Finding the right auto insurance can be a challenge. It's important to compare rates and coverage options from insurance companies by getting multiple quotes. While car insurance is required in almost every U.S. state, the specific type of insurance and amount of coverage needed varies by state and individual.

There are several factors that influence auto insurance rates, including age, gender, marital status, credit score, driving history, location, vehicle type, and insurance history. It's also worth noting that insurance companies use different criteria to write their auto policies, so no two insurance quotes are alike. By understanding these factors and comparing quotes, individuals can find the best auto insurance coverage that suits their needs and budget.

| Characteristics | Values |

|---|---|

| Basic Types of Coverage | Liability Insurance, Collision Insurance, Comprehensive Insurance |

| Additional Coverage Options | Full Tort/Limited Tort, Medical Payments/Personal Injury Protection, Uninsured/Underinsured Motorist Coverage, Towing, Glass Breakage, Rental, Gap |

| Factors Affecting Rates | Deductible, Age, Gender, Demographics, Claims, Moving Violations, Vehicle Choice, Driving Habits, Theft Deterrent Systems, Safety Devices, Accident Prevention Training, Multiple Policies, Payment Plan, Credit Score |

| Factors Affecting Premiums | Credit Score, ZIP Code, Year/Make/Model of Car, Number of Miles Driven, Driving History, Age, Marital Status |

| Liability Insurance Coverage Types | Bodily Injury Liability Coverage, Property Damage Liability Insurance, Uninsured Motorist Coverage |

| Other Coverage Options | Uninsured/Underinsured Motorist Coverage, Comprehensive Coverage, Collision Coverage |

| Ways to Get Cheap Insurance | Understand Factors Affecting Premiums, Increase Deductible, Skip Comprehensive and Collision Coverage, Claim Discounts, Consider Third-Party Ratings, Consider Usage-Based Insurance |

| Ways to Get Insurance Quotes | Online Comparison Sites, Local Captive Agents, Independent Agents or Brokers |

Explore related products

What You'll Learn

![]()

Understand the basic types of coverage

Understanding the types of auto insurance coverage is crucial when deciding on a policy. While different states have varying mandates, most basic auto insurance policies consist of six types of coverage: bodily injury liability, personal injury protection (PIP), property damage liability, collision, comprehensive, and uninsured/underinsured motorist coverage. Each type of coverage is priced separately, allowing for customisation based on individual needs and budgets. Here is a detailed overview of each type of coverage:

Bodily Injury Liability

Bodily injury liability coverage applies to injuries caused to someone else by the designated driver or policyholder. This type of coverage also extends to family members listed on the policy when driving someone else's car with permission. It is essential to have adequate liability insurance, as you may be sued for a large sum of money in the event of a serious accident. It is generally recommended to purchase more than the state-required minimum to protect your assets adequately.

Medical Payments or Personal Injury Protection (PIP)

This coverage pays for the treatment of injuries sustained by the driver and passengers in the policyholder's car. PIP can also cover lost wages, funeral costs, and the cost of replacing services normally performed by someone injured in an auto accident. It provides broad coverage and is required in some states.

Property Damage Liability

Property damage liability coverage pays for damage caused to someone else's property. This typically includes damage to another person's car but can also extend to lamp posts, telephone poles, fences, buildings, or other structures. It is important to note that this coverage only applies to property damage resulting from an accident.

Collision Coverage

Collision coverage protects your car if you collide with another vehicle, person, or object. It helps cover the costs of repairing your car, regardless of fault. However, it is important to note that collision coverage does not include damage caused by animals or mechanical issues. Collision coverage is generally sold with a separate deductible, and having it can reduce out-of-pocket costs.

Comprehensive Coverage

Comprehensive coverage protects your car from incidents other than collisions. It covers events such as fire, theft, vandalism, severe weather, and encounters with animals. Comprehensive coverage is typically sold alongside collision coverage, and it is often required if you lease or finance your vehicle. Like collision coverage, comprehensive coverage is usually associated with a separate deductible.

Uninsured and Underinsured Motorist Coverage

This coverage reimburses you, a family member, or a designated driver if any of you are hit by an uninsured or underinsured driver. It also offers protection in hit-and-run situations or if, as a pedestrian, you are struck by an uninsured or underinsured motorist. This type of coverage is mandatory in some states but optional in others.

