related products

![]()

Removing FHA mortgage insurance

FHA loans are backed by the Federal Housing Administration and are a popular financing option for first-time homebuyers due to their less restrictive down payment and credit score requirements. However, one of the biggest drawbacks of FHA loans is the mandatory mortgage insurance premium (MIP), which can significantly increase the upfront closing costs and monthly payments.

There are a few ways to remove or reduce FHA mortgage insurance:

- Refinancing to a Conventional Loan: The most common way to eliminate FHA mortgage insurance is by refinancing the FHA loan into a conventional mortgage. To do this, you typically need to have at least 20% equity in your home and meet the lender's qualification criteria, which often include a minimum credit score of 620. By refinancing, you can also take advantage of lower interest rates and potentially lower your monthly payments.

- Automatic MIP Removal: In certain scenarios, you may qualify for automatic MIP removal without refinancing. If your loan origination date was between January 1, 2001, and June 2, 2013, your MIP will be canceled once you reach a loan-to-value ratio of 78% or have 22% equity in your home. For loans originated on or after June 3, 2013, with a down payment of at least 10%, the MIP will be canceled after 11 years.

- FHA Streamline Refinance: If you are not eligible for a conventional mortgage refinance, you may consider an FHA Streamline Refinance. This option allows you to refinance your existing FHA loan to a lower interest rate without a new appraisal or income verification. While it won't eliminate your MIP, it can reduce your overall mortgage payment. To qualify, you must have made at least six months of on-time payments on your current FHA loan and demonstrate a "net tangible benefit," such as a lower payment or shorter loan term.

- Reducing MIP Expenses: If you're unable to remove the MIP entirely, you can still lower your MIP expenses by increasing your down payment. By bringing at least 10% to the closing table, you'll qualify for a lower annual MIP payment and reduce the amount you borrow, resulting in a lower upfront premium.

It's important to carefully consider the costs and benefits of each option before making a decision. Refinancing, for example, typically comes with fees that can range from 3% to 6% of the total loan amount. Additionally, it's essential to review your loan documents and understand the specific requirements and conditions of your FHA loan.

Down Payments: Avoiding Mortgage Insurance

You may want to see also

Explore related products

![]()

FHA mortgage insurance reduction

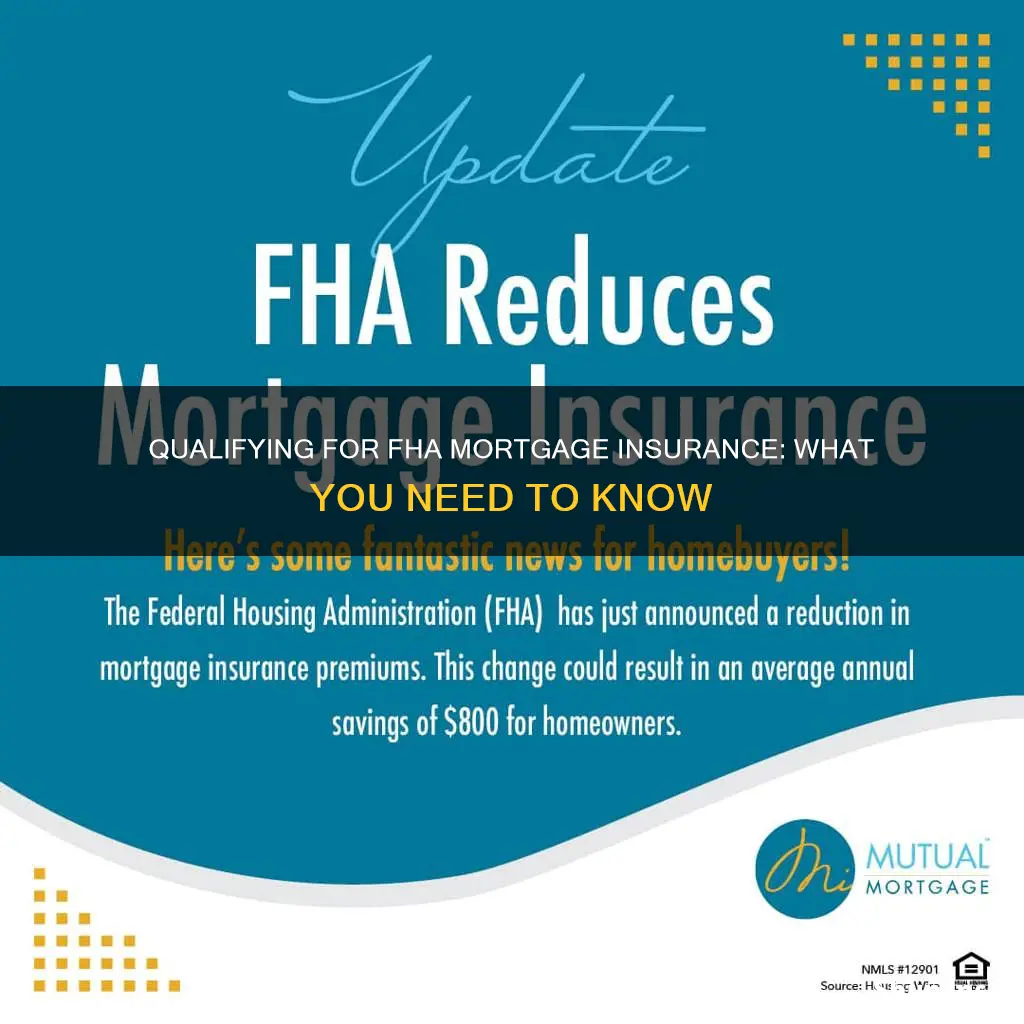

FHA loans are backed by the Federal Housing Administration and are designed to help first-time homebuyers or those with lower credit scores. These loans require mortgage insurance to protect lenders from losses in the event of borrower default. This insurance, known as Mortgage Insurance Premium (MIP), is an additional payment made by the borrower to secure the loan.

The FHA recently announced a reduction in annual MIP costs for certain home loans, which took effect on March 20, 2023. This reduction does not apply to upfront MIP, which is paid at closing, but rather to the annual MIP, which is paid yearly and broken up into monthly payments. The FHA lowered the MIP by 30 basis points, resulting in a savings of around $800 per year for borrowers. This reduction aims to make homeownership more accessible and affordable, especially for low-income and first-time homebuyers.

Borrowers can also take steps to lower their MIP expenses. One way is to increase the down payment to at least 10%, which qualifies for a lower annual MIP payment and allows borrowers to stop paying MIP after 11 years. Another option is to refinance the FHA loan into a conventional mortgage once 20% equity is reached, eliminating the need for MIP altogether.

It is important to note that FHA mortgage insurance removal or reduction may depend on various factors, including the borrower's credit score, debt-to-income ratio, interest rates, and closing costs. Additionally, each mortgage lender has its own qualification criteria for refinancing. Therefore, it is recommended to shop around and compare offers from multiple lenders before making a decision.

Farmers Insurance's Texas Two-Step: Understanding the Insurer's Move

You may want to see also

Frequently asked questions

An FHA loan is a type of mortgage that’s backed by the Federal Housing Administration (FHA). Compared to other mortgage options, FHA loans typically have more lenient standards for borrowers, like credit score and down payment requirements.

An FHA mortgage insurance premium (MIP) is an additional payment you make to secure the mortgage loan. It provides your mortgage lender with some protection in the event that you default on your loan.

FHA loans are designed to be easier to qualify for, especially for first-time buyers or those with less-than-perfect credit. The FHA insures these loans, so lenders are more willing to approve applicants with lower credit scores.