Commercial Auto Insurance: Monthly Cost Breakdown

You may want to see also

Explore related products

![]()

Compare quotes from multiple companies

Comparing quotes from multiple companies is a great way to find the best deal on auto insurance. Here are some tips to help you get started:

Understand the factors that affect insurance premiums

Insurers consider various factors when determining rates, including your driving record, age, gender, vehicle, location, and credit history. Your premium will also depend on the type and amount of coverage you choose.

Get quotes from multiple companies

Use a comparison website or work with an insurance agent to get quotes from multiple companies. Provide the same information to each company, including your personal details, vehicle information, driving history, and the coverage options you want. This will ensure that you can accurately compare the quotes.

Compare rates and coverage options

When comparing quotes, make sure to consider both the price and the coverage offered. Pay attention to the liability coverage limits, deductibles, and any additional coverage options, such as comprehensive and collision insurance.

Check the reputation of the insurance company

In addition to the price and coverage, consider the reputation and customer service of the insurance company. Look for companies with positive reviews and a good track record of handling claims. You can also check their financial strength through rating firms like AM Best.

Ask about discounts

Many insurance companies offer discounts for things like a clean driving record, safety features in your car, or bundling multiple policies. Be sure to ask about any discounts you may be eligible for when getting a quote.

Review the policy carefully before purchasing

Before purchasing a policy, take the time to review it carefully. Make sure you understand the coverage limits, deductibles, and any exclusions or restrictions. It's also a good idea to compare the final quote with the initial quote to ensure there are no surprises.

Ford Credit: Gap Insurance Included?

You may want to see also

Explore related products

$28.02 $32.99

![]()

Research insurer reputation

When researching auto insurance companies, it's important to look into their reputation, including their financial stability and customer satisfaction.

Financial Stability

You can research the financial stability of an auto insurance company by visiting the website of an insurance rating organization. The most popular rating companies are AM Best, Fitch, and Standard & Poor’s. Each of these organizations regularly evaluates insurance company financial reserves, credit rating, and corporate financial strength. The ratings of auto insurance companies of A+, A, or A- are in excellent financial condition. Insurance companies with lower grades have smaller financial reserves in place, less favorable credit ratings, or are less financially strong.

Customer Satisfaction

You can research an insurance company’s consumer satisfaction rating through JD Power and Associates, which conducts annual surveys to evaluate how happy consumers are with insurance company customer service, claims processing, rates, and overall response to their needs. You can also research an insurance company through the Better Business Bureau (BBB). The BBB will certify insurance companies that work with customers to resolve problems and are committed to providing excellent service to their customers. The BBB also keeps records about insurance companies with high numbers of complaints that are filed with the BBB.

You can also check your state insurance website for information regarding auto insurance companies, including licensing information, consumer complaints, and lawsuits filed against auto insurance companies.

Motor Vehicle Self-Insurance Explained

You may want to see also

Explore related products

![[2025 Upgrade] Nmoiss Windshield Sun Shade Umbrella - [Vinyl Coating Heat Shield] Protect Car from Sun Rays & Heat Damage Keep Cool and Protect Interior, Spring Structure Edge Medium 56" L x 31" W](https://m.media-amazon.com/images/I/71sL6kb9cLL._AC_UL320_.jpg)

![]()

Understand how insurance companies determine quotes

Insurance quotes are determined by a multitude of factors, and these factors vary across insurance companies. Quotes are determined by the information you provide to the insurer and the coverage you select. When you approach an insurance provider for a new quote, they will ask you for some details about yourself and the property you want to insure. Each quote is customized for the person buying it. For example, for home insurance, the insurance company will ask about your home, where it's located, what kind of plumbing system it has, and what the roof is made of. Each of these details is a factor in the purchase price of the policy, so the insurance company needs to know to issue an accurate quote.

The quote process is also when the customer decides what kinds of coverage they want in their new policy. Coverage selections influence the quoted price. Not every insurance provider's quote process is the same. Each insurance company has its own factors for determining premiums, so they will ask different questions during the quoting process. Not every insurer offers the same coverages, so you may get different options depending on which insurance company you're getting a quote from.

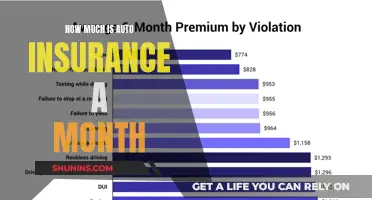

- Your driving history: People with a clean driving record with no tickets or moving violations represent a lower risk to insurers and typically receive lower auto insurance rates.

- Your location: Car insurance companies set rates based in part on where your car is located. It typically costs more to insure vehicles in areas with high theft, vandalism, and accident rates or where repairs and medical care are more expensive. Urban drivers generally pay more for insurance than drivers in suburban or rural areas.

- Your age: Younger drivers are more likely to get into accidents than older drivers, so rates for teens and young adults tend to be higher. Car insurance premiums typically decrease after age 25 if you have a good driving record.

- Your credit history: Some states allow car insurance companies to use credit-based insurance scores to calculate insurance premiums. Typically, higher scores result in lower rates.

- Your vehicle: Some cars cost more to insure than others. Coverage for vehicles with high safety ratings and lower replacement or repair costs will typically be lower.

- How much you drive: In general, the more you drive, the more likely you are to get into an accident. If you put a lot of miles on your car each month, your insurance premium will probably be higher.

- Your coverage limits: A coverage limit is the maximum amount the insurance company will pay for a single claim if you're in an accident or your car is stolen or damaged. The higher the limits, the more your policy will cost.

- Your deductible: The deductible on your policy is the amount you must pay before the insurance company starts paying for the damage. You can usually lower your insurance premium by increasing your deductible.

Gap Insurance: Job Loss Protection

You may want to see also

Explore related products

![]()

Know what information you need to get a quote

To get a car insurance quote, you'll need to provide some personal information, details about your vehicle, and your driving history. Here's a detailed breakdown of the information you'll typically need to provide:

Personal Information:

- Full name and date of birth.

- Home address, as well as the address where the vehicle will be parked or garaged if different from your home address.

- Driver's license number and state of issue.

- Accident prevention course completion date, if applicable.

Vehicle Information:

- Year, make, model, body style, or Vehicle Identification Number (VIN).

- Whether you finance, lease, or own the vehicle.

- Estimated weekly mileage.

- Any safety or anti-theft features installed, such as airbags, anti-lock brakes, or an alarm system.

Driving History:

- Ticket and accident history, including any at-fault accidents or moving violations.

- License suspension information.

- Details of any driving courses or driver's education programs completed.

Having this information readily available will help you obtain an accurate car insurance quote and determine the coverage options, deductible, and policy cost that best suit your needs.

Medical Payments Coverage: Auto Insurance Essential?

You may want to see also

Frequently asked questions

The basic types of auto insurance coverage are liability insurance, collision insurance, and comprehensive insurance. Liability insurance covers third-party personal injury, death-related claims, and damage to another person's property. Collision insurance pays to repair your car after an accident and is required if you have a loan against your vehicle. Comprehensive insurance covers damage from theft, vandalism, fire, water, etc.

Additional types of auto insurance coverage include full tort/limited tort, medical payments/personal injury protection, uninsured/underinsured motorist coverage, towing, glass breakage, rental, and gap insurance.

Factors that impact auto insurance rates include your deductible, age, gender, demographics, claims, moving violations, vehicle choice, driving habits, theft deterrent systems, safety devices, accident prevention training, multiple policies, payment plan, and credit score.

To find cheap auto insurance, shop around and compare quotes from multiple companies, including national companies like Geico and Allstate, as well as smaller insurers. Understand the factors that affect insurance premiums and consider your liability coverage limits, deductible, and whether you need comprehensive and collision coverage. Claim any discounts you may be eligible for and consider usage-based insurance.

You can get free auto insurance quotes online or through an insurance agent. Online comparison sites like The Zebra allow you to compare quotes from multiple companies at once. When getting a quote, you will need to provide your driver's license and personal information, vehicle identification number, date of vehicle purchase, and driving history.